Chilled Seafood in Multiple Retail 2017

|

|

|

- Theresa Powers

- 5 years ago

- Views:

Transcription

1 Market Insight Factsheet Chilled Seafood in Multiple Retail 2017 This factsheet provides a summary of the performance of the chilled seafood sector in the multiple retail seafood market. The chilled seafood sector continues to take the largest share of the multiple retail seafood market with a wide range of segments and species. It is the only seafood sector in growth since Opportunities to grow the category exist around product formats, flavours, mission and channel. This document will examine the detail behind the performance of the chilled seafood sector, specifically: Historic retail seafood sector trends Current seafood sector performance Chilled seafood KPIs Chilled seafood segment performance Chilled seafood species performance Chilled seafood shopper Chilled seafood shopper missions Chilled seafood channels.

2 Historic Retail Seafood Sector Trends Chilled seafood has grown in popularity with British retail shoppers over the past 20 years. In the late 1990 s both the volume and value of chilled seafood began to rise faster than that of frozen seafood. By 2005, chilled seafood had overtaken frozen seafood in volume sales. Overall GB seafood consumption had been growing slowly but steadily until recession hit in 2007, when the relatively high price of seafood meant it struggled to compete with cheaper proteins. From 2007, seafood in multiple retail experienced a sustained period of inflation and price driven growth as consumption fell. Around 2009, retail shoppers became polarized, saving money where possible on basics, but not averse to spending more on quality. Austerity focused shoppers prioritised value for money, and the perceived superior freshness, health and quality of chilled seafood resulted in continued growth of the chilled sector at the expense of frozen and ambient, despite it being double the average price. In October 2016, total seafood, which includes chilled, frozen and ambient varieties, finally returned to full growth for a short period before volume returned to decline in January Current Seafood Sector Performance Seafish has detailed EPOS data (Electronic Point of Sale) available for the past nine years, which can be used to get a longterm picture of the changes in the seafood sectors, segments and species. In March 2017, total GB retail seafood sales were worth 3.14bn (+0.7%), with a volume of 327,004 tonnes (-0.8%) and an average price of 9.60/kg (+1.5%) (Nielsen Scantrack: 52 weeks to excludes discounters). Over the nine years from 2008 to March 2017, total seafood has been in price driven growth, with volume down by -16% and value up by 16%, pushing average price up by 18%. Sector Value Share of Seafood

respectively; with an average price of 13.15/kg (0.3%). This represents a 64.4% share of the seafood retail market by value and 47.1% by volume.")

3 Chilled Seafood Chilled seafood continued to dominate the GB seafood retail market in 2017, with value and volume worth 2.02bn (+1.4%) and 153,893 tonnes (+1.8%) respectively; with an average price of 13.15/kg (0.3%). This represents a 64.4% share of the seafood retail market by value and 47.1% by volume. Over the nine years from 2008 to 2017, chilled seafood increased its retail volume share by 31.9%, whilst frozen and ambient have decreased by -8.3% and -29% respectively. Chilled Seafood KPIs In 2017, there was an increase in the number of shoppers buying chilled seafood despite price increases. Chilled seafood KPIs (key performance indicators), as set out in this table, show penetration is high, with 81.6% of shoppers buying chilled seafood. Compared with the previous year, more shoppers bought chilled seafood, more often, but with smaller baskets. Chilled seafood shoppers bought on average 0.4kg of chilled fish per trip spending 4.39; and bought chilled seafood 20.3 times per year, spending a total of 88.80, equating to 7.8kg/yr. Chilled Seafood Segment Performance It is the chilled natural segment (i.e. includes no additional ingredients), which takes the largest share by both volume (46%) and value (58%) of the chilled seafood sector. By driving long term growth in this sector, chilled natural ultimately drives the GB seafood market; being worth more than the total frozen and total ambient seafood sectors combined. Segment Share of Chilled 2017 (Value) Chilled prepared (14%), chilled meals (8%) and chilled sauce (6%) are ranked second, third and fourth, respectively by value share. In the 52wks to 25th March 2017, chilled natural was worth 1.18bn (+0.1%), with 71,325 (-0.5%) tonnes. Over the long term (9yrs to 25th March 2017) chilled meals, natural, breaded, cakes, sushi and fingers have all been in growth; chilled fingers achieving a 334% increase in volume, albeit starting from a small base. Chilled sectors in decline over the same period included chilled prepared, sauce and batter. Long & Short Term Segment Volume Trends 2017 Over the short term (52 wks. to 25th March 2017), it is the meals, sauce, sushi, dusted and batter segments that have been in volume growth. Dusted (a recently coded segment) continues to show strong volume and value growth, being perceived as a healthier and flavoursome alternative to breaded and battered. Chilled breaded and fingers were in volume decline. 3

displacing cold water prawns (7.3%).")

4 Chilled Seafood Segment Performance 2015 to 2017 Chilled Seafood Species Salmon dominates the chilled seafood sector with a 46% value share of the top species, selling nearly four times its nearest competitor in both volume and value. Smoked salmon makes up 36% of total chilled salmon sales by value. Chilled warm water prawns recently displaced cod as the second most popular species with 11.5% value share, followed closely by cod (10.5%), haddock (8.3%) and mixed seafood (8.0%) displacing cold water prawns (7.3%). The consumption of traditional whitefish species has been in steady decline since the 1980s, whilst salmon and other aquaculture seafood species have grown in popularity. Chilled salmon sales continued to grow through the recession despite being over 40% more expensive per kg than cod in March Lower prices and improved availability have driven cod consumption in recent years. Chilled whitefish consumption fell -62% from 1980 to 2015, compared to chilled salmon up 293% (ref Defra family food). In the 52wks to 25th March 2017, chilled cod was worth 179m, with 14,798 tonnes. Since 2008, its volume and value increased by 40% and 23% respectively. Over the long term (9yrs to 25th March 2017) the top four species, salmon, warm water prawns, cod and haddock were in full (volume and value) growth. Seabream, seabass and crab grew by over 100% from a small base. Over the same period, cold water prawns and mackerel were in volume decline, whilst mixed seafood, tuna and trout were in full decline. Price changes have influenced the majority of species trends since 2008, where significant price increases have impacted negatively on volume sales. The main exceptions to this are chilled salmon and warm water prawns where consumption has continued to increase despite double-digit price increases. 4

.")

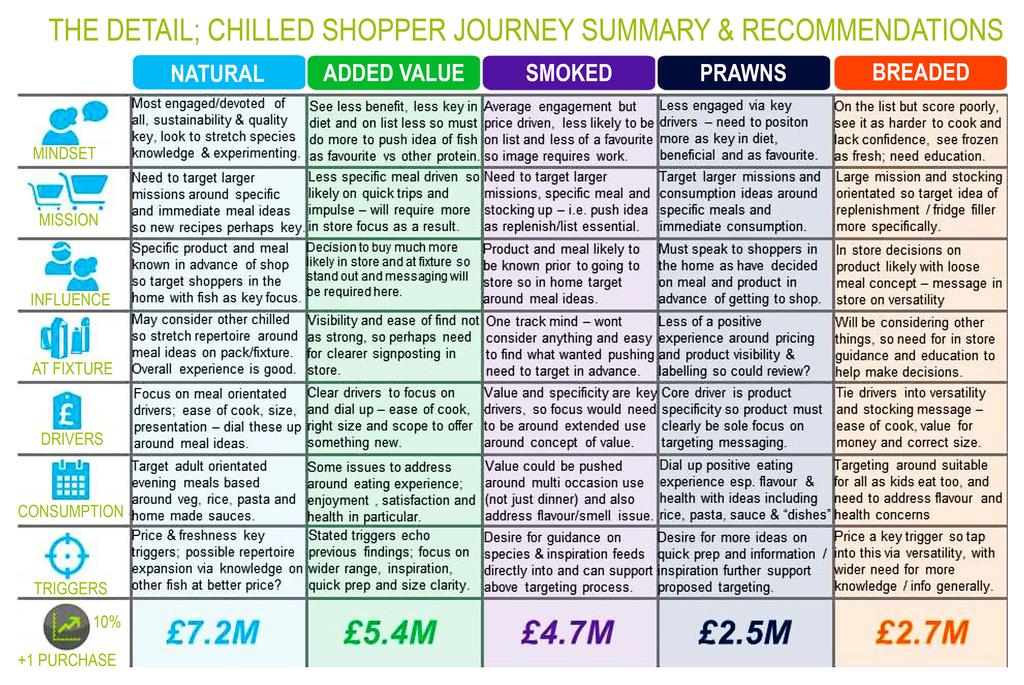

5 Most of the top 10 chilled species have experienced double digit inflation when compared to nine years ago, notably mixed seafood (+85%) and cold water prawns (+54%). Only cod, haddock and sole showed a decrease in average price. In the short term, (52wks to 25th March 2017), most chilled species were in full growth, with the exception of cold water prawns, mackerel and trout. The Chilled Seafood Shopper Seafish commissioned Kantar to carry out two studies to determine why, how, when and where people buy seafood (shopper journey and mission/channel). Combined with previous Seafish shopper research and the Institute of Grocery Distribution IGD benchmarking of the seafood shopper, the insight can then be used to guide new product development (NPD), marketing and sales strategy. For seafood the shopper is usually also the consumer, although, there are some disconnects around seafood products aimed at children - for example, coated fish shapes. One reason for the continued growth of chilled seafood despite its relatively high average price may be down to a strong shopper focus on value for money. Shoppers and consumers perceive chilled and frozen seafood very differently. Chilled seafood is seen as healthier, fresher, better tasting, higher quality and easier to cook than frozen; and is typically bought with a treat or special occasion in mind. Chilled seafood shoppers are generally more engaged and knowledgeable about seafood and surrounding issues such as sustainability. In comparison, frozen seafood is seen as a convenient, cupboard and shopping list staple. Top 5 Attributes Shoppers Use To Identify Higher Quality 5

.")

couples and singles, typically in two person households without children present. Where children are present they are typically aged 5-10 yrs.")

6 Shoppers comment on mushy texture, loss of flavour and struggle with the concept of how frozen seafood can still be fresh and dislike not being able to see the product through the packaging. Chilled meat and fish products labelled British or locally produced are being increasingly associated with better quality (54% Jun 16 vs 42% Jun 15). (IGD) Nielsen demographics describe the chilled seafood shopper as more affluent than the average seafood buyer, but in all other respects they are very similar. Chilled seafood shoppers are predominantly, older (45-64) couples and singles, typically in two person households without children present. Where children are present they are typically aged 5-10 yrs. Top 5 purchase drivers for Chilled Seafood (% of Shoppers that claim it is important) IGD surveys suggest chilled seafood shopper as being unique compared to the typical seafood buyer in being predominantly male and more affluent. When living in a household with young children, the seafood is usually eaten by the shopper only. This unique profile of the chilled seafood shopper opens up a whole host of male targeted flavours, cross-site promotions and marketing opportunities. Health and quality are almost as important to chilled fish shoppers as price with 64% of shoppers claiming it is worth paying extra for higher quality. The Chilled Shopper Mission The Shopper Mission is simply the reason for the shopping trip. The main shop is the key mission for chilled seafood shoppers (39.5%), followed by a top up shop (35.1%). Chilled seafood is most often bought on a pre-planned or impulse meal for tonight mission, intended for immediate consumption or later that same day. This pattern occurs less with other proteins. For the chilled seafood shopper, the decision to buy is Key IGD Chilled Fish Insight and Opportunities more likely to be influenced in store, often with a specific meal in mind and the seafood purchase is likely to influence the other ingredients; offering opportunities for instore shopper marketing, promotions and fixture (point of sale). 6

then discounters and convenience stores.")

7 Chilled Seafood Channels Supermarkets (main estate) are the primary channel for chilled seafood. Around 80% of shoppers use main estate to buy chilled seafood, followed by larger format stores (hypermarkets) then discounters and convenience stores. But, the main estate channel is in decline, with shoppers turning to convenience and online in recent years. The challenge is to grow seafood in these strongly performing channels. Online used to be more attractive to frozen and ambient seafood shoppers, but over a five year period online has seen positive growth across all chilled seafood channels. Chilled natural seafood performed the strongest growing online sales by over 16m in the five years to May The growing convenience channel offers the greatest potential for chilled seafood. Successful products should focus on quality, taste, health and convenience; utilising smaller formats and trending flavours. Cross-linked promotions would target wine and healthy accompaniments including fresh vegetables. Chilled Seafood Growth in Online (Value change 000 5Yrs to Kantar) Purchase The shopper view of the chilled seafood fixture is generally positive. Shoppers favour fixtures that are easy to navigate, where products are attractively presented and easy to find and pricing is EDLP (Everyday Low Pricing). If a specific chilled seafood is not available, shoppers may be tempted to buy another chilled option, but are less likely to accept either frozen or ambient as a substitute: hence ensuring stock on shelf is important to retain the sale. The key to successful seafood products in online is meeting the need for larger format, tasty, filling and healthy mid-week evening meal solutions. General purchase drivers favour products that are easy to cook, with chilled seafood shoppers specifically looking for attractive packaging and product, alongside packs of a convenient size. The trend for polarisation in household size towards single households and larger households could be used to steer pack size strategy. 7

are smell and presentation of fish with eyes and heads.")

.")

8 Seafood shoppers want more recipe inspiration, but report being intimidated by asking an instore fishmonger. The percentage of pre-packaged seafood has grown strongly in recent years. In 2017, 93% of seafood was sold in prepack, rather than from the counter. The chilled shopper has a strong desire for more inspiration, is more open to trying new species and is more receptive to messaging around provenance and responsible sourcing. Key barriers to purchase at fixture (point of sale) are smell and presentation of fish with eyes and heads. Therefore retailers should ensure the fish has sufficient freshness quality to prevent unpleasant odours. Shoppers are unsure on portion size and how to choose fish with adequate freshness quality; in addition they are put off trying new species due to the fear of wastage. Chilled seafood shoppers are much more open to browsing the category compared to chilled meat shoppers (IGD); opening up significant opportunity to educate the shopper and brighten the seafood shopping experience. This could take the form of guides or an interactive fixture; or cross siting to bring together key recipe ingredients into one place to make it easier for the shopper. Recently, the grocery landscape has been shifting to a position of simplicity; the number of stock keeping units (SKUs) at fixture being pared down to the core lines that perform well; and the complexity of the multitude of different types of promotions are being cut and simplified in favour of total price reduction (TPR). In 2015 the dominant chilled fish promotional mechanic was strongly Y for x with TPR promotions at only around 23% by volume. Better performing promotions for chilled fish may be the meal deals and crosslinked promotions with key ingredients. Eating Chilled seafood is typically eaten by adults at a dinner/tea occasion, although lunch features more for chilled seafood than other formats. Chilled seafood shoppers are split in that some find it hard to cook well, whilst others find it easy to cook. Many are put off by handling and preparing the seafood, uncertainty over cooking time and perceived safety issues. Again the greatest barriers are unpleasant smell and overly fishy flavours, which are both indicators of low freshness quality. Another big turn off for shoppers is the fear of bones. When it comes to accompaniments, chilled seafood is most likely to be eaten with salad. Key flavour trends filtering down from foodservice remain as American/ South American (especially Mexican) and Far Eastern. Key flavours are lemon, garlic and chilli. Growing formats are smoked, sushi and poke a Hawaiian raw fish salad superfood. 8

9 9

10 Data: Retail data: AC Nielsen Scantrack/Homescan: 52 weeks to March 25th 2017 (Scantrack excludes discounters and seafood sandwiches) (%) values represent change from the previous year unless otherwise stated Kantar World Panel Seafood Shopper Journey Report 2015 Kantar World Panel Seafood Channel Report 2016 Defra Family Food Survey 2015 IGD 2016 Category Benchmarks IGD Quality in Focus 2016 Update More Information: For the full range of market insight factsheets, covering different sectors of the seafood industry go to the Seafish website - Information and insight is available free of charge for levy paying seafood businesses. Click here to subscribe for the monthly market e-alert, and secure report access Richard Watson Seafish Origin Way, Europarc, Grimsby DN37 9TZ T: +44 (0) F: (0) e: info@seafish.co.uk w: Our Mission: supporting a profitable, sustainable and socially responsible future for the seafood industry 10

Chilled Seafood in Multiple Retail (2018)

") Market Insight Factsheet Chilled Seafood in Multiple Retail () This factsheet provides a summary of the performance of the chilled seafood sector in the multiple retail seafood market up to June. The chilled

Market Insight Factsheet Chilled Seafood in Multiple Retail () This factsheet provides a summary of the performance of the chilled seafood sector in the multiple retail seafood market up to June. The chilled

Frozen Seafood in Multiple Retail Market Insight Factsheet

Market Insight Factsheet Frozen Seafood in Multiple Retail 2017 Frozen seafood has been in decline since 2007, with frozen sauce and frozen seafood meals being the hardest hit, losing over -50% volume.

Market Insight Factsheet Frozen Seafood in Multiple Retail 2017 Frozen seafood has been in decline since 2007, with frozen sauce and frozen seafood meals being the hardest hit, losing over -50% volume.

Seafood in Multiple Retail (2018)

") Market Insight Factsheet Seafood in Multiple Retail () This factsheet provides a summary of the performance of seafood in the multiple retail seafood category up to June. Over the past 10 years, total

Market Insight Factsheet Seafood in Multiple Retail () This factsheet provides a summary of the performance of seafood in the multiple retail seafood category up to June. Over the past 10 years, total

Seafood Consumption (2017 Update)

") Seafood Industry Factsheet Seafood Consumption (2017 Update) There are three methods available to measure and track GB seafood consumption which provide slightly different yet similar figures; whilst useful

Seafood Industry Factsheet Seafood Consumption (2017 Update) There are three methods available to measure and track GB seafood consumption which provide slightly different yet similar figures; whilst useful

CLG: Seafood Consumption. Richard Watson Seafish

CLG: Seafood Consumption Richard Watson Seafish Agenda Seafish Insight Service Benchmark Consumption Trends Trend Drivers Growing Seafood Consumption Market Insight Service Provide 250 reports per year

CLG: Seafood Consumption Richard Watson Seafish Agenda Seafish Insight Service Benchmark Consumption Trends Trend Drivers Growing Seafood Consumption Market Insight Service Provide 250 reports per year

Seafood. Consumption. Seafood Industry Factsheet. Market overview:

Seafood Industry Factsheet Seafood Consumption Market overview: In the UK, shoppers and consumers have a unique relationship with seafood. Unlike most other European countries, seafood can be a daunting

Seafood Industry Factsheet Seafood Consumption Market overview: In the UK, shoppers and consumers have a unique relationship with seafood. Unlike most other European countries, seafood can be a daunting

Haddock. Seafood Industry Factsheet. Market overview: haddock

Seafood Industry Factsheet Haddock Market overview: haddock The UK s supply of haddock (Melanogrammus aeglefinus) relies on imports and domestic landings by the UK fleet. Haddock is popular in both retail

Seafood Industry Factsheet Haddock Market overview: haddock The UK s supply of haddock (Melanogrammus aeglefinus) relies on imports and domestic landings by the UK fleet. Haddock is popular in both retail

Market Insight Factsheet. Haddock (2018 Update)

") Market Insight Factsheet Haddock (2018 Update) Market Overview: This factsheet provides a summary of the UK value chain for haddock. It is intended to inform stakeholders of the UK seafood industry about

Market Insight Factsheet Haddock (2018 Update) Market Overview: This factsheet provides a summary of the UK value chain for haddock. It is intended to inform stakeholders of the UK seafood industry about

Fish and Chips in Commercial Foodservice 2016 JULIA BROOKS, JANUARY 2017

Fish and Chips in Commercial Foodservice 2016 JULIA BROOKS, JANUARY 2017 INTRODUCTION Since the mid nineteenth century fish and chips have built their position as being a symbol of the UK s culinary culture

Fish and Chips in Commercial Foodservice 2016 JULIA BROOKS, JANUARY 2017 INTRODUCTION Since the mid nineteenth century fish and chips have built their position as being a symbol of the UK s culinary culture

Bottled Water Category Overview

Bottled Water Category Overview 2014-2015 Disclaimer The following information is offered in good faith and represents an unqualified interpretation of a range of industry commentary and market data. It

Bottled Water Category Overview 2014-2015 Disclaimer The following information is offered in good faith and represents an unqualified interpretation of a range of industry commentary and market data. It

Bag In Box Consumer Preferences in the UK. Presented during the Performance BIB meetings in Bristol, England 24 & 25 October 2012

Bag In Box Consumer Preferences in the UK Presented during the Performance BIB meetings in Bristol, England 24 & 25 October 2012 By: Katie Mollet, Wine Buyer Bag in Box is worth 579m each year, that s

Bag In Box Consumer Preferences in the UK Presented during the Performance BIB meetings in Bristol, England 24 & 25 October 2012 By: Katie Mollet, Wine Buyer Bag in Box is worth 579m each year, that s

TOTAL STORE CONNECTIVITY: REVEALING NEW PATHWAYS TO WIN SPECIALTY CHEESE

TOTAL STORE CONNECTIVITY: REVEALING NEW PATHWAYS TO WIN SPECIALTY CHEESE International Dairy Deli Bakery Association In partnership with Nielsen Perishables Group May, 2015 AGENDA Study Objectives 3 Deli

TOTAL STORE CONNECTIVITY: REVEALING NEW PATHWAYS TO WIN SPECIALTY CHEESE International Dairy Deli Bakery Association In partnership with Nielsen Perishables Group May, 2015 AGENDA Study Objectives 3 Deli

Must stocks. Market Trends. Increase your footfall. Improve your sales. Market insight. Retail planograms. New products Top sellers

Improve your sales Market Trends New products Top sellers Market insight Must stocks Increase your footfall Retail planograms www.bestway.co.uk www.batleys.co.uk MARKET INSIGHT Canned and packaged food

Improve your sales Market Trends New products Top sellers Market insight Must stocks Increase your footfall Retail planograms www.bestway.co.uk www.batleys.co.uk MARKET INSIGHT Canned and packaged food

IMPORTANCE OF LODI WINES IN THE RETAIL CHANNEL AND OPPORTUNITIES FOR GROWTH. Curtis Mann Director of Wine & Beverage Raley s Family of Fine Stores

IMPORTANCE OF LODI WINES IN THE RETAIL CHANNEL AND OPPORTUNITIES FOR GROWTH Curtis Mann Director of Wine & Beverage Raley s Family of Fine Stores Raley s Overview 3 Billion Dollar Company 120 Stores across

IMPORTANCE OF LODI WINES IN THE RETAIL CHANNEL AND OPPORTUNITIES FOR GROWTH Curtis Mann Director of Wine & Beverage Raley s Family of Fine Stores Raley s Overview 3 Billion Dollar Company 120 Stores across

Media Feedback 2015 Category Quantification Report White Milk in South Africa

Media Feedback 2015 Category Quantification Report White Milk in South Africa Product Definitions Product Pasteurised Milk ESL (Extended Shelf Life) Milk Sterilised Milk Definition Milk is heated in one

Media Feedback 2015 Category Quantification Report White Milk in South Africa Product Definitions Product Pasteurised Milk ESL (Extended Shelf Life) Milk Sterilised Milk Definition Milk is heated in one

The Future Tortilla Market: Organic, Ancient Grains, Transitional

The Future Tortilla Market: Organic, Ancient Grains, Transitional THE EVOLUTION OF VALUE CREATION FROM CONSUMER TO GRAINS Macro Exposures Consumer Values Consumer Trends Customer Responses Category Value

The Future Tortilla Market: Organic, Ancient Grains, Transitional THE EVOLUTION OF VALUE CREATION FROM CONSUMER TO GRAINS Macro Exposures Consumer Values Consumer Trends Customer Responses Category Value

MANGO PERFORMANCE BENCHMARK REPORT

MANGO PERFORMANCE BENCHMARK REPORT 2015-2016 TABLE OF CONTENTS Page 3 Page 5 Page 12 Page 15 Page 27 Page 36 Page 46 Approach and Data Set Parameters Overview and Mango Trend-Spotting Fruit and Tropical

MANGO PERFORMANCE BENCHMARK REPORT 2015-2016 TABLE OF CONTENTS Page 3 Page 5 Page 12 Page 15 Page 27 Page 36 Page 46 Approach and Data Set Parameters Overview and Mango Trend-Spotting Fruit and Tropical

Mango Retail Performance Report 2017

Mango Retail Performance Report 2017 1 Table of Contents Pages 3-9 Pages 10-15 Pages 16-34 Pages 35-44 Pages 45-51 Pages 52-54 Executive Summary Fruit and Tropical Fruit Performance Whole Mango Performance

Mango Retail Performance Report 2017 1 Table of Contents Pages 3-9 Pages 10-15 Pages 16-34 Pages 35-44 Pages 45-51 Pages 52-54 Executive Summary Fruit and Tropical Fruit Performance Whole Mango Performance

Jason McNally. 21 st of April 2009

Coffee & Food On the Go How to maximise your Profits! Jason McNally Dubai 21 st of April 2009 Agenda Cafe Culture Convenience Retailing Coffee to Go Simply Coffee Food to Go Summary Questions COFFEE &

Coffee & Food On the Go How to maximise your Profits! Jason McNally Dubai 21 st of April 2009 Agenda Cafe Culture Convenience Retailing Coffee to Go Simply Coffee Food to Go Summary Questions COFFEE &

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S.

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Voluntary - Public Date: 4/24/2013 GAIN Report Number:

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Voluntary - Public Date: 4/24/2013 GAIN Report Number:

Issue No. 7 SPOTLIGHT THE PHILIPPINES

Issue No. 7 2 Greetings! Foreword Alex Duterrage General Manager for Kantar Worldpanel Philippines Health & wellness have been one of the trending topics across the world. Zooming into the Philippines,

Issue No. 7 2 Greetings! Foreword Alex Duterrage General Manager for Kantar Worldpanel Philippines Health & wellness have been one of the trending topics across the world. Zooming into the Philippines,

Welcome to the. Find out more about the parts of the world where SIAL Network is established, thanks to the Euromonitor s study.

Welcome to the Find out more about the parts of the world where SIAL Network is established, thanks to the Euromonitor s study. SELECT A REGION TO SEE THE REPORT Canada China Indonesia Middle East & Africa

Welcome to the Find out more about the parts of the world where SIAL Network is established, thanks to the Euromonitor s study. SELECT A REGION TO SEE THE REPORT Canada China Indonesia Middle East & Africa

US Chicken Consumption. Presentation to Chicken Marketing Summit July 18, 2017 Asheville, NC

US Chicken Consumption Presentation to Chicken Marketing Summit July 18, 2017 Asheville, NC Primary research sponsor Contributing research sponsors Research findings presented by OBJECTIVES Analyze chicken

US Chicken Consumption Presentation to Chicken Marketing Summit July 18, 2017 Asheville, NC Primary research sponsor Contributing research sponsors Research findings presented by OBJECTIVES Analyze chicken

Shellfish and bivalve markets in the UK

Shellfish and bivalve markets in the UK JULIA BROOKS, MARKET INSIGHT ANALYST, SEAFISH Sources: CEFAS 2015, MMO UK And Foreign Vessels Landings By UK Port And UK Vessel Landings Abroad Underlying Dataset

Shellfish and bivalve markets in the UK JULIA BROOKS, MARKET INSIGHT ANALYST, SEAFISH Sources: CEFAS 2015, MMO UK And Foreign Vessels Landings By UK Port And UK Vessel Landings Abroad Underlying Dataset

MILLENNIAL CONSUMERS SEEK NEW TASTES, WILLING TO PAY A PREMIUM FOR ALCOHOLIC BEVERAGES. Nielsen Releases Most Comprehensive Study To Date

The Nielsen Company 150 North Martingale Road Schaumburg, IL 60173-2076 www.nielsen.com News Release CONTACT: Jennifer Frighetto, 847-605-5686 jennifer.frighetto@nielsen.com FOR IMMEDIATE RELEASE MILLENNIAL

The Nielsen Company 150 North Martingale Road Schaumburg, IL 60173-2076 www.nielsen.com News Release CONTACT: Jennifer Frighetto, 847-605-5686 jennifer.frighetto@nielsen.com FOR IMMEDIATE RELEASE MILLENNIAL

2013 Annual Quantification Report: Media Feedback Report Coffee in South Africa

2013 Annual Quantification Report: Media Feedback Report Coffee in South Africa 30 September 2013 Product Definitions Wine Pure Ground Pure Instant Mixed Ground Mixed Instant Definition This product comprises

2013 Annual Quantification Report: Media Feedback Report Coffee in South Africa 30 September 2013 Product Definitions Wine Pure Ground Pure Instant Mixed Ground Mixed Instant Definition This product comprises

Must stocks. Market Trends. Increase your footfall. Improve your sales. Market insight. Retail planograms. New products Top sellers

Improve your sales Market Trends New products Top sellers Market insight Must stocks Increase your footfall Retail planograms www.bestway.co.uk www.batleys.co.uk MARKET INSIGHT Own Label has a 24% share

Improve your sales Market Trends New products Top sellers Market insight Must stocks Increase your footfall Retail planograms www.bestway.co.uk www.batleys.co.uk MARKET INSIGHT Own Label has a 24% share

CATEGORY INSIGHT REPORT

20 17 CATEGORY INSIGHT REPORT A NEW DAY IN BREAKFAST A host of reasons show that the breakfast category is primed for clear growth and product exploration. A major opportunity in the space: Consumers as

20 17 CATEGORY INSIGHT REPORT A NEW DAY IN BREAKFAST A host of reasons show that the breakfast category is primed for clear growth and product exploration. A major opportunity in the space: Consumers as

Category ADVICE.

2018 www.bestway.co.uk www.batleys.co.uk MARKET INSIGHT Hot Snacks over index in UK Impulse, making it 3 times more important to the convenience shopper (Nielsen Apr 2018) The Instant Hot Snacks market

2018 www.bestway.co.uk www.batleys.co.uk MARKET INSIGHT Hot Snacks over index in UK Impulse, making it 3 times more important to the convenience shopper (Nielsen Apr 2018) The Instant Hot Snacks market

Consumer Insights. Chewy Candy. Empowering Manufacturers and Retailers for Category 1 Growth

Consumer Insights Chewy Candy Empowering Manufacturers and Retailers for Category 1 Growth NCA Sweet Insights Contributing Partners The NPD Group SymphonyIRI The Futures Group The Capre Group 2 Why NCA

Consumer Insights Chewy Candy Empowering Manufacturers and Retailers for Category 1 Growth NCA Sweet Insights Contributing Partners The NPD Group SymphonyIRI The Futures Group The Capre Group 2 Why NCA

Retail Best Practices Study

Retail Best Practices Study Initial Findings January 2009 Study conducted by The Mushroom Council and Encore Associates 1 Objective Table of Contents Executive Summary Mushrooms Value to Retailers Best

Retail Best Practices Study Initial Findings January 2009 Study conducted by The Mushroom Council and Encore Associates 1 Objective Table of Contents Executive Summary Mushrooms Value to Retailers Best

KOREA MARKET REPORT: FRUIT AND VEGETABLES

KOREA MARKET REPORT: FRUIT AND VEGETABLES 주한뉴질랜드대사관 NEW ZEALAND EMBASSY SEOUL DECEMBER 2016 Page 2 of 6 Note for readers This report has been produced by MFAT and NZTE staff of the New Zealand Embassy

KOREA MARKET REPORT: FRUIT AND VEGETABLES 주한뉴질랜드대사관 NEW ZEALAND EMBASSY SEOUL DECEMBER 2016 Page 2 of 6 Note for readers This report has been produced by MFAT and NZTE staff of the New Zealand Embassy

Fresh Produce Report. P13: 12 w/e 3rd January Kantar Worldpanel

Fresh Produce Report P13: 12 w/e 3rd January 2016 1 HOW IS TOTAL PRODUCE PERFORMING? Total Produce is worth 2.1bn and is growing by 4.1% compared to the same period last year. Much of this is driven by

Fresh Produce Report P13: 12 w/e 3rd January 2016 1 HOW IS TOTAL PRODUCE PERFORMING? Total Produce is worth 2.1bn and is growing by 4.1% compared to the same period last year. Much of this is driven by

THE POWER OF BAKERY CATEGORIES

THE POWER OF BAKERY CATEGORIES Todd Hale Retail Insights Thought Leader Principal, Todd Hale, LLC March 30, 2015 DRIVING GROWTH IN DYNAMIC TIMES Staying connected with winning retailers & categories Engaging

THE POWER OF BAKERY CATEGORIES Todd Hale Retail Insights Thought Leader Principal, Todd Hale, LLC March 30, 2015 DRIVING GROWTH IN DYNAMIC TIMES Staying connected with winning retailers & categories Engaging

Premium Ale INSIGHT REPORT. Hall & Woodhouse Premium Ale Insight Report 2016

Premium Ale INSIGHT REPORT 2016 Contents 02 Introduction:...03 Category Overview:...04 Beers, Wines & Spirits Performance Beer Category Trends Premium Ale Performance & Trends Deflation:...14 Impact of

Premium Ale INSIGHT REPORT 2016 Contents 02 Introduction:...03 Category Overview:...04 Beers, Wines & Spirits Performance Beer Category Trends Premium Ale Performance & Trends Deflation:...14 Impact of

COMMITTEE ON COMMODITY PROBLEMS INTERGOVERNMENTAL GROUP ON TEA NINETEENTH SESSION. New Delhi, India, May 2010

May 2010 CCP:TE 10/CRS 19 E COMMITTEE ON COMMODITY PROBLEMS INTERGOVERNMENTAL GROUP ON TEA NINETEENTH SESSION New Delhi, India, 12 14 May 2010 MARKET DEVELOPMENTS IN SELECTED COUNTRIES INDIA Indian Tea-

May 2010 CCP:TE 10/CRS 19 E COMMITTEE ON COMMODITY PROBLEMS INTERGOVERNMENTAL GROUP ON TEA NINETEENTH SESSION New Delhi, India, 12 14 May 2010 MARKET DEVELOPMENTS IN SELECTED COUNTRIES INDIA Indian Tea-

Challenges in Fluid Milk Consumption. October 25, 2017

Challenges in Fluid Milk Consumption October 25, 2017 Increased Competition At Store 1970 s Milk Soft Drinks Coffee Juice 1980 s Milk Soft Drinks Coffee Juice Bottled water RTD juice Teas 1990 s Milk Soft

Challenges in Fluid Milk Consumption October 25, 2017 Increased Competition At Store 1970 s Milk Soft Drinks Coffee Juice 1980 s Milk Soft Drinks Coffee Juice Bottled water RTD juice Teas 1990 s Milk Soft

2017 FINANCIAL REVIEW

2017 FINANCIAL REVIEW In addition to activity, strategy, goals, and challenges, survey respondents also provided financial information from 2014, 2015, and 2016. Select results are provided below: 2016

2017 FINANCIAL REVIEW In addition to activity, strategy, goals, and challenges, survey respondents also provided financial information from 2014, 2015, and 2016. Select results are provided below: 2016

CARBONATED SOFT DRINKS

International Markets Bureau AMERICAN EATING TRENDS REPORT CARBONATED SOFT DRINKS Unless otherwise stated, all of the information in this report was derived from the NPD Group s National Eating Trends

International Markets Bureau AMERICAN EATING TRENDS REPORT CARBONATED SOFT DRINKS Unless otherwise stated, all of the information in this report was derived from the NPD Group s National Eating Trends

Weekday Meal Repertoire

Weekday Meal Repertoire Results from Omnibus research - February 2007 Prepared by The Oxford Partnership for The British Potato Council Introduction and background In 2006 The Oxford Partnership was commissioned

Weekday Meal Repertoire Results from Omnibus research - February 2007 Prepared by The Oxford Partnership for The British Potato Council Introduction and background In 2006 The Oxford Partnership was commissioned

The Frozen Aisle Market Drivers & Trends ALWAYS INSPIRING MORE

The Frozen Aisle Market Drivers & Trends ALWAYS INSPIRING MORE MARKET DRIVERS > The cost of ingredients is making it tougher for manufacturers to hold the line on prices. > The impact of the recession

The Frozen Aisle Market Drivers & Trends ALWAYS INSPIRING MORE MARKET DRIVERS > The cost of ingredients is making it tougher for manufacturers to hold the line on prices. > The impact of the recession

The Vietnam urban food consumption and expenditure study

The Centre for Global Food and Resources The Vietnam urban food consumption and expenditure study Factsheet 4: Where do consumers shop? Wet markets still dominate! The food retail landscape in urban Vietnam

The Centre for Global Food and Resources The Vietnam urban food consumption and expenditure study Factsheet 4: Where do consumers shop? Wet markets still dominate! The food retail landscape in urban Vietnam

Report Brochure P O R T R A I T S U K REPORT PRICE: GBP 2,500 or 5 Report Credits* UK Portraits 2014

Report Brochure P O R T R A I T S U K 2 0 1 4 REPORT PRICE: GBP 2,500 or 5 Report Credits* Wine Intelligence 2013 1 Contents 1 MANAGEMENT SUMMARY >> An introduction to UK Portraits, including segment size,

Report Brochure P O R T R A I T S U K 2 0 1 4 REPORT PRICE: GBP 2,500 or 5 Report Credits* Wine Intelligence 2013 1 Contents 1 MANAGEMENT SUMMARY >> An introduction to UK Portraits, including segment size,

New from Packaged Facts!

New from Packaged Facts! FOODSERVICE MARKET INSIGHTS A fresh perspective on the foodservice marketplace Essential Insights on Consumer customerservice@packagedfacts.com (800) 298-5294 (240) 747-3095 (Intl.)

New from Packaged Facts! FOODSERVICE MARKET INSIGHTS A fresh perspective on the foodservice marketplace Essential Insights on Consumer customerservice@packagedfacts.com (800) 298-5294 (240) 747-3095 (Intl.)

The Power of Meat 2016 An in-depth look at the meat department through the shoppers eyes

Brought to you by: The Power of Meat 2016 An in-depth look at the meat department through the shoppers eyes Presented by: Anne-Marie Roerink Study made possible by: The Power of Meat 2016 1 Meat = prime

Brought to you by: The Power of Meat 2016 An in-depth look at the meat department through the shoppers eyes Presented by: Anne-Marie Roerink Study made possible by: The Power of Meat 2016 1 Meat = prime

An update from the Competitiveness and Market Analysis Branch, Alberta Agriculture and Forestry.

An update from the Competitiveness and Market Analysis Branch, Alberta Agriculture and Forestry. The articles in this series includes information on what consumers are buying and why they are buying it.

An update from the Competitiveness and Market Analysis Branch, Alberta Agriculture and Forestry. The articles in this series includes information on what consumers are buying and why they are buying it.

Final Report. The Lunchtime Occasion in Republic of Ireland and Great Britain

Final Report The Lunchtime Occasion in Republic of Ireland and Great Britain November 2013 Contents Introduction & Research Objectives... 1 Research Method... 2 Segment Profiles... 3 Executive Summary...

Final Report The Lunchtime Occasion in Republic of Ireland and Great Britain November 2013 Contents Introduction & Research Objectives... 1 Research Method... 2 Segment Profiles... 3 Executive Summary...

TRENDS IN SALES OF MEAT PRODUCTS A RETAIL PERSPECTIVE. Meat Market Observatory 25 June 2018

TRENDS IN SALES OF MEAT PRODUCTS A RETAIL PERSPECTIVE Meat Market Observatory 25 June 2018 Belgium Product category Total pigmeat Price evolution (% change Apr-18 vs Apr-17) Price evolution (% change Jan-Apr

TRENDS IN SALES OF MEAT PRODUCTS A RETAIL PERSPECTIVE Meat Market Observatory 25 June 2018 Belgium Product category Total pigmeat Price evolution (% change Apr-18 vs Apr-17) Price evolution (% change Jan-Apr

Matt Southam. Multiple Retail Trade Sector Manager

Matt Southam Multiple Retail Trade Sector Manager Identify Problem Area Consumer Insight Devise Solutions Innovation examples Meet new needs (Popcorn) Meet new occasions (Belvita) Attract new consumers

Matt Southam Multiple Retail Trade Sector Manager Identify Problem Area Consumer Insight Devise Solutions Innovation examples Meet new needs (Popcorn) Meet new occasions (Belvita) Attract new consumers

UK Berry Market. Dr Drew Reynolds Total Produce

UK Berry Market Dr Drew Reynolds Total Produce Introduction To Total Produce Our Group In Numbers People 5000+ Cartons of produce distributed annually 340m+ Operating Facilities 120+ Sales 3.45bn Countries

UK Berry Market Dr Drew Reynolds Total Produce Introduction To Total Produce Our Group In Numbers People 5000+ Cartons of produce distributed annually 340m+ Operating Facilities 120+ Sales 3.45bn Countries

Awareness, Attitude & Usage Study Executive Summary

Awareness, Attitude & Usage Study Executive Summary 8.4.11 Background The National Pecan Shellers Association (NPSA) is interested in encouraging the consumption of Pecans, particularly increasing the

Awareness, Attitude & Usage Study Executive Summary 8.4.11 Background The National Pecan Shellers Association (NPSA) is interested in encouraging the consumption of Pecans, particularly increasing the

Small Winemaker Production and Sales Survey Report November 2017

Small Winemaker Production and Sales Survey Report 2016-17 November 2017 Wine Australia 2 Summary of findings It is estimated that small winemakers (those crushing up to 500 tonnes) contribute 8 per cent

Small Winemaker Production and Sales Survey Report 2016-17 November 2017 Wine Australia 2 Summary of findings It is estimated that small winemakers (those crushing up to 500 tonnes) contribute 8 per cent

Fairtrade Buying Behaviour: We Know What They Think, But Do We Know What They Do?

Fairtrade Buying Behaviour: We Know What They Think, But Do We Know What They Do? Dr. Fred A. Yamoah Prof. Andrew Fearne Dr. Rachel Duffy Dr. Dan Petrovici Background/Context The UK is a major market for

Fairtrade Buying Behaviour: We Know What They Think, But Do We Know What They Do? Dr. Fred A. Yamoah Prof. Andrew Fearne Dr. Rachel Duffy Dr. Dan Petrovici Background/Context The UK is a major market for

Thailand Packaging Machinery Market. Jorge Izquierdo VP Market Development PMMI

Thailand Packaging Machinery Market Jorge Izquierdo VP Market Development PMMI jizquierdo@pmmi.org www.pmmi.org/global www.pmmi.org/research Today General Economic and Political Highlights Current Packaging

Thailand Packaging Machinery Market Jorge Izquierdo VP Market Development PMMI jizquierdo@pmmi.org www.pmmi.org/global www.pmmi.org/research Today General Economic and Political Highlights Current Packaging

Foodservice perspective

supporting a profitable, sustainable and socially responsible future for the seafood industry Foodservice perspective Julia Brooks, Seafish, 28 September 2016 Sources: Q2 2016 The NPD Group / CREST UK,

supporting a profitable, sustainable and socially responsible future for the seafood industry Foodservice perspective Julia Brooks, Seafish, 28 September 2016 Sources: Q2 2016 The NPD Group / CREST UK,

Wine Trends & the U.S. Consumer Laura Maniec, MS. CVRVV Conference January 10 th & 11 th 2013

Wine Trends & the U.S. Consumer Laura Maniec, MS CVRVV Conference January 10 th & 11 th 2013 Consumer Wine Consumption Core segment of wine drinkers continues to grow, driven mostly by younger Millennials

Wine Trends & the U.S. Consumer Laura Maniec, MS CVRVV Conference January 10 th & 11 th 2013 Consumer Wine Consumption Core segment of wine drinkers continues to grow, driven mostly by younger Millennials

The Portuguese clipfish market 2017

The Portuguese clipfish market 2017 08.02.2018 Johnny Thomassen Fiskeriutsending i Portugal On this presentation we will try to answer: - How is the Portuguese economy doing? - Are the consumer habits

The Portuguese clipfish market 2017 08.02.2018 Johnny Thomassen Fiskeriutsending i Portugal On this presentation we will try to answer: - How is the Portuguese economy doing? - Are the consumer habits

Company name (YUM) Analyst: Roman Sandoval, Niklas Podhraski, Akash Patel Spring Recommendation: Don t Buy Target Price until (12/27/2016): $95

Analyst: Roman Sandoval, Niklas Podhraski, Akash Patel Spring Recommendation: Don t Buy Target Price until (12/27/2016): $95") Recommendation: Don t Buy Target Price until (12/27/2016): $95 1. Reasons for the Recommendation One of the most important reasons why we don t want to buy Yum is the growth prospects of the company in

Recommendation: Don t Buy Target Price until (12/27/2016): $95 1. Reasons for the Recommendation One of the most important reasons why we don t want to buy Yum is the growth prospects of the company in

Seafood in the Foodservice Sector

Seafood in the Foodservice Sector 13 th March 2015 Presented by: Caroline Hughes & Sam Bannister Background to the research Our objectives To understand the barriers to increasing the presence of seafood

Seafood in the Foodservice Sector 13 th March 2015 Presented by: Caroline Hughes & Sam Bannister Background to the research Our objectives To understand the barriers to increasing the presence of seafood

An update from the Competitiveness and Market Analysis Section, Alberta Agriculture and Forestry.

An update from the Competitiveness and Market Analysis Section, Alberta Agriculture and Forestry. The articles in this series includes information on what consumers are buying and why they are buying it.

An update from the Competitiveness and Market Analysis Section, Alberta Agriculture and Forestry. The articles in this series includes information on what consumers are buying and why they are buying it.

U.S. Retail Coffee. Joe Stanziano Senior Vice President and General Manager, Coffee

U.S. Retail Coffee Joe Stanziano Senior Vice President and General Manager, Coffee 1 Our Coffee Vision Build BELOVED COFFEE BRANDS that ignite the senses and inspire passions every day. OUR STRATEGIC PRIORITIES

U.S. Retail Coffee Joe Stanziano Senior Vice President and General Manager, Coffee 1 Our Coffee Vision Build BELOVED COFFEE BRANDS that ignite the senses and inspire passions every day. OUR STRATEGIC PRIORITIES

RESTAURANT OUTLOOK SURVEY

Reference Period: Fourth Quarter 2016 RESTAURANT OUTLOOK SURVEY Prepared by Chris Elliott, Senior Economist January 23, 2017 Q2-2011 Restaurant Outlook Survey Fourth Quarter 2016 1 Highlights The share

Reference Period: Fourth Quarter 2016 RESTAURANT OUTLOOK SURVEY Prepared by Chris Elliott, Senior Economist January 23, 2017 Q2-2011 Restaurant Outlook Survey Fourth Quarter 2016 1 Highlights The share

Veganuary Month Survey Results

Veganuary 2016 6-Month Survey Results Project Background Veganuary is a global campaign that encourages people to try eating a vegan diet for the month of January. Following Veganuary 2016, Faunalytics

Veganuary 2016 6-Month Survey Results Project Background Veganuary is a global campaign that encourages people to try eating a vegan diet for the month of January. Following Veganuary 2016, Faunalytics

Excise Duty on Beer and Cider and Small Breweries Relief

Excise Duty on Beer and Cider and Small Breweries Relief Memorandum to the Chancellor CAMRA, The Campaign for Real Ale March 2006 1 1.0 Executive Summary 1.1 CAMRA calls on the Government to freeze or

Excise Duty on Beer and Cider and Small Breweries Relief Memorandum to the Chancellor CAMRA, The Campaign for Real Ale March 2006 1 1.0 Executive Summary 1.1 CAMRA calls on the Government to freeze or

Country Profile: Bakery & Cereals sector in Indonesia

Country Profile: Bakery & Cereals sector in Indonesia #1157469 $875 156 pages In Stock Report Description Country Profile: Bakery & Cereals sector in Indonesia Summary GlobalDatas Country Profile report

Country Profile: Bakery & Cereals sector in Indonesia #1157469 $875 156 pages In Stock Report Description Country Profile: Bakery & Cereals sector in Indonesia Summary GlobalDatas Country Profile report

Table of Contents. Contact Information

Case Study 2015 Table of Contents The Challenge.......................................................................... 1 Pizza Hut and the U.S. Pizza Market...................................................

Case Study 2015 Table of Contents The Challenge.......................................................................... 1 Pizza Hut and the U.S. Pizza Market...................................................

November 8, 2017 Conference. Creating. Connections And Communities

November 8, 2017 Conference Creating Connections And Communities UNDERSTANDING THE CHANGING CONSUMER In 2017, Canadians will spend $155 Billion on food NPD Eating Patterns in Canada 2017 3 IF YOU REMEMBER

November 8, 2017 Conference Creating Connections And Communities UNDERSTANDING THE CHANGING CONSUMER In 2017, Canadians will spend $155 Billion on food NPD Eating Patterns in Canada 2017 3 IF YOU REMEMBER

Drinks Sector Guide. The global alcoholic drinks market grew by 3.3% in 2014 to reach a value of $1,152,011.1 million.

Drinks Sector Guide Drinks Sector Guide The global alcoholic drinks market grew by 3.3% in 2014 to reach a value of $1,152,011.1 million. Beer, cider and FABs is the largest segment of the global alcoholic

Drinks Sector Guide Drinks Sector Guide The global alcoholic drinks market grew by 3.3% in 2014 to reach a value of $1,152,011.1 million. Beer, cider and FABs is the largest segment of the global alcoholic

Wine Australia Wine.com Data Report. July 21, 2017

Wine Australia Wine.com Data Report July 21, 2017 INTRODUCTION Wine Opinions is a wine market research company focusing on the attitudes, behaviors, and taste preferences of U.S. wine drinkers. Wine Opinions

Wine Australia Wine.com Data Report July 21, 2017 INTRODUCTION Wine Opinions is a wine market research company focusing on the attitudes, behaviors, and taste preferences of U.S. wine drinkers. Wine Opinions

Western Uganda s Arabica Opportunity. Kampala 20 th March, 2018

Western Uganda s Arabica Opportunity Kampala 20 th March, 2018 The western region has three main islands of Arabica production we focus on the Rwenzori region served by Kasese 3 Primary focus is the Rwenzori

Western Uganda s Arabica Opportunity Kampala 20 th March, 2018 The western region has three main islands of Arabica production we focus on the Rwenzori region served by Kasese 3 Primary focus is the Rwenzori

(A report prepared for Milk SA)

") South African Milk Processors Organisation The voluntary organisation of milk processors for the promotion of the development of the secondary dairy industry to the benefit of the dairy industry, the consumer

South African Milk Processors Organisation The voluntary organisation of milk processors for the promotion of the development of the secondary dairy industry to the benefit of the dairy industry, the consumer

Sector trend analysis. Cod fish in the United Kingdom. May MARKET ACCESS SECRETARIAT Global Analysis Report. Contents.

MARKET ACCESS SECRETARIAT Global Analysis Report Sector trend analysis Cod fish in the United Kingdom May 2017 Executive summary The United Kingdom (U.K.) is one of the most significant importers of cod

MARKET ACCESS SECRETARIAT Global Analysis Report Sector trend analysis Cod fish in the United Kingdom May 2017 Executive summary The United Kingdom (U.K.) is one of the most significant importers of cod

Retailer Survey Results

Retailer Survey Results Chex Finer Foods October, 2014 1 Grocery Mix Pretty much everything we sell is natural/specialty Hard to see the difference with a lot of our selections. Many could fall into either

Retailer Survey Results Chex Finer Foods October, 2014 1 Grocery Mix Pretty much everything we sell is natural/specialty Hard to see the difference with a lot of our selections. Many could fall into either

EMBARGO TO ON FRIDAY 16 SEPTEMBER. Scotch Whisky Association. Exports of Scotch Whisky; Year to end of June 2016 (2016 H1)

") EMBARGO TO 00.01 ON FRIDAY 16 SEPTEMBER Scotch Whisky Association Exports of Scotch Whisky; Year to end of June 2016 (2016 H1) VOLUME UP 3.1% to 531 MILLION bottles VALUE DOWN SLIGHTLY BY 1.0% TO 1.70

EMBARGO TO 00.01 ON FRIDAY 16 SEPTEMBER Scotch Whisky Association Exports of Scotch Whisky; Year to end of June 2016 (2016 H1) VOLUME UP 3.1% to 531 MILLION bottles VALUE DOWN SLIGHTLY BY 1.0% TO 1.70

CATEGORY CLOSE UP: FUELING THE FOUNTAIN

CATEGORY CLOSE UP: FUELING THE FOUNTAIN Operators fend off competition and keep up with trends to ensure their cold dispensed beverage sales continue to grow. By Jamie Hartford On paper, cold dispensed

CATEGORY CLOSE UP: FUELING THE FOUNTAIN Operators fend off competition and keep up with trends to ensure their cold dispensed beverage sales continue to grow. By Jamie Hartford On paper, cold dispensed

What do we know about fresh produce consumption

What do we know about fresh produce consumption PMA A & NZ - Fresh Forum Newcastle March 2011 Martin Kneebone Director Freshlogic Content Macro food market trends Food shopping consumer behaviour Household

What do we know about fresh produce consumption PMA A & NZ - Fresh Forum Newcastle March 2011 Martin Kneebone Director Freshlogic Content Macro food market trends Food shopping consumer behaviour Household

Pecans. The Consumer Speaks A consumer A&U study on Pecans 9/09/11

Pecans The Consumer Speaks A consumer A&U study on Pecans 9/09/11 2 Goal To increase Pecan sales.. 3 Objective Understand the consumer: Consumption frequency Usage occasions Attitudes / Behaviors / Beliefs

Pecans The Consumer Speaks A consumer A&U study on Pecans 9/09/11 2 Goal To increase Pecan sales.. 3 Objective Understand the consumer: Consumption frequency Usage occasions Attitudes / Behaviors / Beliefs

The Future of the Confectionery Market in South Africa to 2019

The Future of the Confectionery Market in South Africa to 2019 The Future of the Confectionery Market in South Africa to 2019 The Business Research Store is run by Sector Publishing Intelligence Ltd. SPi

The Future of the Confectionery Market in South Africa to 2019 The Future of the Confectionery Market in South Africa to 2019 The Business Research Store is run by Sector Publishing Intelligence Ltd. SPi

Financial results 2014/2015. Strategy and development perspectives

Financial results 2014/2015 Strategy and development perspectives Warsaw, September 2015 1 Agenda Strategy of the AMBRA Group Wine market in Poland Financial results and KPIs for 2014/2015 Development

Financial results 2014/2015 Strategy and development perspectives Warsaw, September 2015 1 Agenda Strategy of the AMBRA Group Wine market in Poland Financial results and KPIs for 2014/2015 Development

International Beverage. Frank van Oers

International Beverage Frank van Oers Long-term Growth Will Come from Single-Serve and Instants FY08 $3.2 Billion 6% 7% 8% 11% 18% 12% 38% 4% 24% 12% 3% 56% 1% 2 Multi-Serve (ex. Brazil) Single-Serve Instants

International Beverage Frank van Oers Long-term Growth Will Come from Single-Serve and Instants FY08 $3.2 Billion 6% 7% 8% 11% 18% 12% 38% 4% 24% 12% 3% 56% 1% 2 Multi-Serve (ex. Brazil) Single-Serve Instants

Candy/Snack Innovation Forum. February 21, 2006

Candy/Snack Innovation Forum February 21, 2006 Welcome To The Candy/Snack Forum Facilitators Debbie Wildrick Product Director- Packaged Goods 7-Eleven, Inc. Bill Dusek Managing Director Dechert-Hampe &

Candy/Snack Innovation Forum February 21, 2006 Welcome To The Candy/Snack Forum Facilitators Debbie Wildrick Product Director- Packaged Goods 7-Eleven, Inc. Bill Dusek Managing Director Dechert-Hampe &

Lukewarm sales for cold beverages

Lukewarm sales for cold beverages COLD BEVERAGES By Gillian Hurst Flat is one retailer s description of cold beverage sales in his store and he is not alone. With the exception of the most popular carbonated

Lukewarm sales for cold beverages COLD BEVERAGES By Gillian Hurst Flat is one retailer s description of cold beverage sales in his store and he is not alone. With the exception of the most popular carbonated

AMERICA S No.1 BARBECUE SAUCE. MAKE IT YOUR No.1

AMERICA S No.1 BARBECUE SAUCE MAKE IT YOUR No.1 WWW.SWEETBABYRAYS.CO.UK AMERICA S No.1 BARBECUE SAUCE NOW No.1 OVER here STRAIGHT OFF THE BOAT FROM THE USA, SWEET BABY RAY S IS THE NO1 BBQ SAUCE IN THE

AMERICA S No.1 BARBECUE SAUCE MAKE IT YOUR No.1 WWW.SWEETBABYRAYS.CO.UK AMERICA S No.1 BARBECUE SAUCE NOW No.1 OVER here STRAIGHT OFF THE BOAT FROM THE USA, SWEET BABY RAY S IS THE NO1 BBQ SAUCE IN THE

Foodservice EUROPE. 10 countries analyzed: AUSTRIA BELGIUM FRANCE GERMANY ITALY NETHERLANDS PORTUGAL SPAIN SWITZERLAND UK

Foodservice EUROPE MARKET INSIGHTS & CHALLENGES 2015 2016 2017 2020 Innovative European Foodservice Experts 18, avenue Marcel Anthonioz BP 28 01220 Divonne-les-Bains - France 10 countries analyzed: AUSTRIA

Foodservice EUROPE MARKET INSIGHTS & CHALLENGES 2015 2016 2017 2020 Innovative European Foodservice Experts 18, avenue Marcel Anthonioz BP 28 01220 Divonne-les-Bains - France 10 countries analyzed: AUSTRIA

2017 National Monitor of Fuel Consumer Attitudes ACAPMA

2017 National Monitor of Fuel Consumer Attitudes ACAPMA FIVE DIFFERENT FUEL SHOPPERS Convenience Store Shopper Location Driven Price Sensitive, Fuel Only Price Sensitive, Loyalty Fixed Retailer Percentage

2017 National Monitor of Fuel Consumer Attitudes ACAPMA FIVE DIFFERENT FUEL SHOPPERS Convenience Store Shopper Location Driven Price Sensitive, Fuel Only Price Sensitive, Loyalty Fixed Retailer Percentage

Shopping behaviours of different food and drinks consumption groups 35% 27% 16%

In Fact research facts from the HSC Shopping behaviours of different food and drinks consumption groups Background The cost of healthier foods is thought to be a barrier to healthy eating, but recent research

In Fact research facts from the HSC Shopping behaviours of different food and drinks consumption groups Background The cost of healthier foods is thought to be a barrier to healthy eating, but recent research

Feeser s Fall Meeting Soup Overview Soup Promotion. Campbell s Soup Company & Key Impact Sales October

Feeser s Fall Meeting Soup Overview Soup Promotion Campbell s Soup Company & Key Impact Sales October 10-2014 1 Introduction Soup, a traditional comfort food and quintessential healthy fare, is a significant

Feeser s Fall Meeting Soup Overview Soup Promotion Campbell s Soup Company & Key Impact Sales October 10-2014 1 Introduction Soup, a traditional comfort food and quintessential healthy fare, is a significant

RESEARCH UPDATE from Texas Wine Marketing Research Institute by Natalia Kolyesnikova, PhD Tim Dodd, PhD THANK YOU SPONSORS

RESEARCH UPDATE from by Natalia Kolyesnikova, PhD Tim Dodd, PhD THANK YOU SPONSORS STUDY 1 Identifying the Characteristics & Behavior of Consumer Segments in Texas Introduction Some wine industries depend

RESEARCH UPDATE from by Natalia Kolyesnikova, PhD Tim Dodd, PhD THANK YOU SPONSORS STUDY 1 Identifying the Characteristics & Behavior of Consumer Segments in Texas Introduction Some wine industries depend

Strategies for the future. Understanding on and off trade trends in order to drive growth in both

Strategies for the future Understanding on and off trade trends in order to drive growth in both EeBriaTrade is a craft beer marketplace connecting over 400 breweries with pubs nationwide 2 Craft Beer

Strategies for the future Understanding on and off trade trends in order to drive growth in both EeBriaTrade is a craft beer marketplace connecting over 400 breweries with pubs nationwide 2 Craft Beer

Wine On-Premise UK 2016

Wine On-Premise UK 2016 T H E M E N U Introduction... Page 5 The UK s Best On-Premise Distributors... Page 7 The UK s Most Listed Wine Brands... Page 17 The Big Picture... Page 26 The Style Mix... Page

Wine On-Premise UK 2016 T H E M E N U Introduction... Page 5 The UK s Best On-Premise Distributors... Page 7 The UK s Most Listed Wine Brands... Page 17 The Big Picture... Page 26 The Style Mix... Page

Update : Consumer Attitudes

Blah blah blah blah blah Consumers developed 40 words/attributes to describe commercially available EVOOs. Sensory differences were independent of country of origin. Update : Consumer Attitudes There was

Blah blah blah blah blah Consumers developed 40 words/attributes to describe commercially available EVOOs. Sensory differences were independent of country of origin. Update : Consumer Attitudes There was

Work Sample (Minimum) for 10-K Integration Assignment MAN and for suppliers of raw materials and services that the Company relies on.

for 10-K Integration Assignment MAN and for suppliers of raw materials and services that the Company relies on.") Work Sample (Minimum) for 10-K Integration Assignment MAN 4720 Employee Name: Your name goes here Company: Starbucks Date of Your Report: Date of 10-K: PESTEL 1. Political: Pg. 5 The Company supports the

Work Sample (Minimum) for 10-K Integration Assignment MAN 4720 Employee Name: Your name goes here Company: Starbucks Date of Your Report: Date of 10-K: PESTEL 1. Political: Pg. 5 The Company supports the

This is Haruhisa Inada. I will explain the financial results of the first quarter of FY 2018.

This is Haruhisa Inada. I will explain the financial results of the first quarter of FY 2018. 1 Compared to the previous year, revenue was 277.1 billion yen, up 3.3%, operating income was 26.6 billion

This is Haruhisa Inada. I will explain the financial results of the first quarter of FY 2018. 1 Compared to the previous year, revenue was 277.1 billion yen, up 3.3%, operating income was 26.6 billion

Eating Pattern Recession Part 3. Background. his report provides a unique look at inhome

Updates from Competitiveness and Market Analysis Branch Issue 13, April, 2011 Background T his report provides a unique look at inhome and away from home eating behaviour. What foods do Canadians eat at

Updates from Competitiveness and Market Analysis Branch Issue 13, April, 2011 Background T his report provides a unique look at inhome and away from home eating behaviour. What foods do Canadians eat at

COONAWARRA CABERNET SYMPOSIUM

COONAWARRA CABERNET SYMPOSIUM ANGIE BRADBURY Managing Director Consumer trends in local and international markets Drivers of consumer behaviour Challenges and opportunities for the noble grape What we

COONAWARRA CABERNET SYMPOSIUM ANGIE BRADBURY Managing Director Consumer trends in local and international markets Drivers of consumer behaviour Challenges and opportunities for the noble grape What we

CONTRACT CATERING FLAT AT BEST. The latest data kindly supplied by Peter Backman of Horizons For Success shows

CONTRACT CATERING FLAT AT BEST The latest data kindly supplied by Peter Backman of Horizons For Success shows that the contract catering sectors food and drink sales have barely moved over the last three

CONTRACT CATERING FLAT AT BEST The latest data kindly supplied by Peter Backman of Horizons For Success shows that the contract catering sectors food and drink sales have barely moved over the last three

The Grocer: Food-to-go Research on behalf of The Grocer October 2018

The Grocer: Food-to-go Research on behalf of The Grocer October 2018 Lucia Juliano Head of CPG & Retail Research +44 (0) 161 242 1371 ljuliano@harrisinteractive.co.uk 1 Almost two-thirds of people buy

The Grocer: Food-to-go Research on behalf of The Grocer October 2018 Lucia Juliano Head of CPG & Retail Research +44 (0) 161 242 1371 ljuliano@harrisinteractive.co.uk 1 Almost two-thirds of people buy

Attachment A. Core U.S. OJ & GJ Scanned Sales Data

Attachment A Channels Core U.S. OJ & GJ Scanned Sales Data Food ($2M+ Grocery) Drug Convenience Mass Walmart Specialty Channel Larger U.S. Universe (please describe) Market / Account Level Product Categories

Attachment A Channels Core U.S. OJ & GJ Scanned Sales Data Food ($2M+ Grocery) Drug Convenience Mass Walmart Specialty Channel Larger U.S. Universe (please describe) Market / Account Level Product Categories

Tet period: 4 weeks before the first day of Lunar New Year (4 w/e 2018/2/18)

") Tet period: 4 weeks before the first day of Lunar New Year (4 w/e 2018/2/18) In-home purchases during Tet 2018 is estimated to reach over 45 trillion VND for total Vietnam (nearly double value of normal

Tet period: 4 weeks before the first day of Lunar New Year (4 w/e 2018/2/18) In-home purchases during Tet 2018 is estimated to reach over 45 trillion VND for total Vietnam (nearly double value of normal

EZ Stop N Save Convenience Stores

EZ Stop N Save Convenience Stores Case Study Sponsored By: Page1 EZ Stop N Save Convenience Stores Case Logistics You will have 12 minutes to present to the coffee buying team of EZ Stop N Save. You should

EZ Stop N Save Convenience Stores Case Study Sponsored By: Page1 EZ Stop N Save Convenience Stores Case Logistics You will have 12 minutes to present to the coffee buying team of EZ Stop N Save. You should