October 22nd, By Jack Scoville

|

|

|

- Dwain Pierce

- 6 years ago

- Views:

Transcription

1 October 22nd, 2017 By Jack Scoville Wheat: US markets were lower last week in all three markets. The trade remains concerned about demand even though the weekly export sales report was strong last week. Export demand appears to be in line with USDA projections for the year. Traders do not appear all that concerned with the slower than normal planting progress for crops in the Great Plains and Midwest as there is plenty of Wheat available around the world. The US looks to plant less acres to Wheat again this year, meaning that the US will have less area planted to Wheat than seen over the last 100 or more years once again this year. The weekly charts show that futures moved close to some support areas again last week. Australia has started to see some rains that have started to break the extreme drought seen in Wheat country. However, it is close to harvest time now, so the rains might not be all that beneficial as big rains now could damage the quality of what will be a very small; crop. Even so, Australian prices have moved lower and Australian Wheat is providing more competition for sales in the Far East for the US now. US Wheat remains very competitive in world markets due to reduced production from about all origins except for Russia. Russia has been selling aggressively and has set the world price, but US prices are just as cheap right now. This is due to the weaker futures along with the weaker US Dollar. Wheat prices are cheap enough now and need not go lower. A big rally will probably be difficult without better and sustained demand. Weekly Chicago Soft Red Winter Wheat Futures Weekly Chicago Hard Red Winter Wheat Futures

2 Weekly Minneapolis Hard Red Spring Wheat Futures

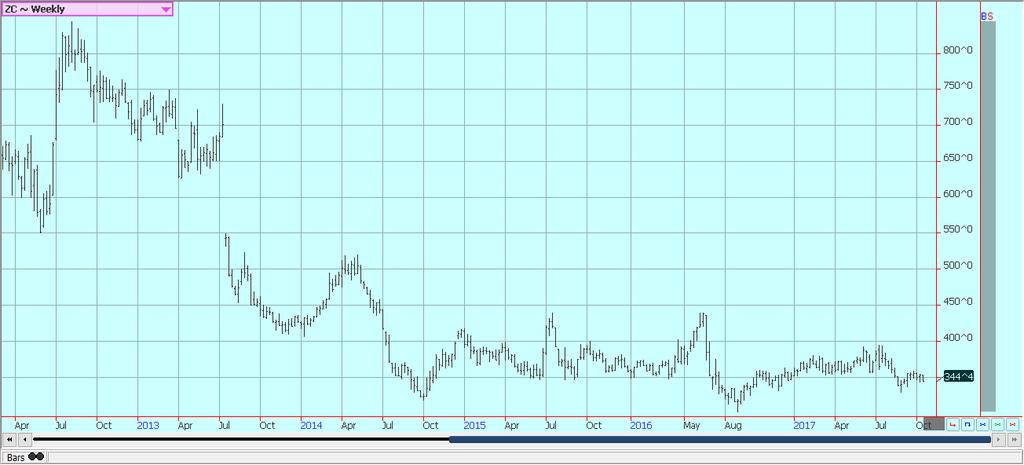

3 Corn: Corn closed lower and Oats closed a little higher for the week as the US Corn harvest expands in much of the Midwest. The export sales report on Thursday was very strong for Corn and was a reason to buy the market, but traders seem much more interested in the harvest and the potential for increasing supplies. Basis levels remain very weak but are starting to improve again as transportation logistics become easier. The Mississippi and Illinois rivers have been low due to lack of rainfall and barge transportation has been difficult and very expensive. There has been some significant rain in the Midwest over the last couple of weeks, with more seen over the weekend, and river levels should be improving. A lock on the Ohio River was closed for emergency repairs and that caused transportation problems on that river system, but has now been repaired. Basis levels throughout the Midwest have reacted to the improved situation, although they remain generally weak as it is still harvest time. The market is hearing more harvest results as activity moves north into central parts of the Corn Belt and also gets active in the east. Yields have been generally strong, but the harvest pace has been a little slow as producers have been concentrating more on getting the Soybeans harvested and letting the Corn dry in the fields. Many producers in central and eastern areas are now about done with the Soybeans harvest and will now concentrate on Corn. Weekly Corn Futures:

4

5 Weekly Oats Futures Soybeans and Soybean Meal: Soybeans and Soybean Meal were lower on Friday in reaction to ideas of strong harvest progress and big crops being harvested. Soybean Meal also suffers from weak demand due to strong competition from DDGS in the market and on ideas that crush levels can remain strong due to the need to produce Soybean Oil on reduced Argentine imports. The US government moved to impose punitive duties on Argentine Soybean Oil imports into the US recently, then has tried to move mandate levels to reflect the reduced feedstock supply. The latter move has failed as the government said Friday that mandate levels will be maintained or expanded and not cut back in any way. Harvest weather should be good this week in the Midwest after weekend rains as forecasts call for cool and dry conditions. There are still forecasts around for weather patterns to change in Brazil and bring some badly needed rain to the north and drier conditions to the south and into Argentina. The US harvest has been more active in areas east of the Mississippi River and is starting to finish in these areas, while areas to the west of the river are expanding. The yield data generally runs behind year ago levels, but are still very strong overall. Basis levels have started to improve as the river levels move higher due to recent rains, although basis levels have been weak at the Gulf of Mexico. It remains too dry for best planting in the northern half of Brazil, while the southern half of Brazil and the northern half of Argentina get too much rain. It is planting time for Soybeans there, but progress is very slow right now. Ideas are that the weather patterns there can start to change and more favorable planting weather will be seen near the end of the month.

6

7 Weekly Chicago Soybeans Futures: Weekly Chicago Soybean Meal Futures

8 Rice: Rice closed higher on Friday, but lower for the week. The daily charts still show futures prices locked in a short term trading range. The sales report last week was strong, and were especially strong for long grain into Latin America. That demand news has been great for the market. Latin American buyers in recent years have complained about the quality of the US crop and have bought more and more from Brazil or elsewhere in Latin America. The strong sales now show that the US quality is very good this year and also that the US is featuring competitive prices into these regions. Domestic cash market conditions are generally quiet. The Delta harvest is about over and as farmers are holding out for higher prices. California has significant harvest progress to make now. Reports from the country indicate good to very good yields and quality for the Delta as the harvest comes to a close in most areas. Yields in California right now are lower than hoped for as the late start to planting appears to have created a short season and less yield potential. Domestic cash quotes have held generally steady amid little interest in the Delta and are called firm in California. Weekly Chicago Rice Futures

9 Palm Oil and Vegetable Oils: Palm Oil futures moved a little higher last week, and weekly charts show that the market remains in a trading range. The market moved higher as data released by the private sources showed that exports for the first half of the month was very strong. Both showed that exports this month are at least 10% higher than last month. China is back and buying now and demand could get stronger. Canola was higher on a weaker Canadian Dollar and despite increased farm selling and active harvest activity. Farmers have started to more actively sell and deliver as the harvest starts to move into its final stages. Yield reports yet imply a good but not great crop in just about all areas of the Prairies. Soybean Oil was also higher. The US government moved to impose punitive duties on Argentine Soybean Oil imports into the US recently, then has tried to move mandate levels to reflect the reduced feedstock supply. The latter move has failed as the government said Friday that mandate levels will be maintained or expanded and not cut back in any way. Ideas are that US domestic Soybean Oil demand can stay strong. Weekly Malaysian Palm Oil Futures:

10 Weekly Chicago Soybean Oil Futures Weekly Canola Futures:

11 Cotton: Cotton was lower last week as a big crop of good quality is being harvested. Even improved export sales could not support the market last week as the amount sold was not exceptional for this time of year at under 400,000 bales. The classing report released on Friday shows that quality is holding after the hurricanes seen in Texas and the Southeast this Summer. The harvest still has a long way to go, but the quality is good and there is a lot of Cotton that will have to come to the market sooner or later. Futures appear to be turning trends down again, and tests of 6500 December and perhaps near 6000 December are possible now. Harvest is more active and will continue to expand as more and more of the crop comes to maturity, Bolls are opening now in just about all production areas, but harvest remains a little behind normal. West Texas conditions are called good and the Southwest should be good despite hot weather this year. There is strong production potential in Asia, and mostly in India and Pakistan due to improved monsoon rains. However, the rains were variable, with some areas getting flooding rains and others not enough rain. Some rains are expected in most areas this week amid relatively moderate temperatures. Chinese growing conditions are good. Areas in southern Russia and surrounding nations are in good condition. Weekly US Cotton Futures Frozen Concentrated Orange Juice and Citrus: FCOJ closed higher and appear to be developing a trading range. The market has not been able to fill a gap left in reaction to Irma and the losses seen in Florida as a result of the devastating storm. Futures are still reacting to t the USDA reports that showed big production loss potential from the hurricane, but not the losses expected by the trade. USDA is expected bt many to show further dramatic cuts in production in coming reports. Ideas remain that the Orange groves are badly damaged in Florida due to Irma. Crops in many areas were almost completely destroyed. Other areas suffered losses of 50% or more of the crop. Some growers say that trees will be stressed again next year due to the winds and rains from Irma. The demand side remains weak and there are plenty of supplies in the US. Trees that are still alive now are

12 showing fruit of good sizes, although many have lost a lot of the fruit. Brazil crops are stressed from hot and dry weather. Weekly FCOJ Futures Coffee: Futures were lower in New York and in London last week, with commercials scale down buyers and speculators still the best sellers, but now on both sides of the market. The trends are down on the charts in New York as traders look at the potential for a big crop in Brazil. London trends are sideways. The Brazil weather and tree condition is the main fundamental reason for lower New York prices, but could become the major reason to buy the market soon. Rains appeared in Brazil a couple of weeks ago, then it turned dry again. These rains promoted flowering, and some reports indicate that flowering has been very good. Other areas have seen good flowering, but might not see much fruit as the trees have defoliated due to earlier stress. The current dry period is causing some to wonder if the flowers will start to abort. There are some forecasts for rains early this week, but amounts and coverage forecasts have faded as the even draws closer. The rains will need to continue and be in good amounts as it has been very dry and trees have been stressed for a year or more in some cases. Some were stressed after the production last year, while others suffered due to the dry and cold Winter. Even so, improved weather now could mean a very good crop, although most likely not a huge crop of over 50 million bags. Cash market conditions in Central America are more active as the next harvest continues. There is coffee to sell and offers are on the table for the next crop. Differentials have been stable but weak in the region. Colombia has reported some difficult growing conditions, but exports have held well as production appears to be good. Differentials have been stable and relatively strong.

13 Weekly New York Arabica Coffee Futures Weekly London Robusta Coffee Futures

14 Sugar: Futures were a little lower in New York and in London, and price trends remain sideways in both markets. Both markets held support areas on the weekly charts, but remain locked in sideways trends as ideas of big production go against hopes for improved demand. Brazil has been hot and dry, but some rains are in the forecast for early this week. No one is talking about production losses yet, but many are watching the situation. The market expects firmer prices over time as the Indian harvest could be delayed due to wet conditions that would delay Sugarcane harvesting. There are questions about the Indian production this year as the distribution on monsoon rains was not uniform. Some areas saw flooding rains while others got well below normal totals. The monsoon is starting to recede now. Overall upside potential is limited as there are still projections for a surplus in the world production, and these projections for the surplus seem to be getting bigger over time. Production potential in Thailand seems strong as monsoon rains have been better than last year. However, buying from the Far East has often gone to India lately as Thai differentials have been high.

15 Weekly New York World Raw Sugar Futures Weekly London White Sugar Futures

16 Cocoa: Futures closed a Little lower on Friday, but higher for the week in response to positive demand news from as the North American grind data last week and the European grind data the previous week. The North American data did show an increase in demand, but not as much as some traders had hoped for. The trends are now up in New York and in London on both the daily and weekly charts, although the weekly charts show that some important resistance is just ahead at about 2180 New York December. Traders saw positive grind data from Asia on Friday. World production ideas remain high. Harvest reports show good to very good production will be seen this year in West Africa. Ghana and Ivory Coast expects a very good crop this year. Nigeria and Cameroon are reporting good yields on the initial harvest, and also good quality. The growing conditions in other parts of the world are generally good. East Africa is getting better rains now. Good conditions are still seen in Southeast Asia. Traders talk of increased demand to go against big world production as prices are now attractive for grinders and chocolate manufacturers. Weekly New York Cocoa Futures

17 Weekly London Cocoa Futures Dairy and Meat: Dairy markets were sharply lower again last week and Milk futures made new lows for the move. The Global Dairy Auction was weaker last week. USDA reports ample supplies, but good to very good demand in just about all parts of the US. Milk and Cheese demand has been mixed, but Butter demand has weakened and prices in this market have moved sharply lower. Demand is good for cream, but cream has generally been available to meet the demand. Cream demand for Butter has been very good. Demand for Ice Cream has been mixed depending on the region, but is holding well due to mild weather in much of the US. Cheese demand still appears to be weaker and inventories appear high. US production conditions have featured some abnormally hot weather in the west that is hurting milk production. Production in the rest of the country has been strong. US cattle and beef prices were lower, but futures held up trends. Beef prices remain firm, and Cattle traded about #2.00 per hundredweight higher last week. Ideas are that packers are still enjoying very strong margins at this time and can afford to pay more for Cattle. This did happen last week. The beef market was somewhat better last week to support ideas that prices for Cattle could continue to improve. Cattle prices were steady to slightly weaker in early dealings and amid lighter than expected volume. It is the threat of increased supplies down the road that keeps the packers from buying aggressively. Feedlots are full, but ideas are that the big offer of Cattle has passed. The monthly Cattle on Feed report on Friday showed big placements, so prices should move lower this week in both Live Cattle and Feeder Cattle futures.

18 Pork markets and Lean Hogs futures were higher. Ideas are that futures are reflecting the weaker supply and demand fundamentals now, but the overall market seems to be improving. Demand has been improved for the last couple of weeks and this has affected pricing. There are still ideas of bug supplies out there, but the market seems to have the supply side priced. The weekly charts show that the market is trying to form a low at current prices, and futures have been cheap enough that a low is possible at this time. The weekly charts suggest that futures are completing an important bottom in prices at this time. Weekly Chicago Class 3 Milk Futures

19 Weekly Chicago Cheese Futures Weekly Chicago Butter Futures

20 Weekly Chicago Live Cattle Futures: Weekly Feeder Cattle Futures: Weekly Chicago Lean Hog Futures:

21 Futures and options trading involves substantial risk of loss and may not be suitable for everyone. The valuation of futures and options may fluctuate and as a result, clients may lose more than their original investment. In no event should the content of this website be construed as an express or implied promise, guarantee, or implication by or from The PRICE Futures Group, Inc. that you will profit or that losses can or will be limited whatsoever. Past performance is not indicative of future results. Information provided on this report is intended solely for informative purpose and is obtained from sources believed to be reliable. No guarantee of any kind is implied or possible where projections of future conditions are attempted. The leverage created by trading on margin can work against you as well as for you, and losses can exceed your entire investment. Before opening an account and trading, you should seek advice from your advisors as appropriate to ensure that you understand the risks and can withstand the losses.

October 8th, By Jack Scoville

October 8th, 2018 By Jack Scoville Wheat: Wheat was higher last week as world prices held firm. Firm prices extend from Russia to Australia on reduced world production. It remains very dry in Australia,

October 8th, 2018 By Jack Scoville Wheat: Wheat was higher last week as world prices held firm. Firm prices extend from Russia to Australia on reduced world production. It remains very dry in Australia,

April 16th, By Jack Scoville

April 16th, 2018 By Jack Scoville Wheat: Wheat markets were near unchanged in Chicago as weather and demand remained the dominant factors in the market. Kansas City was lower for the week, while Minneapolis

April 16th, 2018 By Jack Scoville Wheat: Wheat markets were near unchanged in Chicago as weather and demand remained the dominant factors in the market. Kansas City was lower for the week, while Minneapolis

March 25th, By Jack Scoville

March 25th, 2019 By Jack Scoville Wheat: Winter Wheat markets were higher and Minneapolis Spring Wheat prices closed slightly higher for the week. Chicago SRW prices are now above important resistance

March 25th, 2019 By Jack Scoville Wheat: Winter Wheat markets were higher and Minneapolis Spring Wheat prices closed slightly higher for the week. Chicago SRW prices are now above important resistance

August 13th, By Jack Scoville

August 13th, 2018 By Jack Scoville Wheat: Wheat closed lower last week, with most of the selling coming on Friday in response to the USDA production and supply and demand reports. The US data was somewhat

August 13th, 2018 By Jack Scoville Wheat: Wheat closed lower last week, with most of the selling coming on Friday in response to the USDA production and supply and demand reports. The US data was somewhat

September 3rd, By Jack Scoville

September 3rd, 2017 By Jack Scoville Wheat: US markets were mixed, with Chicago markets moving higher and Minneapolis markets moving lower. Minneapolis moved lower on bigger than expected production projections

September 3rd, 2017 By Jack Scoville Wheat: US markets were mixed, with Chicago markets moving higher and Minneapolis markets moving lower. Minneapolis moved lower on bigger than expected production projections

January 15th, By Jack Scoville

January 15th, 2017 By Jack Scoville Wheat: US markets closed lower on Friday and lower for the week in response to the USDA planted area estimates. USDA showed higher than expected planted area for all

January 15th, 2017 By Jack Scoville Wheat: US markets closed lower on Friday and lower for the week in response to the USDA planted area estimates. USDA showed higher than expected planted area for all

February 11th, By Jack Scoville

February 11th, 2019 By Jack Scoville Wheat: Winter Wheat markets were lower for the week last week. Chicago SRW prices held firm on Friday in response to news that Egypt had bought 120,000 tons of SRW.

February 11th, 2019 By Jack Scoville Wheat: Winter Wheat markets were lower for the week last week. Chicago SRW prices held firm on Friday in response to news that Egypt had bought 120,000 tons of SRW.

April 9th, By Jack Scoville

April 9th, 2018 By Jack Scoville Wheat: Wheat markets were higher as weather returned as a dominant factor in the market. Forecasts still call for dry weather in Texas and Oklahoma and it is dry again

April 9th, 2018 By Jack Scoville Wheat: Wheat markets were higher as weather returned as a dominant factor in the market. Forecasts still call for dry weather in Texas and Oklahoma and it is dry again

December 17th, By Jack Scoville

December 17th, 2017 By Jack Scoville Wheat: US markets closed slightly lower again in Chicago last week as demand from the export market remains a big problem. Futures also closed lower in Minneapolis,

December 17th, 2017 By Jack Scoville Wheat: US markets closed slightly lower again in Chicago last week as demand from the export market remains a big problem. Futures also closed lower in Minneapolis,

September 10th, By Jack Scoville

September 10th, 2018 By Jack Scoville Wheat: Wheat markets were lower last week on reports of softer prices in Europe and Russia. The market keeps it focus primarily on Russia and the prices it sells Wheat

September 10th, 2018 By Jack Scoville Wheat: Wheat markets were lower last week on reports of softer prices in Europe and Russia. The market keeps it focus primarily on Russia and the prices it sells Wheat

May 14th, By Jack Scoville

May 14th, 2018 By Jack Scoville Wheat: Wheat markets were lower, with much of the selling in reaction to the USDA reports released on Thursday. The reports showed increased production estimates from a

May 14th, 2018 By Jack Scoville Wheat: Wheat markets were lower, with much of the selling in reaction to the USDA reports released on Thursday. The reports showed increased production estimates from a

April 30th, By Jack Scoville

April 30th, 2018 By Jack Scoville Wheat: Wheat markets were higher as weather and demand remained the dominant factors in the market. It remains very dry in western parts of the Great Plains, and crop

April 30th, 2018 By Jack Scoville Wheat: Wheat markets were higher as weather and demand remained the dominant factors in the market. It remains very dry in western parts of the Great Plains, and crop

May 21st, By Jack Scoville

May 21st, 2018 By Jack Scoville Wheat: Wheat markets were higher on uncertain production prospects at home and increasingly in other producing countries. The dry conditions in the western Great Plains,

May 21st, 2018 By Jack Scoville Wheat: Wheat markets were higher on uncertain production prospects at home and increasingly in other producing countries. The dry conditions in the western Great Plains,

February 25th, By Jack Scoville

February 25th, 2019 By Jack Scoville Wheat: Winter Wheat markets were mostly a little higher on Friday, but lower for the week. World Wheat prices were softer as well. USDA released its export sales report

February 25th, 2019 By Jack Scoville Wheat: Winter Wheat markets were mostly a little higher on Friday, but lower for the week. World Wheat prices were softer as well. USDA released its export sales report

January 8 th, By Jack Scoville

January 8 th, 2017 By Jack Scoville Wheat: US markets were higher for the week. The weekly charts show that trends are turning up in Chicago SRW and have already turned up in Chicago HRW and Minneapolis.

January 8 th, 2017 By Jack Scoville Wheat: US markets were higher for the week. The weekly charts show that trends are turning up in Chicago SRW and have already turned up in Chicago HRW and Minneapolis.

February 12 th, By Jack Scoville

February 12 th, 2017 By Jack Scoville Wheat: US markets were higher last week. Prices surged after the monthly USDS supply and demand updates were released. USDA increased US export demand by 50 million

February 12 th, 2017 By Jack Scoville Wheat: US markets were higher last week. Prices surged after the monthly USDS supply and demand updates were released. USDA increased US export demand by 50 million

March 19 th, By Jack Scoville

March 19 th, 2017 By Jack Scoville Wheat: US markets were higher and closed the week on a strong note. Chicago SRW futures could complete a test of the lows and indicate a new up trend is underway if some

March 19 th, 2017 By Jack Scoville Wheat: US markets were higher and closed the week on a strong note. Chicago SRW futures could complete a test of the lows and indicate a new up trend is underway if some

Monthly Economic Letter

Monthly Economic Letter Cotton Market Fundamentals & Price Outlook RECENT PRICE MOVEMENT After falling in the days surrounding the release of last month s USDA report, NY futures and the A Index were mostly

Monthly Economic Letter Cotton Market Fundamentals & Price Outlook RECENT PRICE MOVEMENT After falling in the days surrounding the release of last month s USDA report, NY futures and the A Index were mostly

Soft Commodity Markets - Upcoming Milestones, and How the Market Could Be Affected

Soft Commodity Markets - Upcoming Milestones, and How the Market Could Be Affected September 15, 2014 Judith Ganes President J. Ganes Consulting, LLC Weather & Politics Current Weather Expectations El

Soft Commodity Markets - Upcoming Milestones, and How the Market Could Be Affected September 15, 2014 Judith Ganes President J. Ganes Consulting, LLC Weather & Politics Current Weather Expectations El

Cocoa Prepared by Foresight October 3, 2018

Cocoa Prepared by Foresight October 3, 2018 TABLES Cocoa Bean Price Forecast... P. 4 World Cocoa Supply/Demand, Crop Year... P. 7 World Cocoa Production... P. 8 Cocoa Crops in Major Producing Countries...

Cocoa Prepared by Foresight October 3, 2018 TABLES Cocoa Bean Price Forecast... P. 4 World Cocoa Supply/Demand, Crop Year... P. 7 World Cocoa Production... P. 8 Cocoa Crops in Major Producing Countries...

Basis could avoid last fall s disaster Smaller corn crop should free up space for soybeans By Bryce Knorr

Basis could avoid last fall s disaster Smaller corn crop should free up space for soybeans By Bryce Knorr While the futures market has offered only occasional hope this summer, the picture in the cash

Basis could avoid last fall s disaster Smaller corn crop should free up space for soybeans By Bryce Knorr While the futures market has offered only occasional hope this summer, the picture in the cash

Cocoa Prepared by Foresight December 5, 2017

Cocoa Prepared by Foresight December 5, 2017 TABLES Cocoa Bean Price Forecast... P. 4 World Cocoa Supply/Demand, Crop Year... P. 7 World Cocoa Production... P. 8 Cocoa Crops in Major Producing Countries...

Cocoa Prepared by Foresight December 5, 2017 TABLES Cocoa Bean Price Forecast... P. 4 World Cocoa Supply/Demand, Crop Year... P. 7 World Cocoa Production... P. 8 Cocoa Crops in Major Producing Countries...

Acreage Forecast

World (John Sandbakken and Larry Kleingartner) The sunflower is native to North America but commercialization of the plant took place in Russia. Sunflower oil is the preferred oil in most of Europe, Mexico

World (John Sandbakken and Larry Kleingartner) The sunflower is native to North America but commercialization of the plant took place in Russia. Sunflower oil is the preferred oil in most of Europe, Mexico

Commitment of. Traders. Managed Money. Fund Positions

October 5, 2018 Market Summary The USDA will issue its October Supply and Demand report this next Thursday and will incorporate updated ending stocks data from last weeks report. Additionally, they will

October 5, 2018 Market Summary The USDA will issue its October Supply and Demand report this next Thursday and will incorporate updated ending stocks data from last weeks report. Additionally, they will

World coffee consumption increases but prices still low

World coffee consumption increases but prices still low The coffee market stabilised slightly in February, but prices remain at very low levels. A lack of news regarding fundamentals with expectations

World coffee consumption increases but prices still low The coffee market stabilised slightly in February, but prices remain at very low levels. A lack of news regarding fundamentals with expectations

Record exports from Brazil weigh heavy on the coffee market

Record exports from Brazil weigh heavy on the coffee market Coffee exports from Brazil reached a record high of 36.8 million bags in crop year 2014/15 (April to March), fuelled by domestic stocks and encouraged

Record exports from Brazil weigh heavy on the coffee market Coffee exports from Brazil reached a record high of 36.8 million bags in crop year 2014/15 (April to March), fuelled by domestic stocks and encouraged

Coffee market ends 2016/17 coffee year in deficit for the third consecutive year

Coffee market ends 2016/17 coffee year in deficit for the third consecutive year The ICO composite indicator continued its downward trend that started at the end of August, averaging 124.46 US cents/lb.

Coffee market ends 2016/17 coffee year in deficit for the third consecutive year The ICO composite indicator continued its downward trend that started at the end of August, averaging 124.46 US cents/lb.

Monthly Economic Letter

Monthly Economic Letter Cotton Market Fundamentals & Price Outlook RECENT PRICE MOVEMENT After some upward movement in April, most benchmark prices turned lower in early May. After climbing to the upper

Monthly Economic Letter Cotton Market Fundamentals & Price Outlook RECENT PRICE MOVEMENT After some upward movement in April, most benchmark prices turned lower in early May. After climbing to the upper

2018/19 expected to be the second year of surplus

2018/19 expected to be the second year of surplus Coffee year 2018/19 is expected to be the second consecutive season of surplus, as global output, estimated at 167.47 million bags, exceeds world consumption,

2018/19 expected to be the second year of surplus Coffee year 2018/19 is expected to be the second consecutive season of surplus, as global output, estimated at 167.47 million bags, exceeds world consumption,

Volatility returns to the coffee market as prices stay low

Volatility returns to the coffee market as prices stay low Daily coffee prices hit their lowest level in 19 months during August, as commodity markets worldwide were negatively affected by currency movements

Volatility returns to the coffee market as prices stay low Daily coffee prices hit their lowest level in 19 months during August, as commodity markets worldwide were negatively affected by currency movements

MONTHLY COFFEE MARKET REPORT

E MONTHLY COFFEE MARKET REPORT May 2014 After five consecutive months of rising prices, the coffee market reversed lower in May. From a high of 179 cents/lb in April, the daily price of the ICO composite

E MONTHLY COFFEE MARKET REPORT May 2014 After five consecutive months of rising prices, the coffee market reversed lower in May. From a high of 179 cents/lb in April, the daily price of the ICO composite

Prices for all coffee groups increased in May

Prices for all coffee groups increased in May In May 2018, the ICO composite indicator increased by 0.7% to an average of 113.34 US cents/lb, following three months of declines. Prices for all coffee groups

Prices for all coffee groups increased in May In May 2018, the ICO composite indicator increased by 0.7% to an average of 113.34 US cents/lb, following three months of declines. Prices for all coffee groups

2016 China Dry Bean Historical production And Estimated planting intentions Analysis

2016 China Dry Bean Historical production And Estimated planting intentions Analysis Performed by Fairman International Business Consulting 1 of 10 P a g e I. EXECUTIVE SUMMARY A. Overall Bean Planting

2016 China Dry Bean Historical production And Estimated planting intentions Analysis Performed by Fairman International Business Consulting 1 of 10 P a g e I. EXECUTIVE SUMMARY A. Overall Bean Planting

Coffee market ends 2015/16 in deficit for the second consecutive year

Coffee market ends 2015/16 in deficit for the second consecutive year The coffee market settled up by 5.5% in September, mostly driven by a steady increase in Robusta prices supported by concerns over

Coffee market ends 2015/16 in deficit for the second consecutive year The coffee market settled up by 5.5% in September, mostly driven by a steady increase in Robusta prices supported by concerns over

Monthly Economic Letter

Monthly Economic Letter Cotton Market Fundamentals & Price Outlook RECENT PRICE MOVEMENT NY futures experienced volatility recently, with the net effect being a slight increase in prices. The A Index also

Monthly Economic Letter Cotton Market Fundamentals & Price Outlook RECENT PRICE MOVEMENT NY futures experienced volatility recently, with the net effect being a slight increase in prices. The A Index also

MONTHLY COFFEE MARKET REPORT

1 E MONTHLY COFFEE MARKET REPORT March 2014 Ongoing uncertainty over the Brazilian coffee crop has caused significant fluctuations in coffee prices during March, with monthly volatility of the International

1 E MONTHLY COFFEE MARKET REPORT March 2014 Ongoing uncertainty over the Brazilian coffee crop has caused significant fluctuations in coffee prices during March, with monthly volatility of the International

Fresh Deciduous Fruit (Apples, Grapes, & Pears): World Markets and Trade

: World Markets and Trade") Million MT United States Department of Agriculture Foreign Agricultural Service December 21 Fresh Deciduous Fruit (Apples, Grapes, & Pears): World Markets and Trade 21/11 Forecast: World Apple Trade Declines;

Million MT United States Department of Agriculture Foreign Agricultural Service December 21 Fresh Deciduous Fruit (Apples, Grapes, & Pears): World Markets and Trade 21/11 Forecast: World Apple Trade Declines;

Monthly Economic Letter

Monthly Economic Letter Cotton Market Fundamentals & Price Outlook RECENT PRICE MOVEMENT NY futures and the A Index decreased throughout December before stabilizing in January. Chinese and Pakistani prices

Monthly Economic Letter Cotton Market Fundamentals & Price Outlook RECENT PRICE MOVEMENT NY futures and the A Index decreased throughout December before stabilizing in January. Chinese and Pakistani prices

MONTHLY COFFEE MARKET REPORT

E MONTHLY COFFEE MARKET REPORT June 2013 Coffee prices fell sharply in June 2013, as market fundamentals, combined with an uncertain macroeconomic outlook, drove the ICO composite indicator price to its

E MONTHLY COFFEE MARKET REPORT June 2013 Coffee prices fell sharply in June 2013, as market fundamentals, combined with an uncertain macroeconomic outlook, drove the ICO composite indicator price to its

SPRING WHEAT FUTURES AND OPTIONS

SPRING WHEAT FUTURES AND OPTIONS W hether it s a farmer near Minot, a trader in Minneapolis or a there is only one place to look when it comes to hard red spring WORLD S LARGEST SPRING WHEAT MARKET Since

SPRING WHEAT FUTURES AND OPTIONS W hether it s a farmer near Minot, a trader in Minneapolis or a there is only one place to look when it comes to hard red spring WORLD S LARGEST SPRING WHEAT MARKET Since

WEEKLY MAIZE REPORT 06 FEBRUARY 2019

WEEKLY MAIZE REPORT 06 FEBRUARY 2019 Unigrain (Pty) Ltd Tel. No. : +27 11 692 4400 Fax. No. : +27 11 412 1183 INTERNATIONAL MARKET Table 1: CME Maize prices and weekly changes (cents/bushel) Currently

WEEKLY MAIZE REPORT 06 FEBRUARY 2019 Unigrain (Pty) Ltd Tel. No. : +27 11 692 4400 Fax. No. : +27 11 412 1183 INTERNATIONAL MARKET Table 1: CME Maize prices and weekly changes (cents/bushel) Currently

Dairy Market R E P O R T

Volume 18 No. 8 Dairy Market R E P O R T August 2015 DMI NMPF Overview Milk prices in many major milk-producing countries have plummeted to levels that are producing severe financial stress for their farmers.

Volume 18 No. 8 Dairy Market R E P O R T August 2015 DMI NMPF Overview Milk prices in many major milk-producing countries have plummeted to levels that are producing severe financial stress for their farmers.

Record Exports for Coffee Year 2016/17

Record Exports for Coffee Year 2016/17 Total exports in September 2017 reached 8.34 million bags, compared to 9.8 million in September 2016. While coffee year 2016/17 registered a decrease in its final

Record Exports for Coffee Year 2016/17 Total exports in September 2017 reached 8.34 million bags, compared to 9.8 million in September 2016. While coffee year 2016/17 registered a decrease in its final

Minutes for the Freshfel/SHAFFE Citrus Teleconference of 25 September 2009

25th September 2009 Minutes for the Freshfel/SHAFFE Citrus Teleconference of 25 September 2009 Introduction: A declaration was made by all participants that the discussion will by no means involve matters

25th September 2009 Minutes for the Freshfel/SHAFFE Citrus Teleconference of 25 September 2009 Introduction: A declaration was made by all participants that the discussion will by no means involve matters

International Market Trends on Cocoa Trade for Sustainable Development Programme

International Market Trends on Cocoa Trade for Sustainable Development Programme Global Cocoa Trends: Production Primary cocoa growing regions are Africa, Asia and Latin America. Africa accounts for 70%

International Market Trends on Cocoa Trade for Sustainable Development Programme Global Cocoa Trends: Production Primary cocoa growing regions are Africa, Asia and Latin America. Africa accounts for 70%

Coffee market settles lower amidst strong global exports

Coffee market settles lower amidst strong global exports The ICO composite indicator price declined by 1.2% in February 2018 to an average of 114.19 US cents/lb. Indicator prices for all three Arabica

Coffee market settles lower amidst strong global exports The ICO composite indicator price declined by 1.2% in February 2018 to an average of 114.19 US cents/lb. Indicator prices for all three Arabica

Coffee market ends 2014 at ten month low

Coffee market ends 2014 at ten month low Coffee prices continued to slide downwards in December 2014, with the monthly average of the ICO composite indicator at its lowest level since February. Recent

Coffee market ends 2014 at ten month low Coffee prices continued to slide downwards in December 2014, with the monthly average of the ICO composite indicator at its lowest level since February. Recent

Ecobank s pan-african footprint. Africa-Asia trade flows

Ecobank s pan-african footprint Africa-Asia trade flows Ghana, Côte d Ivoire and Nigeria: The changing face of West African cocoa Dr Edward George Head of Group Research, Ecobank Lagos, February 3rd 2016

Ecobank s pan-african footprint Africa-Asia trade flows Ghana, Côte d Ivoire and Nigeria: The changing face of West African cocoa Dr Edward George Head of Group Research, Ecobank Lagos, February 3rd 2016

MONTHLY COFFEE MARKET REPORT

E MONTHLY COFFEE MARKET REPORT February 2014 February 2014 has seen significant developments in the coffee market, with prices shooting upwards at a startling rate. The ICO composite daily price has increased

E MONTHLY COFFEE MARKET REPORT February 2014 February 2014 has seen significant developments in the coffee market, with prices shooting upwards at a startling rate. The ICO composite daily price has increased

Monthly Economic Letter U.S. and Global Market Fundamentals

Monthly Economic Letter U.S. and Global Market Fundamentals August 2012 www.cottoninc.com After trading within relatively narrow bands throughout July, New York futures moved higher in early August, with

Monthly Economic Letter U.S. and Global Market Fundamentals August 2012 www.cottoninc.com After trading within relatively narrow bands throughout July, New York futures moved higher in early August, with

and the World Market for Wine The Central Valley is a Central Part of the Competitive World of Wine What is happening in the world of wine?

The Central Valley Winegrape Industry and the World Market for Wine Daniel A. Sumner University it of California i Agricultural l Issues Center January 5, 211 The Central Valley is a Central Part of the

The Central Valley Winegrape Industry and the World Market for Wine Daniel A. Sumner University it of California i Agricultural l Issues Center January 5, 211 The Central Valley is a Central Part of the

WEEKLY MAIZE REPORT 11 JULY 2018

28 29 21 211 212 213 214 215 216 217 218 WEEKLY MAIZE REPORT 11 JULY 218 Unigrain (Pty) Ltd Tel. No. : +27 11 692 44 Fax. No. : +27 11 412 1183 INTERNATIONAL MARKET Table 1: CME Maize prices and weekly

28 29 21 211 212 213 214 215 216 217 218 WEEKLY MAIZE REPORT 11 JULY 218 Unigrain (Pty) Ltd Tel. No. : +27 11 692 44 Fax. No. : +27 11 412 1183 INTERNATIONAL MARKET Table 1: CME Maize prices and weekly

Rick Alexander

ralexander@zaner.com NOT SEEING SHARP DROPS LATELY IN THE WHEAT COMPLEX. EXPORTS SLIGHTLY AHEAD OF 5 YEAR AVE. Posted on 8/17/2016 7:15:52 AM WE HAVE A VERY GOOD HEDGING DEPARTMENT HEADED BY TED SEIFRIED.

ralexander@zaner.com NOT SEEING SHARP DROPS LATELY IN THE WHEAT COMPLEX. EXPORTS SLIGHTLY AHEAD OF 5 YEAR AVE. Posted on 8/17/2016 7:15:52 AM WE HAVE A VERY GOOD HEDGING DEPARTMENT HEADED BY TED SEIFRIED.

In this week we enlighten you about peanuts from the USA, Argentina and China.

Dear client, In this week we enlighten you about peanuts from the USA, Argentina and China. USA From the USA there is still a stock of about 950,000 metric farmer tons left from the 2013 crop. Though this

Dear client, In this week we enlighten you about peanuts from the USA, Argentina and China. USA From the USA there is still a stock of about 950,000 metric farmer tons left from the 2013 crop. Though this

India. Oilseeds and Products Update. August 2012

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Required Report - public distribution Oilseeds and Products

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Required Report - public distribution Oilseeds and Products

MONTHLY REPORTS EDIBLE OIL JUNE - JULY 2016

MONTHLY REPORTS EDIBLE OIL Monthly Prices Movement Edible Oil prices remained volatile in June month tracking movement in Indian Rupee and uncertain fundamentals. Soy Oil prices remained mixed with more

MONTHLY REPORTS EDIBLE OIL Monthly Prices Movement Edible Oil prices remained volatile in June month tracking movement in Indian Rupee and uncertain fundamentals. Soy Oil prices remained mixed with more

J / A V 9 / N O.

July/Aug 2003 Volume 9 / NO. 7 See Story on Page 4 Implications for California Walnut Producers By Mechel S. Paggi, Ph.D. Global production of walnuts is forecast to be up 3 percent in 2002/03 reaching

July/Aug 2003 Volume 9 / NO. 7 See Story on Page 4 Implications for California Walnut Producers By Mechel S. Paggi, Ph.D. Global production of walnuts is forecast to be up 3 percent in 2002/03 reaching

Coffee prices rose slightly in January 2019

Coffee prices rose slightly in January 2019 In January 2019, the ICO composite indicator rose by 0.9% to 101.56 US cents/lb as prices for all group indicators increased. After starting at a low of 99.16

Coffee prices rose slightly in January 2019 In January 2019, the ICO composite indicator rose by 0.9% to 101.56 US cents/lb as prices for all group indicators increased. After starting at a low of 99.16

Downward correction as funds respond to increasingly positive supply outlook

Downward correction as funds respond to increasingly positive supply outlook Coffee prices fell sharply at the end of April as institutional investors sold off their positions. The coffee market continues

Downward correction as funds respond to increasingly positive supply outlook Coffee prices fell sharply at the end of April as institutional investors sold off their positions. The coffee market continues

Milk and Milk Products. Price and Trade Update. Weekly Newsletter. Milk and Milk Products. Price and Trade Update: April

April Milk and Milk Products Price and Trade Update Weekly Newsletter Milk and Milk Products Price and Trade Update: April 1 PRICES: Remain depressed International dairy product prices began the year at

April Milk and Milk Products Price and Trade Update Weekly Newsletter Milk and Milk Products Price and Trade Update: April 1 PRICES: Remain depressed International dairy product prices began the year at

Coffee market remains volatile but lacks direction

Coffee market remains volatile but lacks direction Prices fluctuated significantly during August, with the ICO composite indicator dropping by 10 cents before jumping back up another 12 cents by the end

Coffee market remains volatile but lacks direction Prices fluctuated significantly during August, with the ICO composite indicator dropping by 10 cents before jumping back up another 12 cents by the end

WEEKLY MAIZE REPORT 13 DECEMBER 2017

90/91 91/92 92/93 93/94 94/95 95/96 96/97 97/98 98/99 99/00 00/01 01/02 02/03 03/04 04/05 05/06 06/07 07/08 08/09 09/10 10/11 11/12 12/13 13/14 14/15 15/16 16/17 17/18 WEEKLY MAIZE REPORT 13 DECEMBER 2017

90/91 91/92 92/93 93/94 94/95 95/96 96/97 97/98 98/99 99/00 00/01 01/02 02/03 03/04 04/05 05/06 06/07 07/08 08/09 09/10 10/11 11/12 12/13 13/14 14/15 15/16 16/17 17/18 WEEKLY MAIZE REPORT 13 DECEMBER 2017

Outlook for FCOJ in 2019/20

December 2018 Outlook for FCOJ in 2019/20 The Orange Juice Market Moves Towards Balance RaboResearch Food & Agribusiness far.rabobank.com Andrés Padilla Senior Analyst Beverages +55 11 5503 7000 Contents

December 2018 Outlook for FCOJ in 2019/20 The Orange Juice Market Moves Towards Balance RaboResearch Food & Agribusiness far.rabobank.com Andrés Padilla Senior Analyst Beverages +55 11 5503 7000 Contents

MONTHLY REPORTS PULSES JUNE - JULY 2016

MONTHLY REPORTS PULSES Monthly Prices Movement Pulses prices overall remained firm throughout the month amid expectation of lower output, delayed Monsoon despite strict government measures to control price

MONTHLY REPORTS PULSES Monthly Prices Movement Pulses prices overall remained firm throughout the month amid expectation of lower output, delayed Monsoon despite strict government measures to control price

Ramacafe September 2008 Judith Ganes-Chase

Implications of Rising Costs Ramacafe September 2008 Judith Ganes-Chase Factors Influencing Coffee Production Trends Weather (especially Brazil) Producers continued drive to add value to production Consumers

Implications of Rising Costs Ramacafe September 2008 Judith Ganes-Chase Factors Influencing Coffee Production Trends Weather (especially Brazil) Producers continued drive to add value to production Consumers

Record exports in coffee year 2017/18

Record exports in coffee year 2017/18 Total coffee exports increased each year since 2010/11 with a new record reached in 2017/18 at 121.86 million bags, 2% higher than 2016/17. In the twelve months ending

Record exports in coffee year 2017/18 Total coffee exports increased each year since 2010/11 with a new record reached in 2017/18 at 121.86 million bags, 2% higher than 2016/17. In the twelve months ending

Coffee market continues downward trend

Coffee market continues downward trend Since August 2017, the ICO composite indicator price has declined in each month except January 2018. The composite indicator decreased by 1.1% in March 2018 to an

Coffee market continues downward trend Since August 2017, the ICO composite indicator price has declined in each month except January 2018. The composite indicator decreased by 1.1% in March 2018 to an

Dairy Market. Overview. Commercial Use of Dairy Products

Dairy Market Dairy Management Inc. R E P O R T Volume 19 No. 2 February 2016 DMI NMPF Overview U.S. milk production continues to grow at an annual rate of less than 1 percent, and domestic commercial use

Dairy Market Dairy Management Inc. R E P O R T Volume 19 No. 2 February 2016 DMI NMPF Overview U.S. milk production continues to grow at an annual rate of less than 1 percent, and domestic commercial use

WORLD SUGAR REPORT. January 4, Published by McKeany-Flavell Co., Inc. (510)

") WORLD SUGAR REPORT January 4, 2017 Published by McKeany-Flavell Co., Inc. www.mckeanyflavell.com (510) 832-2866 WORLD SUGAR SUPPLY & DEMAND (World Table 1) After a fall to oversold levels, world raw sugar

WORLD SUGAR REPORT January 4, 2017 Published by McKeany-Flavell Co., Inc. www.mckeanyflavell.com (510) 832-2866 WORLD SUGAR SUPPLY & DEMAND (World Table 1) After a fall to oversold levels, world raw sugar

Dairy Outlook. December By Jim Dunn Professor of Agricultural Economics, Penn State University. Market Psychology

Dairy Outlook December 2015 By Jim Dunn Professor of Agricultural Economics, Penn State University Market Psychology The Class III market has taken a beating lately as cheese prices have drifted down and

Dairy Outlook December 2015 By Jim Dunn Professor of Agricultural Economics, Penn State University Market Psychology The Class III market has taken a beating lately as cheese prices have drifted down and

Fresh Deciduous Fruit (Apples, Grapes, & Pears): World Markets and Trade

: World Markets and Trade") Fresh Deciduous Fruit (Apples, Grapes, & Pears): World Markets and Trade June 21 APPLES Record Production but Trade Estimate Revised Downward The world production estimate for 29/1 is virtually unchanged

Fresh Deciduous Fruit (Apples, Grapes, & Pears): World Markets and Trade June 21 APPLES Record Production but Trade Estimate Revised Downward The world production estimate for 29/1 is virtually unchanged

Coffee market ends 2017/18 in surplus

Coffee market ends 217/18 in surplus World coffee production in coffee year 217/18 is estimated 5.7% higher at 164.81 million bags as output of Arabica increased by 2.2% to 11.82, and Robusta grew 11.7%

Coffee market ends 217/18 in surplus World coffee production in coffee year 217/18 is estimated 5.7% higher at 164.81 million bags as output of Arabica increased by 2.2% to 11.82, and Robusta grew 11.7%

MARKET REPORT. November 2017

MARKET REPORT November 2017 B E R G A M O T O I L - I TA LY Favorable growing conditions over the winter and spring time provided the right environment for when the trees start to blossom (April) resulting

MARKET REPORT November 2017 B E R G A M O T O I L - I TA LY Favorable growing conditions over the winter and spring time provided the right environment for when the trees start to blossom (April) resulting

WEEKLY OILSEED REPORT 27 JUNE 2018

WEEKLY OILSEED REPORT 27 JUNE 218 Unigrain (Pty) Ltd Tel. No. : +27 11 692 44 Fax. No. : +27 11 412 1183 INTERNATIONAL MARKET Table 1: CME Soybean prices and weekly change (cents/bushel) Currently 2/6/218

WEEKLY OILSEED REPORT 27 JUNE 218 Unigrain (Pty) Ltd Tel. No. : +27 11 692 44 Fax. No. : +27 11 412 1183 INTERNATIONAL MARKET Table 1: CME Soybean prices and weekly change (cents/bushel) Currently 2/6/218

Dairy Market. November 2017

Dairy Market Dairy Management Inc. R E P O R T Volume 20 No. 10 November 2017 DMI NMPF Overview U.S. Cheddar cheese prices hit a 10-month high in October, while butter prices softened but remained well

Dairy Market Dairy Management Inc. R E P O R T Volume 20 No. 10 November 2017 DMI NMPF Overview U.S. Cheddar cheese prices hit a 10-month high in October, while butter prices softened but remained well

World sugar market. Platts/Kingsman EU conference Geneva 14th of April Benoît Boisleux

World sugar market Platts/Kingsman EU conference Geneva 14th of April 215 Benoît Boisleux One year evolution of world prices NY 11 (2 nd month continuation) Cts/lb 2 Kingsman EU conf 8 April 214 NY 2nd

World sugar market Platts/Kingsman EU conference Geneva 14th of April 215 Benoît Boisleux One year evolution of world prices NY 11 (2 nd month continuation) Cts/lb 2 Kingsman EU conf 8 April 214 NY 2nd

World of sugar PAGE 54

World of sugar More than 1 countries produce sugar, about 8% of which is made from sugar cane grown primarily in the tropical and sub-tropical zones of the southern hemisphere, and the balance from sugar

World of sugar More than 1 countries produce sugar, about 8% of which is made from sugar cane grown primarily in the tropical and sub-tropical zones of the southern hemisphere, and the balance from sugar

Commodity Market Monthly

Commodity Market Monthly Research Department, Commodities Unit June 1, 216 www.imf.org/commodities commodities@imf.org Commodity prices surged 6. percent in May, extending gains for fourth consecutive

Commodity Market Monthly Research Department, Commodities Unit June 1, 216 www.imf.org/commodities commodities@imf.org Commodity prices surged 6. percent in May, extending gains for fourth consecutive

Dairy Market. May 2016

Dairy Market R E P O R T Volume 19 No. 5 May 2016 DMI NMPF Overview Increased production per cow and expectations for additional milk production growth is dampening the outlook for milk prices for the

Dairy Market R E P O R T Volume 19 No. 5 May 2016 DMI NMPF Overview Increased production per cow and expectations for additional milk production growth is dampening the outlook for milk prices for the

WEEKLY MAIZE REPORT 30 OCTOBER 2018

WEEKLY MAIZE REPORT 30 OCTOBER 2018 Unigrain (Pty) Ltd Tel. No. : +27 11 692 4400 Fax. No. : +27 11 412 1183 INTERNATIONAL MARKET Table 1: CME Maize prices and weekly changes (cents/bushel) Currently 23/10/2018

WEEKLY MAIZE REPORT 30 OCTOBER 2018 Unigrain (Pty) Ltd Tel. No. : +27 11 692 4400 Fax. No. : +27 11 412 1183 INTERNATIONAL MARKET Table 1: CME Maize prices and weekly changes (cents/bushel) Currently 23/10/2018

Tea Statistics Report 2015

Tea Statistics Report 215 Introduction This report presents the scope and scale of the UTZ tea program in 215. Throughout this report tea also includes rooibos unless otherwise specified. The statistics

Tea Statistics Report 215 Introduction This report presents the scope and scale of the UTZ tea program in 215. Throughout this report tea also includes rooibos unless otherwise specified. The statistics

Wheat Summary. MF Global Daily Report

US research@mfglobal.com April 7, 2011 Wheat Summary MF Global Daily Report MF Global Inc. 440 S. LaSalle 20th Floor Chicago, IL 60605 Review Markets that are being supported by weather concerns always

US research@mfglobal.com April 7, 2011 Wheat Summary MF Global Daily Report MF Global Inc. 440 S. LaSalle 20th Floor Chicago, IL 60605 Review Markets that are being supported by weather concerns always

Coffee Season 2013/14 Finishes in Balance but Deficit Expected Next Year

Coffee Season 2013/14 Finishes in Balance but Deficit Expected Next Year Coffee prices were volatile again over the course of September, mostly reacting to weather news from Brazil. Daily prices fell initially

Coffee Season 2013/14 Finishes in Balance but Deficit Expected Next Year Coffee prices were volatile again over the course of September, mostly reacting to weather news from Brazil. Daily prices fell initially

Water Street Solutions Aerial Crop Tour /30/15

Water Street Solutions Aerial Crop Tour 2015 7/30/15 1 When we left Peoria, IL, we flew northwest to Geneseo, IL. The crop was as I expected for the first half of the route. The second half from Toulon,

Water Street Solutions Aerial Crop Tour 2015 7/30/15 1 When we left Peoria, IL, we flew northwest to Geneseo, IL. The crop was as I expected for the first half of the route. The second half from Toulon,

Heeren E-Market Report

December 19, 2016 Overview Garlic will remain in an extreme market. We see Iceberg getting tighter. Cauliflower is also in an extreme market as we are seeing a shortage in supply and prices are escalated.

December 19, 2016 Overview Garlic will remain in an extreme market. We see Iceberg getting tighter. Cauliflower is also in an extreme market as we are seeing a shortage in supply and prices are escalated.

July marks another month of continuous low prices

July marks another month of continuous low prices In July 2018, the ICO composite indicator price decreased by 2.9% to an average of 107.20 US cents/lb, which is the lowest monthly average for July since

July marks another month of continuous low prices In July 2018, the ICO composite indicator price decreased by 2.9% to an average of 107.20 US cents/lb, which is the lowest monthly average for July since

Dairy Market. Overview. Commercial Use of Dairy Products. U.S. Dairy Trade

Dairy Market Dairy Management Inc. R E P O R T Volume 19 No. 11 November 2016 DMI NMPF Overview Four straight months of rising milk prices and three straight months of falling feed costs have brought some

Dairy Market Dairy Management Inc. R E P O R T Volume 19 No. 11 November 2016 DMI NMPF Overview Four straight months of rising milk prices and three straight months of falling feed costs have brought some

Dairy Market. May 2017

Dairy Market Dairy Management Inc. R E P O R T Volume 20 No. 4 May 2017 DMI NMPF Overview The rate of milk production growth began to moderate during the first quarter, but additional milk production continues

Dairy Market Dairy Management Inc. R E P O R T Volume 20 No. 4 May 2017 DMI NMPF Overview The rate of milk production growth began to moderate during the first quarter, but additional milk production continues

Dairy Market R E P O R T

Volume 18 No. 12 Dairy Market R E P O R T D e c e m b e r 2 0 1 5 DMI NMPF Overview The U.S. average all-milk price, which spent seven months of 2015 hovering around $16.70 per hundredweight, has moved

Volume 18 No. 12 Dairy Market R E P O R T D e c e m b e r 2 0 1 5 DMI NMPF Overview The U.S. average all-milk price, which spent seven months of 2015 hovering around $16.70 per hundredweight, has moved

Commitment of. Traders. Managed Money. Fund Positions

October 19, 2018 Market Summary Corn started the week off strong, closing Monday up 4 cents at $3.77 1/4, which marked the highest close since August 20th. Nov soybeans also managed their highest daily

October 19, 2018 Market Summary Corn started the week off strong, closing Monday up 4 cents at $3.77 1/4, which marked the highest close since August 20th. Nov soybeans also managed their highest daily

Coffee market recovers slightly from December slump

Coffee market recovers slightly from December slump After reaching its lowest level in 22 months in December 2017, the monthly average of the ICO composite indicator price increased by 1.4% to 115.60 US

Coffee market recovers slightly from December slump After reaching its lowest level in 22 months in December 2017, the monthly average of the ICO composite indicator price increased by 1.4% to 115.60 US

CropCast Global Coffee Estimates

CropCast Weekly Report Kenny Miller Tuesday, June 06, 2017 CropCast Global Estimates AREA (th hectares) YIELD (kg/ha) PRODUCTION (M bags) 16/17 17/18 16/17 17/18 16/17 17/18 South America 4281 4206 994

CropCast Weekly Report Kenny Miller Tuesday, June 06, 2017 CropCast Global Estimates AREA (th hectares) YIELD (kg/ha) PRODUCTION (M bags) 16/17 17/18 16/17 17/18 16/17 17/18 South America 4281 4206 994

Market Outlook GLOBAL DAIRY. *Mid-point of range. Milk powder, cheese and butterfat are Oceania; whey is EU.

U.S. exports (MT, Jan-Dec): NDM/SMP 444,727 2% CHEESE 260,033 16% WHEY 468,144 4% BUTTERFAT 46,019-27% Details: PAGE 3 February 28, 2013 Volume 17 No.2 GLOBAL DAIRY Market Outlook U.S. Dairy Export Council

U.S. exports (MT, Jan-Dec): NDM/SMP 444,727 2% CHEESE 260,033 16% WHEY 468,144 4% BUTTERFAT 46,019-27% Details: PAGE 3 February 28, 2013 Volume 17 No.2 GLOBAL DAIRY Market Outlook U.S. Dairy Export Council

UTZ Coffee Statistics Report 2017

UTZ Coffee Statistics Report 2017 UTZ is the largest certification program in the world for sustainable coffee More than 480,000 coffee farmers and workers benefit from the UTZ program UTZ certified coffee

UTZ Coffee Statistics Report 2017 UTZ is the largest certification program in the world for sustainable coffee More than 480,000 coffee farmers and workers benefit from the UTZ program UTZ certified coffee

EMBARGO TO ON FRIDAY 16 SEPTEMBER. Scotch Whisky Association. Exports of Scotch Whisky; Year to end of June 2016 (2016 H1)

") EMBARGO TO 00.01 ON FRIDAY 16 SEPTEMBER Scotch Whisky Association Exports of Scotch Whisky; Year to end of June 2016 (2016 H1) VOLUME UP 3.1% to 531 MILLION bottles VALUE DOWN SLIGHTLY BY 1.0% TO 1.70

EMBARGO TO 00.01 ON FRIDAY 16 SEPTEMBER Scotch Whisky Association Exports of Scotch Whisky; Year to end of June 2016 (2016 H1) VOLUME UP 3.1% to 531 MILLION bottles VALUE DOWN SLIGHTLY BY 1.0% TO 1.70

Dairy Market. October 2016

Dairy Market Dairy Management Inc. R E P O R T Volume 19 No. 10 October 2016 DMI NMPF Overview Milk prices continued a generally solid recovery from their late-spring low through August, when the U.S.

Dairy Market Dairy Management Inc. R E P O R T Volume 19 No. 10 October 2016 DMI NMPF Overview Milk prices continued a generally solid recovery from their late-spring low through August, when the U.S.

WEEKLY MAIZE REPORT 28 NOVEMBER 2018

WEEKLY MAIZE REPORT 28 NOVEMBER 2018 Unigrain (Pty) Ltd Tel. No. : +27 11 692 4400 Fax. No. : +27 11 412 1183 INTERNATIONAL MARKET Table 1: CME Maize prices and weekly changes (cents/bushel) Currently

WEEKLY MAIZE REPORT 28 NOVEMBER 2018 Unigrain (Pty) Ltd Tel. No. : +27 11 692 4400 Fax. No. : +27 11 412 1183 INTERNATIONAL MARKET Table 1: CME Maize prices and weekly changes (cents/bushel) Currently

The supply and demand for oilseeds in South Africa

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Required Report - public distribution Date: GAIN Report

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Required Report - public distribution Date: GAIN Report

Consistently higher production and more exportable supplies from Thailand are major factors in the decline in world rice prices in 2014 and continued

Rice Consistently higher production and more exportable supplies from Thailand are major factors in the decline in world rice prices in 2014 and continued lower levels over the next ten years. Part of

Rice Consistently higher production and more exportable supplies from Thailand are major factors in the decline in world rice prices in 2014 and continued lower levels over the next ten years. Part of

Paper Packaging Practice June Copyright 2015 RISI, Inc. All rights reserved.

Global Containerboard Outlook Ken Waghorne, VP Paper Packaging Practice June 2015 1 Today s Agenda Regional Containerboard Markets Asia Europe Western Eastern North America Latin America Rest of World

Global Containerboard Outlook Ken Waghorne, VP Paper Packaging Practice June 2015 1 Today s Agenda Regional Containerboard Markets Asia Europe Western Eastern North America Latin America Rest of World