February 12 th, By Jack Scoville

|

|

|

- Hillary Barker

- 5 years ago

- Views:

Transcription

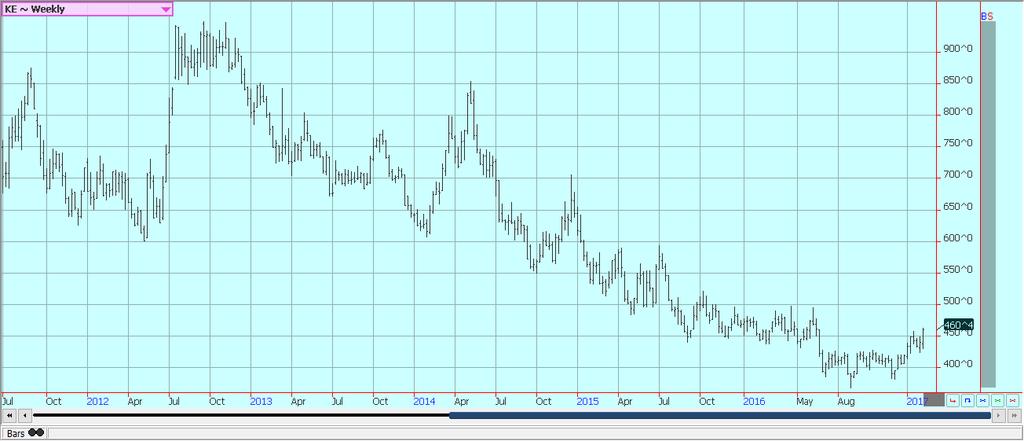

1 February 12 th, 2017 By Jack Scoville Wheat: US markets were higher last week. Prices surged after the monthly USDS supply and demand updates were released. USDA increased US export demand by 50 million bushels and cut ending stocks a like amount. The ending stocks for the US are still projected to be high at billion bushels. The big surprise came in the world data. USDA cut production and ending stocks for India and Kazakhstan and also world ending stocks. USDA cut world ending stocks estimates from million tons to million tons. The move was a surprise as the market had expected marginally lower world stocks levels. Export demand for US Wheat remains strong. US export sales are primarily for HRW and HRS as the world seeks out quality Wheat. That has helped support HRS and HRW futures on spreads against SRW, where the demand has been much more limited. Chart trends have turned up, and SRW Chicago Wheat futures are now testing an important resistance area near 450 per bushel. This resistance area could hold for now. The big world supplies and competitive nature of the market continues to limit upside potential for futures prices. But, the reduced US planted area for Winter Wheat and the potential for reduced planted area worldwide due to the current depressed prices and an increased speculative appetite to own agricultural futures should keep prices trading with a firm tone. Weekly Chicago Soft Red Winter Wheat Futures. Weekly Chicago Hard Red Winter Wheat Futures

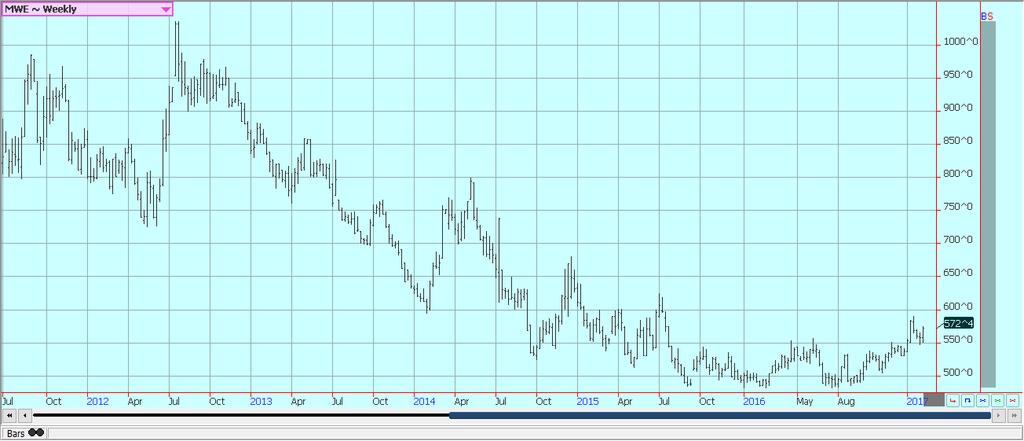

2 Weekly Minneapolis Wheat Futures

3 Corn: Corn closed higher for the week and pushed through some important resistance on the charts at the 370 area to close near the highs for the week. It was a very positive close and one that implied that more price gains are possible. USDA increased ethanol demand in its monthly supply and demand updates last week by 25 million bushels, but left export demand unchanged for now. Ending stocks re reduced to billion bushels, which is still a lot of corn to have at the end of the year and the highest projected ending stocks level in decades. Demand for Corn has been stronger than expected, especially on the export and energy fronts. Export demand was strong again last week at almost 1.0 million tons. USDA estimated world Corn ending stocks at million tons, from million in January US farmers appear undersold in Corn, but are said to begin selling in a much bigger way if the rally continues for another five to 10 cents per bushel in futures. They face little world competition as South America is still out of the market and is likely to be out of the market until this Summer. There is not much Corn there as Brazil ran out and used the extra Argentine Corn, so internal pipelines will need to be filled before much export can be made. Growing conditions are said to be good in Brazil, and the Safrinha crop is being planted as the Soybeans get harvested. Heavy rains are possible this week to slow the progress down. Conditions have improved in Argentina due to recent rains. Crop losses in Argentina are still expected from the previous bad weather. Weekly Corn Futures:,

4 Weekly Oats Futures Soybeans and Soybean Meal: Soybeans and Soybean Meal were higher last week. It was a higher week based on hopes for continued demand from potential harvest delays in Brazil and somewhat reduced production in Argentina. The harvest in Brazil has been moving right along despite reports of rains in areas ready for harvest. Mato Grosso is already over one third harvested, and harvest should be increasing around the rains in other states. Mato Grosso and surrounding areas are expected to get some heavy rains this week, but the rapid harvest pace until now should keep concerns to a minimum. Production ideas currently appear to be near or above 105 million tons. Argentina has seen improved crop conditions due to recent rains in southern areas and drier conditions in flooded areas. These general weather trends are expected to continue this week. Production estimates for Argentina now range from 52 to 55 million tons, down from 55 to 57 million tons early in the growing season. USDA left its US supply and demand estimates unchanged last week and this was considered a disappointment for Soybeans traders. It cut Argentine Soybeans production to 55.5 million tons, from 57 million last month. Brazilian Soybeans production was unchanged at 104 million tons. World ending stocks were estimated at 80.4 million tons, from 82.3 million last month. Chinese buying has been reported to be very strong since the end of the holiday week, and bigger export sales are expected this Thursday after a disappointing week of export sales last week. The market has maintained a firm tone as US prices remain competitive in the world market. Brazil prices have been trending higher as farmers there hold back on sales due to the stronger Real. The Real has rallied from about 28.5 cents to about 32 cents since December.

5 Weekly Chicago Soybeans Futures: Weekly Chicago Soybean Meal Futures

6 Rice: World markets were mixed last week. Asian prices should Vietnamese prices higher and the rest of the major exporters with steady to lower quotes. US markets were slightly higher for the week after a short covering rally on Friday. The slightly higher close was something of a victory for anyone who might be bullish the market. Anyone bullish is hard to find given the multiyear move lower. The market took increased ending stocks for the US as seen in the monthly USDA supply and demand updates in stride. USDA reduced long grain milled export demand by 2.0 million hundredweight and increased ending stocks by the same amount. The move was just facing reality as long grain milled exports have been the weak spot in the US export picture this year. World ending stocks levels were lower on lower ending stocks in India, Thailand, Burma, and Philippines. The domestic cash market remains generally slow, with both buyers and sellers not showing much interest. US farmers are still making final planting decisions and there is still widespread talk that those with alternatives will choose to plant other crops that appear to have better profit potential. Weekly Chicago Rice Futures

7 Palm Oil and Vegetable Oils: World vegetable oils markets were generally firm last week. Both Soybean Oil and Canola had strong weeks, but Palm Oil remained in a mostly sideways trade. MPOB released its monthly supply and demand statistics. Production was 1.28 million tons in January, from 1.47 million in December. Exports were 1.28 million tons, from 1.27 million tons in December. Ending stocks were 1.54 million tons, from 1.67 million the previous month. The data showed lower ending stocks levels due to lower than expected production. Exports were about as expected. However, the private surveyors showed that exports are off to a slower start this month. SGS said that Malaysian Palm Oil exports are 337,282 tons, from 338,777 tons last month. ITS said exports were 340,947 tons, from 351,907 tons last month. The export data appeared to be the more important factor in the price action on Friday. Meanwhile, Soybean Oil prices held and moved away from a support area on the weekly charts. US demand has been good, especially from the bio fuels sector. The bio fuels sector has also been importing from Argentina. The Argentine imports might stop in the near future as Congress is not expected to renew some tax credits that allowed the imports to happen. Biofuels demand should remain strong and should grow over time in the world market. Overall world vegetable oil demand should remain good. Soybean Oil should get more of this demand as it is relatively cheap on spreads to Palm Oil. Palm Oil production is expected to increase in the next few months as the trees there recover from El Nino, but the recovery has been slower than expected. Weekly Malaysian Palm Oil Futures:

8 Weekly Chicago Soybean Oil Futures Weekly Canola Futures:

9 Cotton: Futures were lower for the week. the weekly export sales were down from the last few weeks, but this could be reflecting the lost demand from China and Southeast Asia due to the Lunar New Year. USDA showed the export strength in its monthly supply and demand updates. Exports were increased by 200,000 bales to 12.7 million, and ending stocks were trimmed to 4.8 million bales from 5.0 million last month. World ending stocks levels were reduced, mostly due to less stocks in exporter countries as importer stocks are expected to increased slightly. Next target for the market is a weekly high at 7780 March, but chart patterns suggest that prices can now move over 8000 in the near term. The weekly charts show that the longer term uptrend remains intact. Speculators are the major longs and commercials are the major shorts. This may start to change as trade talk suggests that the commercials have to price a significant amount on call Cotton before First Notice Day for March contracts in the next couple of weeks. The commercials have been bearish the market due to ideas of big US domestic supplies, but the stronger than expected demand and ideas that more inflation is coming have been the main factor behind the buying by speculators. Weekly US Cotton Futures Frozen Concentrated Orange Juice and Citrus: FCOJ closed a little higher last week, but held well within recent trading ranges. Chart patterns suggest that there is more down side potential with final objectives near or below basis the nearest futures contract. USDA now estimates Florida Oranges production at 70 million boxes, a very low amount. The Greening Disease remains the overriding factor for reduced production, but the state has also been dry. Irrigation is being used to support blooms for the next crop. The Florida harvest remains active amid dry and warm weather conditions. Early and Mid oranges are being harvested for processing. The Valencia harvest is moving quickly. Demand for Orange Juice inside the US is still a big problem. It is currently at its lowest level since records started being kept in 2002, and there are no real prospects for improvement right now as consumers have plenty of alternatives. Sao Paulo state is getting good weather and crop conditions are called good. Brazil should be able to fill world demand this year and has been an active seller into the US in recent weeks. The Brazil imports are helping to keep inventories at comfortable levels, especially when the weaker demand is factored in.

10 Weekly FCOJ Futures Coffee: Futures were a little lower again last week. The demand side of the market was quiet t the start of the week, but got more animated near the end of the week as futures prices started to hold and recover some of the losses. Futures in New York have seen selling pressure for a month now, and futures prices in London have felt selling pressure for a couple of weeks. There has not been any real change in the fundamentals. There is less production in Brazil this year, in part because it is the second year of the biennial cycle and in part due to the drought in northeast Brazil. Production ideas range from 45 to 50 million bags. Offers are less and seen at high prices from Robusta countries such as Vietnam, and has been a short crop there as well due to dry weather at flowering time. Vietnamese prices have started to drop a little bit as demand has shifted to other countries. The demand has been great for inferior qualities of Coffee from the rest of Latin America, although prices paid remain low and differentials paid remain weak. Differentials for better qualities are stable. Brazil exported 2.6 million bags of Coffee in January, down 8.7% from December. Arabica exports were down 3.9% to 2.4 million bags and Robusta exports were down 71.7% at 22,118 bags. The lower export pace from Brazil is being covered by other Latin American countries.

11 Weekly New York Arabica Coffee Futures Weekly London Robusta Coffee Futures

12 Sugar: Futures closed lower after failing to break out from resistance at the top end of the current trading range. New York closed within the range seen for the last month and a half, but London is now pushing through the support zone. Part of the selling is coming as the March contract will go into delivery in London this week and in New York at the end of the month. Long speculators are closing out positions, and for now the commercial is only providing partial buying interest. News of less than expected production in Brazil combined with less on offer from India and Thailand provide the best reasons for strong prices. India continues to debate the need for imports, and most analysts expect the country to import at least some Sugar. The government is still saying no imports are needed and has maintained a high import tariff. However, mills are closing early this year as there is little Cane to process. Internal prices are moving higher. China has imported significantly less Sugar as it continues to liquidate supplies in government storage by selling them into the local cash market. Demand from North Africa and the Middle East is consistent. The weather in Latin American countries away from Brazil appears to be mostly good, although northeast Brazil remain too dry. Northeast Brazil could see some very beneficial rains this week. Most of Southeast Asia has had good rains.

13 Weekly New York World Raw Sugar Futures Weekly London White Sugar Futures

14 Cocoa: Futures markets were lower and moved to new lows on the charts in New York and in London. The lower prices are starting to hurt West Africa exporters who sold cheap and did not cover in domestic cash markets. The situation has hurt prices in Ivory Coast even more, and now some producers are leaving pods on trees and letting them rot as there is no money to be made by picking and processing. Overall price action remains weak as the main crop harvest continues in West Africa under good weather conditions. The demand from Europe is reported improved, but still weak over all, and the North American demand has been weaker than anticipated. Supplies in storage in Europe are reported to be very high. The next production cycle still appears to be big as the growing conditions around the world are generally very good. West Africa has seen much better rains this year and now getting warm and dry weather. Traders will watch now to see if Harmattan winds develop that could decimate the mid crop. East Africa is getting enough rain now, and overall production conditions are now called good. Good conditions are still being reported in Southeast Asia. Weekly New York Cocoa Futures

15 Weekly London Cocoa Futures Dairy and Meat: Dairy markets were mostly a little lower as good supplies of milk remain available to the market. Demand is good for cream, but cheese makers have started to back away from the market. Bottled milk demand has been mostly strong, but the Midwest is reporting less demand. Production has been seasonally strong in the east and west and stable in the Midwest. Production has been lower in the mountains due to recent bad weather. Butter and cheese manufacturers report that inventories are starting to increase as there is a lot of milk available. This is especially true for Butter, where bulk supplies are going to storage. Cheese supplies are increasing and much of the production is going into aging coolers. Midwest cheese makers are pulling back on taking new milk. Butter manufacturers are mostly producing bulk butter for inventories. Aged inventories are increasing. Dried products prices are mixed. Whey prices are mixed to strong, and whole milk prices are stable. NDM prices are stable to weak. International markets are featuring higher prices due to reduced production. Production is less in Europe and Russia. Export demand for New Zealand has increased due to stronger demand from China. Production is in a short term decline due to poor pasture conditions. On the other hand, hay supplies in Australia are good even with reports of lower production in January. South American prices are firm as raw milk production goes into a seasonal decline. Argentina is seeing weaker production due to big storms in central and northern areas that has also affected production in parts of Uruguay. Export demand from both countries has been strong, especially from Brazil and Russia. Brazil production is down on hotter weather, especially in southern areas. US cattle and beef prices were firm last week as packers reached for supplies. Feedlot offers were good, but weights are down, and there is talk that Cattle sup0plies might be light for the next several weeks. The Cattle on Feed and semiannual inventory reports showed that there is plenty of cattle out there. However, it appears that a lot of the cattle is not yet ready for market. Packers appear short bought. Ideas are that prices can hold at higher levels for now, but that weaker prices will be seen once feedlot offers start to increase in a few months. The supply and demand reports showed good demand for beef for the year. Australia has less to offer and very high prices. Herd culling has slackened in both Australia and New Zealand. Pasture conditions in both countries

16 is better than a year ago on colder and wetter weather seen until now. Conditions in Australia are very good and surplus hay is reported in many areas. New Zealand now needs drier weather to promote growth.

17 Pork markets have been firm, and live hog futures trends are mostly up. Pork demand remains stronger than expected and ham prices have been contra seasonally strong. The monthly supply and demand updates from USDA showed that strong pork demand can continue on the domestic and export fronts. The demand should help keep supplies available to the market under control at a time when hogs production remains very strong. Pork prices have trended higher in retail and wholesale markets. Export prices have been strong as well. Packer demand has been very good as packers move to meet the strong domestic and world demand. The charts show that the market could remain higher, and strong demand ideas should continue to support the market overall. Weekly Chicago Class 3 Milk Futures

18 Weekly Chicago Cheese Futures Weekly Chicago Butter Futures

19 Weekly Chicago Live Cattle Futures: Weekly Feeder Cattle Futures:

20 Weekly Chicago Lean Hog Futures: Futures and options trading involves substantial risk of loss and may not be suitable for everyone. The valuation of futures and options may fluctuate and as a result, clients may lose more than their original investment. In no event should the content of this website be construed as an express or implied promise, guarantee, or implication by or from The PRICE Futures Group, Inc. that you will profit or that losses can or will be limited whatsoever. Past performance is not indicative of future results. Information provided on this report is intended solely for informative purpose and is obtained from sources believed to be reliable. No guarantee of any kind is implied or possible where projections of future conditions are attempted. The leverage created by trading on margin can work against you as well as for you, and losses can exceed your entire investment. Before opening an account and trading, you should seek advice from your advisors as appropriate to ensure that you understand the risks and can withstand the losses.

October 8th, By Jack Scoville

October 8th, 2018 By Jack Scoville Wheat: Wheat was higher last week as world prices held firm. Firm prices extend from Russia to Australia on reduced world production. It remains very dry in Australia,

October 8th, 2018 By Jack Scoville Wheat: Wheat was higher last week as world prices held firm. Firm prices extend from Russia to Australia on reduced world production. It remains very dry in Australia,

February 11th, By Jack Scoville

February 11th, 2019 By Jack Scoville Wheat: Winter Wheat markets were lower for the week last week. Chicago SRW prices held firm on Friday in response to news that Egypt had bought 120,000 tons of SRW.

February 11th, 2019 By Jack Scoville Wheat: Winter Wheat markets were lower for the week last week. Chicago SRW prices held firm on Friday in response to news that Egypt had bought 120,000 tons of SRW.

January 8 th, By Jack Scoville

January 8 th, 2017 By Jack Scoville Wheat: US markets were higher for the week. The weekly charts show that trends are turning up in Chicago SRW and have already turned up in Chicago HRW and Minneapolis.

January 8 th, 2017 By Jack Scoville Wheat: US markets were higher for the week. The weekly charts show that trends are turning up in Chicago SRW and have already turned up in Chicago HRW and Minneapolis.

January 15th, By Jack Scoville

January 15th, 2017 By Jack Scoville Wheat: US markets closed lower on Friday and lower for the week in response to the USDA planted area estimates. USDA showed higher than expected planted area for all

January 15th, 2017 By Jack Scoville Wheat: US markets closed lower on Friday and lower for the week in response to the USDA planted area estimates. USDA showed higher than expected planted area for all

August 13th, By Jack Scoville

August 13th, 2018 By Jack Scoville Wheat: Wheat closed lower last week, with most of the selling coming on Friday in response to the USDA production and supply and demand reports. The US data was somewhat

August 13th, 2018 By Jack Scoville Wheat: Wheat closed lower last week, with most of the selling coming on Friday in response to the USDA production and supply and demand reports. The US data was somewhat

April 16th, By Jack Scoville

April 16th, 2018 By Jack Scoville Wheat: Wheat markets were near unchanged in Chicago as weather and demand remained the dominant factors in the market. Kansas City was lower for the week, while Minneapolis

April 16th, 2018 By Jack Scoville Wheat: Wheat markets were near unchanged in Chicago as weather and demand remained the dominant factors in the market. Kansas City was lower for the week, while Minneapolis

February 25th, By Jack Scoville

February 25th, 2019 By Jack Scoville Wheat: Winter Wheat markets were mostly a little higher on Friday, but lower for the week. World Wheat prices were softer as well. USDA released its export sales report

February 25th, 2019 By Jack Scoville Wheat: Winter Wheat markets were mostly a little higher on Friday, but lower for the week. World Wheat prices were softer as well. USDA released its export sales report

March 25th, By Jack Scoville

March 25th, 2019 By Jack Scoville Wheat: Winter Wheat markets were higher and Minneapolis Spring Wheat prices closed slightly higher for the week. Chicago SRW prices are now above important resistance

March 25th, 2019 By Jack Scoville Wheat: Winter Wheat markets were higher and Minneapolis Spring Wheat prices closed slightly higher for the week. Chicago SRW prices are now above important resistance

December 17th, By Jack Scoville

December 17th, 2017 By Jack Scoville Wheat: US markets closed slightly lower again in Chicago last week as demand from the export market remains a big problem. Futures also closed lower in Minneapolis,

December 17th, 2017 By Jack Scoville Wheat: US markets closed slightly lower again in Chicago last week as demand from the export market remains a big problem. Futures also closed lower in Minneapolis,

September 10th, By Jack Scoville

September 10th, 2018 By Jack Scoville Wheat: Wheat markets were lower last week on reports of softer prices in Europe and Russia. The market keeps it focus primarily on Russia and the prices it sells Wheat

September 10th, 2018 By Jack Scoville Wheat: Wheat markets were lower last week on reports of softer prices in Europe and Russia. The market keeps it focus primarily on Russia and the prices it sells Wheat

May 14th, By Jack Scoville

May 14th, 2018 By Jack Scoville Wheat: Wheat markets were lower, with much of the selling in reaction to the USDA reports released on Thursday. The reports showed increased production estimates from a

May 14th, 2018 By Jack Scoville Wheat: Wheat markets were lower, with much of the selling in reaction to the USDA reports released on Thursday. The reports showed increased production estimates from a

May 21st, By Jack Scoville

May 21st, 2018 By Jack Scoville Wheat: Wheat markets were higher on uncertain production prospects at home and increasingly in other producing countries. The dry conditions in the western Great Plains,

May 21st, 2018 By Jack Scoville Wheat: Wheat markets were higher on uncertain production prospects at home and increasingly in other producing countries. The dry conditions in the western Great Plains,

October 22nd, By Jack Scoville

October 22nd, 2017 By Jack Scoville Wheat: US markets were lower last week in all three markets. The trade remains concerned about demand even though the weekly export sales report was strong last week.

October 22nd, 2017 By Jack Scoville Wheat: US markets were lower last week in all three markets. The trade remains concerned about demand even though the weekly export sales report was strong last week.

March 19 th, By Jack Scoville

March 19 th, 2017 By Jack Scoville Wheat: US markets were higher and closed the week on a strong note. Chicago SRW futures could complete a test of the lows and indicate a new up trend is underway if some

March 19 th, 2017 By Jack Scoville Wheat: US markets were higher and closed the week on a strong note. Chicago SRW futures could complete a test of the lows and indicate a new up trend is underway if some

April 30th, By Jack Scoville

April 30th, 2018 By Jack Scoville Wheat: Wheat markets were higher as weather and demand remained the dominant factors in the market. It remains very dry in western parts of the Great Plains, and crop

April 30th, 2018 By Jack Scoville Wheat: Wheat markets were higher as weather and demand remained the dominant factors in the market. It remains very dry in western parts of the Great Plains, and crop

April 9th, By Jack Scoville

April 9th, 2018 By Jack Scoville Wheat: Wheat markets were higher as weather returned as a dominant factor in the market. Forecasts still call for dry weather in Texas and Oklahoma and it is dry again

April 9th, 2018 By Jack Scoville Wheat: Wheat markets were higher as weather returned as a dominant factor in the market. Forecasts still call for dry weather in Texas and Oklahoma and it is dry again

September 3rd, By Jack Scoville

September 3rd, 2017 By Jack Scoville Wheat: US markets were mixed, with Chicago markets moving higher and Minneapolis markets moving lower. Minneapolis moved lower on bigger than expected production projections

September 3rd, 2017 By Jack Scoville Wheat: US markets were mixed, with Chicago markets moving higher and Minneapolis markets moving lower. Minneapolis moved lower on bigger than expected production projections

Dairy Market. May 2016

Dairy Market R E P O R T Volume 19 No. 5 May 2016 DMI NMPF Overview Increased production per cow and expectations for additional milk production growth is dampening the outlook for milk prices for the

Dairy Market R E P O R T Volume 19 No. 5 May 2016 DMI NMPF Overview Increased production per cow and expectations for additional milk production growth is dampening the outlook for milk prices for the

World coffee consumption increases but prices still low

World coffee consumption increases but prices still low The coffee market stabilised slightly in February, but prices remain at very low levels. A lack of news regarding fundamentals with expectations

World coffee consumption increases but prices still low The coffee market stabilised slightly in February, but prices remain at very low levels. A lack of news regarding fundamentals with expectations

Monthly Economic Letter

Monthly Economic Letter Cotton Market Fundamentals & Price Outlook RECENT PRICE MOVEMENT NY futures experienced volatility recently, with the net effect being a slight increase in prices. The A Index also

Monthly Economic Letter Cotton Market Fundamentals & Price Outlook RECENT PRICE MOVEMENT NY futures experienced volatility recently, with the net effect being a slight increase in prices. The A Index also

Soft Commodity Markets - Upcoming Milestones, and How the Market Could Be Affected

Soft Commodity Markets - Upcoming Milestones, and How the Market Could Be Affected September 15, 2014 Judith Ganes President J. Ganes Consulting, LLC Weather & Politics Current Weather Expectations El

Soft Commodity Markets - Upcoming Milestones, and How the Market Could Be Affected September 15, 2014 Judith Ganes President J. Ganes Consulting, LLC Weather & Politics Current Weather Expectations El

Monthly Economic Letter

Monthly Economic Letter Cotton Market Fundamentals & Price Outlook RECENT PRICE MOVEMENT After falling in the days surrounding the release of last month s USDA report, NY futures and the A Index were mostly

Monthly Economic Letter Cotton Market Fundamentals & Price Outlook RECENT PRICE MOVEMENT After falling in the days surrounding the release of last month s USDA report, NY futures and the A Index were mostly

Volatility returns to the coffee market as prices stay low

Volatility returns to the coffee market as prices stay low Daily coffee prices hit their lowest level in 19 months during August, as commodity markets worldwide were negatively affected by currency movements

Volatility returns to the coffee market as prices stay low Daily coffee prices hit their lowest level in 19 months during August, as commodity markets worldwide were negatively affected by currency movements

Coffee market ends 2014 at ten month low

Coffee market ends 2014 at ten month low Coffee prices continued to slide downwards in December 2014, with the monthly average of the ICO composite indicator at its lowest level since February. Recent

Coffee market ends 2014 at ten month low Coffee prices continued to slide downwards in December 2014, with the monthly average of the ICO composite indicator at its lowest level since February. Recent

Cocoa Prepared by Foresight October 3, 2018

Cocoa Prepared by Foresight October 3, 2018 TABLES Cocoa Bean Price Forecast... P. 4 World Cocoa Supply/Demand, Crop Year... P. 7 World Cocoa Production... P. 8 Cocoa Crops in Major Producing Countries...

Cocoa Prepared by Foresight October 3, 2018 TABLES Cocoa Bean Price Forecast... P. 4 World Cocoa Supply/Demand, Crop Year... P. 7 World Cocoa Production... P. 8 Cocoa Crops in Major Producing Countries...

WEEKLY MAIZE REPORT 13 DECEMBER 2017

90/91 91/92 92/93 93/94 94/95 95/96 96/97 97/98 98/99 99/00 00/01 01/02 02/03 03/04 04/05 05/06 06/07 07/08 08/09 09/10 10/11 11/12 12/13 13/14 14/15 15/16 16/17 17/18 WEEKLY MAIZE REPORT 13 DECEMBER 2017

90/91 91/92 92/93 93/94 94/95 95/96 96/97 97/98 98/99 99/00 00/01 01/02 02/03 03/04 04/05 05/06 06/07 07/08 08/09 09/10 10/11 11/12 12/13 13/14 14/15 15/16 16/17 17/18 WEEKLY MAIZE REPORT 13 DECEMBER 2017

Record exports from Brazil weigh heavy on the coffee market

Record exports from Brazil weigh heavy on the coffee market Coffee exports from Brazil reached a record high of 36.8 million bags in crop year 2014/15 (April to March), fuelled by domestic stocks and encouraged

Record exports from Brazil weigh heavy on the coffee market Coffee exports from Brazil reached a record high of 36.8 million bags in crop year 2014/15 (April to March), fuelled by domestic stocks and encouraged

Dairy Market. Overview. Commercial Use of Dairy Products

Dairy Market Dairy Management Inc. R E P O R T Volume 21 No. 6 June 2018 DMI NMPF Overview U.S. dairy markets received a one-two punch during the first weeks of June in the form of collateral damage from

Dairy Market Dairy Management Inc. R E P O R T Volume 21 No. 6 June 2018 DMI NMPF Overview U.S. dairy markets received a one-two punch during the first weeks of June in the form of collateral damage from

2016 China Dry Bean Historical production And Estimated planting intentions Analysis

2016 China Dry Bean Historical production And Estimated planting intentions Analysis Performed by Fairman International Business Consulting 1 of 10 P a g e I. EXECUTIVE SUMMARY A. Overall Bean Planting

2016 China Dry Bean Historical production And Estimated planting intentions Analysis Performed by Fairman International Business Consulting 1 of 10 P a g e I. EXECUTIVE SUMMARY A. Overall Bean Planting

Wheat Summary. MF Global Daily Report

US research@mfglobal.com April 7, 2011 Wheat Summary MF Global Daily Report MF Global Inc. 440 S. LaSalle 20th Floor Chicago, IL 60605 Review Markets that are being supported by weather concerns always

US research@mfglobal.com April 7, 2011 Wheat Summary MF Global Daily Report MF Global Inc. 440 S. LaSalle 20th Floor Chicago, IL 60605 Review Markets that are being supported by weather concerns always

Fresh Deciduous Fruit (Apples, Grapes, & Pears): World Markets and Trade

: World Markets and Trade") Million MT United States Department of Agriculture Foreign Agricultural Service December 21 Fresh Deciduous Fruit (Apples, Grapes, & Pears): World Markets and Trade 21/11 Forecast: World Apple Trade Declines;

Million MT United States Department of Agriculture Foreign Agricultural Service December 21 Fresh Deciduous Fruit (Apples, Grapes, & Pears): World Markets and Trade 21/11 Forecast: World Apple Trade Declines;

Dairy Market. April 2016

Dairy Market Dairy Management Inc. R E P O R T Volume 19 No. 4 April 2016 DMI NMPF Overview Dairy market developments during the first part of April brought slight improvements in the outlook for milk

Dairy Market Dairy Management Inc. R E P O R T Volume 19 No. 4 April 2016 DMI NMPF Overview Dairy market developments during the first part of April brought slight improvements in the outlook for milk

Monthly Economic Letter

Monthly Economic Letter Cotton Market Fundamentals & Price Outlook RECENT PRICE MOVEMENT After some upward movement in April, most benchmark prices turned lower in early May. After climbing to the upper

Monthly Economic Letter Cotton Market Fundamentals & Price Outlook RECENT PRICE MOVEMENT After some upward movement in April, most benchmark prices turned lower in early May. After climbing to the upper

WEEKLY MAIZE REPORT 06 FEBRUARY 2019

WEEKLY MAIZE REPORT 06 FEBRUARY 2019 Unigrain (Pty) Ltd Tel. No. : +27 11 692 4400 Fax. No. : +27 11 412 1183 INTERNATIONAL MARKET Table 1: CME Maize prices and weekly changes (cents/bushel) Currently

WEEKLY MAIZE REPORT 06 FEBRUARY 2019 Unigrain (Pty) Ltd Tel. No. : +27 11 692 4400 Fax. No. : +27 11 412 1183 INTERNATIONAL MARKET Table 1: CME Maize prices and weekly changes (cents/bushel) Currently

Dairy Market. Overview. Commercial Use of Dairy Products

Dairy Market Dairy Management Inc. R E P O R T Volume 19 No. 2 February 2016 DMI NMPF Overview U.S. milk production continues to grow at an annual rate of less than 1 percent, and domestic commercial use

Dairy Market Dairy Management Inc. R E P O R T Volume 19 No. 2 February 2016 DMI NMPF Overview U.S. milk production continues to grow at an annual rate of less than 1 percent, and domestic commercial use

Basis could avoid last fall s disaster Smaller corn crop should free up space for soybeans By Bryce Knorr

Basis could avoid last fall s disaster Smaller corn crop should free up space for soybeans By Bryce Knorr While the futures market has offered only occasional hope this summer, the picture in the cash

Basis could avoid last fall s disaster Smaller corn crop should free up space for soybeans By Bryce Knorr While the futures market has offered only occasional hope this summer, the picture in the cash

Dairy Market. June 2016

Dairy Market Dairy Management Inc. R E P O R T Volume 19 No. 6 June 2016 DMI NMPF Overview U.S. milk production was 1.2 percent higher in April than a year earlier, interrupting the pattern of the three

Dairy Market Dairy Management Inc. R E P O R T Volume 19 No. 6 June 2016 DMI NMPF Overview U.S. milk production was 1.2 percent higher in April than a year earlier, interrupting the pattern of the three

Citrus: World Markets and Trade

United States Department of Agriculture Foreign Agricultural Service Citrus: World Markets and Trade Oranges Global orange production for 2012/13 is forecast to drop over 4 percent from the previous year

United States Department of Agriculture Foreign Agricultural Service Citrus: World Markets and Trade Oranges Global orange production for 2012/13 is forecast to drop over 4 percent from the previous year

Coffee market ends 2016/17 coffee year in deficit for the third consecutive year

Coffee market ends 2016/17 coffee year in deficit for the third consecutive year The ICO composite indicator continued its downward trend that started at the end of August, averaging 124.46 US cents/lb.

Coffee market ends 2016/17 coffee year in deficit for the third consecutive year The ICO composite indicator continued its downward trend that started at the end of August, averaging 124.46 US cents/lb.

World of sugar PAGE 54

World of sugar More than 1 countries produce sugar, about 8% of which is made from sugar cane grown primarily in the tropical and sub-tropical zones of the southern hemisphere, and the balance from sugar

World of sugar More than 1 countries produce sugar, about 8% of which is made from sugar cane grown primarily in the tropical and sub-tropical zones of the southern hemisphere, and the balance from sugar

Cocoa Prepared by Foresight December 5, 2017

Cocoa Prepared by Foresight December 5, 2017 TABLES Cocoa Bean Price Forecast... P. 4 World Cocoa Supply/Demand, Crop Year... P. 7 World Cocoa Production... P. 8 Cocoa Crops in Major Producing Countries...

Cocoa Prepared by Foresight December 5, 2017 TABLES Cocoa Bean Price Forecast... P. 4 World Cocoa Supply/Demand, Crop Year... P. 7 World Cocoa Production... P. 8 Cocoa Crops in Major Producing Countries...

WEEKLY MAIZE REPORT 11 JULY 2018

28 29 21 211 212 213 214 215 216 217 218 WEEKLY MAIZE REPORT 11 JULY 218 Unigrain (Pty) Ltd Tel. No. : +27 11 692 44 Fax. No. : +27 11 412 1183 INTERNATIONAL MARKET Table 1: CME Maize prices and weekly

28 29 21 211 212 213 214 215 216 217 218 WEEKLY MAIZE REPORT 11 JULY 218 Unigrain (Pty) Ltd Tel. No. : +27 11 692 44 Fax. No. : +27 11 412 1183 INTERNATIONAL MARKET Table 1: CME Maize prices and weekly

Asia Loses Its Sweet Tooth for Chocolate

Asia Loses Its Sweet Tooth for Chocolate Rising prices, slower growth have Asian buyers shunning cocoa A Chinese visitor packs chocolates into one of her suitcases in Hong Kong, where demand for the sweet

Asia Loses Its Sweet Tooth for Chocolate Rising prices, slower growth have Asian buyers shunning cocoa A Chinese visitor packs chocolates into one of her suitcases in Hong Kong, where demand for the sweet

Downward correction in coffee market as supply prospects improve

Downward correction in coffee market as supply prospects improve The recent rally in coffee prices underwent a notable reversal in November 2016, attributed to improved weather prospects in Brazil and

Downward correction in coffee market as supply prospects improve The recent rally in coffee prices underwent a notable reversal in November 2016, attributed to improved weather prospects in Brazil and

Dairy Market R E P O R T

Volume 18 No. 8 Dairy Market R E P O R T August 2015 DMI NMPF Overview Milk prices in many major milk-producing countries have plummeted to levels that are producing severe financial stress for their farmers.

Volume 18 No. 8 Dairy Market R E P O R T August 2015 DMI NMPF Overview Milk prices in many major milk-producing countries have plummeted to levels that are producing severe financial stress for their farmers.

SPRING WHEAT FUTURES AND OPTIONS

SPRING WHEAT FUTURES AND OPTIONS W hether it s a farmer near Minot, a trader in Minneapolis or a there is only one place to look when it comes to hard red spring WORLD S LARGEST SPRING WHEAT MARKET Since

SPRING WHEAT FUTURES AND OPTIONS W hether it s a farmer near Minot, a trader in Minneapolis or a there is only one place to look when it comes to hard red spring WORLD S LARGEST SPRING WHEAT MARKET Since

MONTHLY COFFEE MARKET REPORT

E MONTHLY COFFEE MARKET REPORT May 2014 After five consecutive months of rising prices, the coffee market reversed lower in May. From a high of 179 cents/lb in April, the daily price of the ICO composite

E MONTHLY COFFEE MARKET REPORT May 2014 After five consecutive months of rising prices, the coffee market reversed lower in May. From a high of 179 cents/lb in April, the daily price of the ICO composite

Monthly Economic Letter U.S. and Global Market Fundamentals

Monthly Economic Letter U.S. and Global Market Fundamentals August 2012 www.cottoninc.com After trading within relatively narrow bands throughout July, New York futures moved higher in early August, with

Monthly Economic Letter U.S. and Global Market Fundamentals August 2012 www.cottoninc.com After trading within relatively narrow bands throughout July, New York futures moved higher in early August, with

Dairy Market R E P O R T

Volume 18 No. 12 Dairy Market R E P O R T D e c e m b e r 2 0 1 5 DMI NMPF Overview The U.S. average all-milk price, which spent seven months of 2015 hovering around $16.70 per hundredweight, has moved

Volume 18 No. 12 Dairy Market R E P O R T D e c e m b e r 2 0 1 5 DMI NMPF Overview The U.S. average all-milk price, which spent seven months of 2015 hovering around $16.70 per hundredweight, has moved

Dairy Outlook. December By Jim Dunn Professor of Agricultural Economics, Penn State University. Market Psychology

Dairy Outlook December 2015 By Jim Dunn Professor of Agricultural Economics, Penn State University Market Psychology The Class III market has taken a beating lately as cheese prices have drifted down and

Dairy Outlook December 2015 By Jim Dunn Professor of Agricultural Economics, Penn State University Market Psychology The Class III market has taken a beating lately as cheese prices have drifted down and

Coffee market ends 2015/16 in deficit for the second consecutive year

Coffee market ends 2015/16 in deficit for the second consecutive year The coffee market settled up by 5.5% in September, mostly driven by a steady increase in Robusta prices supported by concerns over

Coffee market ends 2015/16 in deficit for the second consecutive year The coffee market settled up by 5.5% in September, mostly driven by a steady increase in Robusta prices supported by concerns over

Prices for all coffee groups increased in May

Prices for all coffee groups increased in May In May 2018, the ICO composite indicator increased by 0.7% to an average of 113.34 US cents/lb, following three months of declines. Prices for all coffee groups

Prices for all coffee groups increased in May In May 2018, the ICO composite indicator increased by 0.7% to an average of 113.34 US cents/lb, following three months of declines. Prices for all coffee groups

Record Exports for Coffee Year 2016/17

Record Exports for Coffee Year 2016/17 Total exports in September 2017 reached 8.34 million bags, compared to 9.8 million in September 2016. While coffee year 2016/17 registered a decrease in its final

Record Exports for Coffee Year 2016/17 Total exports in September 2017 reached 8.34 million bags, compared to 9.8 million in September 2016. While coffee year 2016/17 registered a decrease in its final

July marks another month of continuous low prices

July marks another month of continuous low prices In July 2018, the ICO composite indicator price decreased by 2.9% to an average of 107.20 US cents/lb, which is the lowest monthly average for July since

July marks another month of continuous low prices In July 2018, the ICO composite indicator price decreased by 2.9% to an average of 107.20 US cents/lb, which is the lowest monthly average for July since

Commodity: TURMERIC (May) S2 S1 Pivot R1 R2

S2 S1 Pivot R1 R2") Commodity: TURMERIC (May) S2 S1 Pivot R1 R2 5714 5938 6224 6448 6734 Fundamentals Turmeric futures (May) is expected to remain stuck in the range of 6200-6545 levels. In days to come, we may see fewer

Commodity: TURMERIC (May) S2 S1 Pivot R1 R2 5714 5938 6224 6448 6734 Fundamentals Turmeric futures (May) is expected to remain stuck in the range of 6200-6545 levels. In days to come, we may see fewer

Coffee market ends 2017/18 in surplus

Coffee market ends 217/18 in surplus World coffee production in coffee year 217/18 is estimated 5.7% higher at 164.81 million bags as output of Arabica increased by 2.2% to 11.82, and Robusta grew 11.7%

Coffee market ends 217/18 in surplus World coffee production in coffee year 217/18 is estimated 5.7% higher at 164.81 million bags as output of Arabica increased by 2.2% to 11.82, and Robusta grew 11.7%

2018/19 expected to be the second year of surplus

2018/19 expected to be the second year of surplus Coffee year 2018/19 is expected to be the second consecutive season of surplus, as global output, estimated at 167.47 million bags, exceeds world consumption,

2018/19 expected to be the second year of surplus Coffee year 2018/19 is expected to be the second consecutive season of surplus, as global output, estimated at 167.47 million bags, exceeds world consumption,

World Scenario: Oilseed Production

World Scenario: Oilseed Production Commodity 13/14 (Million Ton) 16/17 (Million Ton) Soybean 280.3 352 Sunflower seed 43.6 48.22 Rapeseed 69.6 63.13 Cotton Seed 44.4 39.52 Groundnuts 28.4 30.32 Palm-kernal

World Scenario: Oilseed Production Commodity 13/14 (Million Ton) 16/17 (Million Ton) Soybean 280.3 352 Sunflower seed 43.6 48.22 Rapeseed 69.6 63.13 Cotton Seed 44.4 39.52 Groundnuts 28.4 30.32 Palm-kernal

Dairy Market. October 2016

Dairy Market Dairy Management Inc. R E P O R T Volume 19 No. 10 October 2016 DMI NMPF Overview Milk prices continued a generally solid recovery from their late-spring low through August, when the U.S.

Dairy Market Dairy Management Inc. R E P O R T Volume 19 No. 10 October 2016 DMI NMPF Overview Milk prices continued a generally solid recovery from their late-spring low through August, when the U.S.

For personal use only

SEPTEMBER 216 GLOBAL DAIRY UPDATE European milk production has decreased for the first time since early 215, with volumes in June down 2 compared to last year. Last week we announced our annual results,

SEPTEMBER 216 GLOBAL DAIRY UPDATE European milk production has decreased for the first time since early 215, with volumes in June down 2 compared to last year. Last week we announced our annual results,

Fresh Deciduous Fruit (Apples, Grapes, & Pears): World Markets and Trade

: World Markets and Trade") Fresh Deciduous Fruit (Apples, Grapes, & Pears): World Markets and Trade June 21 APPLES Record Production but Trade Estimate Revised Downward The world production estimate for 29/1 is virtually unchanged

Fresh Deciduous Fruit (Apples, Grapes, & Pears): World Markets and Trade June 21 APPLES Record Production but Trade Estimate Revised Downward The world production estimate for 29/1 is virtually unchanged

Monitoring EU Agri-Food Trade: Development until June 2017

Monitoring EU Agri-Food Trade: Development until June 2017 June 2017: Agri-food exports again above previous years level After a rebound in May, the monthly value of EU agri-food exports went down to EUR

Monitoring EU Agri-Food Trade: Development until June 2017 June 2017: Agri-food exports again above previous years level After a rebound in May, the monthly value of EU agri-food exports went down to EUR

Milk and Milk Products. Price and Trade Update. Weekly Newsletter. Milk and Milk Products. Price and Trade Update: April

April Milk and Milk Products Price and Trade Update Weekly Newsletter Milk and Milk Products Price and Trade Update: April 1 PRICES: Remain depressed International dairy product prices began the year at

April Milk and Milk Products Price and Trade Update Weekly Newsletter Milk and Milk Products Price and Trade Update: April 1 PRICES: Remain depressed International dairy product prices began the year at

Becoming a Smarter Trader: The Market Impact of the Structure in the Sugar, Coffee, and OJ Markets

Becoming a Smarter Trader: The Market Impact of the Structure in the Sugar, Coffee, and OJ Markets Judith Ganes March 12 th, 2014 Increasing Reliance on a Few Suppliers for Global Needs Efficiency gains

Becoming a Smarter Trader: The Market Impact of the Structure in the Sugar, Coffee, and OJ Markets Judith Ganes March 12 th, 2014 Increasing Reliance on a Few Suppliers for Global Needs Efficiency gains

Dairy Market R E P O R T

Volume 17 No. 5 Dairy Market R E P O R T May 2014 DMI NMPF Overview Many key milk and dairy product prices continued to set records in April. And while the dairy futures markets indicate that prices will

Volume 17 No. 5 Dairy Market R E P O R T May 2014 DMI NMPF Overview Many key milk and dairy product prices continued to set records in April. And while the dairy futures markets indicate that prices will

MONTHLY COFFEE MARKET REPORT

E MONTHLY COFFEE MARKET REPORT February 2014 February 2014 has seen significant developments in the coffee market, with prices shooting upwards at a startling rate. The ICO composite daily price has increased

E MONTHLY COFFEE MARKET REPORT February 2014 February 2014 has seen significant developments in the coffee market, with prices shooting upwards at a startling rate. The ICO composite daily price has increased

Dairy Market. May 2017

Dairy Market Dairy Management Inc. R E P O R T Volume 20 No. 4 May 2017 DMI NMPF Overview The rate of milk production growth began to moderate during the first quarter, but additional milk production continues

Dairy Market Dairy Management Inc. R E P O R T Volume 20 No. 4 May 2017 DMI NMPF Overview The rate of milk production growth began to moderate during the first quarter, but additional milk production continues

Coffee prices rose slightly in January 2019

Coffee prices rose slightly in January 2019 In January 2019, the ICO composite indicator rose by 0.9% to 101.56 US cents/lb as prices for all group indicators increased. After starting at a low of 99.16

Coffee prices rose slightly in January 2019 In January 2019, the ICO composite indicator rose by 0.9% to 101.56 US cents/lb as prices for all group indicators increased. After starting at a low of 99.16

Dairy Market. Overview. Commercial Use of Dairy Products. U.S. Dairy Trade

Dairy Market Dairy Management Inc. R E P O R T Volume 21 No. 7 July 2018 DMI NMPF Overview Fallout from the developing tariff conflict between the United States and some of its major trading partners has

Dairy Market Dairy Management Inc. R E P O R T Volume 21 No. 7 July 2018 DMI NMPF Overview Fallout from the developing tariff conflict between the United States and some of its major trading partners has

Dairy Market. Overview. Commercial Use of Dairy Products. U.S. Dairy Trade

Dairy Market Dairy Management Inc. R E P O R T Volume 21 No. 5 May 2018 DMI NMPF Overview Many of the key dairy market statistics reported for March and April indicated that milk prices for U.S. dairy

Dairy Market Dairy Management Inc. R E P O R T Volume 21 No. 5 May 2018 DMI NMPF Overview Many of the key dairy market statistics reported for March and April indicated that milk prices for U.S. dairy

Brazil Milk Cow Numbers and Milk Production per Cow,

TABLE OF CONTENTS 1. Brazil 1.1. Brazil Milk Market Introduction 1.1.1. Brazil Cow Milk Market Production and Fluid Milk Consumption by Volume, 1.1.2. Brazil Milk Cow Numbers and Milk Production per Cow,

TABLE OF CONTENTS 1. Brazil 1.1. Brazil Milk Market Introduction 1.1.1. Brazil Cow Milk Market Production and Fluid Milk Consumption by Volume, 1.1.2. Brazil Milk Cow Numbers and Milk Production per Cow,

Ecobank s pan-african footprint. Africa-Asia trade flows

Ecobank s pan-african footprint Africa-Asia trade flows Ghana, Côte d Ivoire and Nigeria: The changing face of West African cocoa Dr Edward George Head of Group Research, Ecobank Lagos, February 3rd 2016

Ecobank s pan-african footprint Africa-Asia trade flows Ghana, Côte d Ivoire and Nigeria: The changing face of West African cocoa Dr Edward George Head of Group Research, Ecobank Lagos, February 3rd 2016

Acreage Forecast

World (John Sandbakken and Larry Kleingartner) The sunflower is native to North America but commercialization of the plant took place in Russia. Sunflower oil is the preferred oil in most of Europe, Mexico

World (John Sandbakken and Larry Kleingartner) The sunflower is native to North America but commercialization of the plant took place in Russia. Sunflower oil is the preferred oil in most of Europe, Mexico

MONTHLY COFFEE MARKET REPORT

1 E MONTHLY COFFEE MARKET REPORT March 2014 Ongoing uncertainty over the Brazilian coffee crop has caused significant fluctuations in coffee prices during March, with monthly volatility of the International

1 E MONTHLY COFFEE MARKET REPORT March 2014 Ongoing uncertainty over the Brazilian coffee crop has caused significant fluctuations in coffee prices during March, with monthly volatility of the International

Rick Alexander

ralexander@zaner.com NOT SEEING SHARP DROPS LATELY IN THE WHEAT COMPLEX. EXPORTS SLIGHTLY AHEAD OF 5 YEAR AVE. Posted on 8/17/2016 7:15:52 AM WE HAVE A VERY GOOD HEDGING DEPARTMENT HEADED BY TED SEIFRIED.

ralexander@zaner.com NOT SEEING SHARP DROPS LATELY IN THE WHEAT COMPLEX. EXPORTS SLIGHTLY AHEAD OF 5 YEAR AVE. Posted on 8/17/2016 7:15:52 AM WE HAVE A VERY GOOD HEDGING DEPARTMENT HEADED BY TED SEIFRIED.

POC 2018 PALM & LAURIC OILS PRICE OUTLOOK CONFERENCE & EXHIBITION. Emerging Trends In The Edible Oil Sector A View From Pakistan..

POC 2018 PALM & LAURIC OILS PRICE OUTLOOK CONFERENCE & EXHIBITION 5-7 March, 2018 Hotel Shangri-La, Kuala Lumpur Emerging Trends In The Edible Oil Sector A View From Pakistan.. By Abdul Rasheed Janmohammed

POC 2018 PALM & LAURIC OILS PRICE OUTLOOK CONFERENCE & EXHIBITION 5-7 March, 2018 Hotel Shangri-La, Kuala Lumpur Emerging Trends In The Edible Oil Sector A View From Pakistan.. By Abdul Rasheed Janmohammed

Gordon Food Service Market Updates for January 4, 2019

Gordon Food Service Market Updates for January 4, 2019 Dairy Cheese The Block and Barrel Markets have continued to be bearish. Speculators feel this will continue with the current environment trades are

Gordon Food Service Market Updates for January 4, 2019 Dairy Cheese The Block and Barrel Markets have continued to be bearish. Speculators feel this will continue with the current environment trades are

Commitment of. Traders. Managed Money. Fund Positions

October 5, 2018 Market Summary The USDA will issue its October Supply and Demand report this next Thursday and will incorporate updated ending stocks data from last weeks report. Additionally, they will

October 5, 2018 Market Summary The USDA will issue its October Supply and Demand report this next Thursday and will incorporate updated ending stocks data from last weeks report. Additionally, they will

MGEX Spring Wheat 2013

MGEX Spring Wheat 213 The Minneapolis Grain Exchange, Inc. (MGEX) has been the principal market for hard red spring (HRS) wheat since 1881, offering futures and options contracts based on this unique commodity.

MGEX Spring Wheat 213 The Minneapolis Grain Exchange, Inc. (MGEX) has been the principal market for hard red spring (HRS) wheat since 1881, offering futures and options contracts based on this unique commodity.

Fresh Deciduous Fruit (Apples, Grapes, & Pears): World Markets and Trade

: World Markets and Trade") United States Department of Agriculture Foreign Agricultural Service Fresh Deciduous Fruit (Apples, Grapes, & Pears): World Markets and Trade 9 1, MT Deciduous Fruit on Seasonal Cycles 6 Northern Hemisphere

United States Department of Agriculture Foreign Agricultural Service Fresh Deciduous Fruit (Apples, Grapes, & Pears): World Markets and Trade 9 1, MT Deciduous Fruit on Seasonal Cycles 6 Northern Hemisphere

Monitoring EU Agri-Food Trade: Development until January 2018

Monitoring EU Agri-Food Trade: Development until January 2018 January 2018: good start of a year for EU agri-food exports The value of EU agri-food exports in January 2018 kept its very high level, now

Monitoring EU Agri-Food Trade: Development until January 2018 January 2018: good start of a year for EU agri-food exports The value of EU agri-food exports in January 2018 kept its very high level, now

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S.

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Voluntary - Public Date: 4/24/2013 GAIN Report Number:

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Voluntary - Public Date: 4/24/2013 GAIN Report Number:

Dairy Market. November 2017

Dairy Market Dairy Management Inc. R E P O R T Volume 20 No. 10 November 2017 DMI NMPF Overview U.S. Cheddar cheese prices hit a 10-month high in October, while butter prices softened but remained well

Dairy Market Dairy Management Inc. R E P O R T Volume 20 No. 10 November 2017 DMI NMPF Overview U.S. Cheddar cheese prices hit a 10-month high in October, while butter prices softened but remained well

MONTHLY REPORTS EDIBLE OIL JUNE - JULY 2016

MONTHLY REPORTS EDIBLE OIL Monthly Prices Movement Edible Oil prices remained volatile in June month tracking movement in Indian Rupee and uncertain fundamentals. Soy Oil prices remained mixed with more

MONTHLY REPORTS EDIBLE OIL Monthly Prices Movement Edible Oil prices remained volatile in June month tracking movement in Indian Rupee and uncertain fundamentals. Soy Oil prices remained mixed with more

MONTHLY REPORTS PULSES JUNE - JULY 2016

MONTHLY REPORTS PULSES Monthly Prices Movement Pulses prices overall remained firm throughout the month amid expectation of lower output, delayed Monsoon despite strict government measures to control price

MONTHLY REPORTS PULSES Monthly Prices Movement Pulses prices overall remained firm throughout the month amid expectation of lower output, delayed Monsoon despite strict government measures to control price

In this week we enlighten you about peanuts from the USA, Argentina and China.

Dear client, In this week we enlighten you about peanuts from the USA, Argentina and China. USA From the USA there is still a stock of about 950,000 metric farmer tons left from the 2013 crop. Though this

Dear client, In this week we enlighten you about peanuts from the USA, Argentina and China. USA From the USA there is still a stock of about 950,000 metric farmer tons left from the 2013 crop. Though this

Monitoring EU Agri-Food Trade: Development until April 2017

Monitoring EU Agri-Food Trade: Development until April 2017 April 2017: Agri-food exports back to average values The monthly value of EU agri-food exports in April 2017 reached a value of EUR 10.6 billion,

Monitoring EU Agri-Food Trade: Development until April 2017 April 2017: Agri-food exports back to average values The monthly value of EU agri-food exports in April 2017 reached a value of EUR 10.6 billion,

Commodity Market Monthly

Commodity Market Monthly Research Department, Commodities Unit June 1, 216 www.imf.org/commodities commodities@imf.org Commodity prices surged 6. percent in May, extending gains for fourth consecutive

Commodity Market Monthly Research Department, Commodities Unit June 1, 216 www.imf.org/commodities commodities@imf.org Commodity prices surged 6. percent in May, extending gains for fourth consecutive

Commitment of. Traders. Managed Money. Fund Positions

October 19, 2018 Market Summary Corn started the week off strong, closing Monday up 4 cents at $3.77 1/4, which marked the highest close since August 20th. Nov soybeans also managed their highest daily

October 19, 2018 Market Summary Corn started the week off strong, closing Monday up 4 cents at $3.77 1/4, which marked the highest close since August 20th. Nov soybeans also managed their highest daily

Downward correction as funds respond to increasingly positive supply outlook

Downward correction as funds respond to increasingly positive supply outlook Coffee prices fell sharply at the end of April as institutional investors sold off their positions. The coffee market continues

Downward correction as funds respond to increasingly positive supply outlook Coffee prices fell sharply at the end of April as institutional investors sold off their positions. The coffee market continues

Vegetable Imports Approaching 20% of Total

Vegetable Imports Approaching 20% of Total Domestic Supply The taste of imported vegetables has become more familiar to the palates of Japanese consumers in recent years. According to the Ministry of Finance,

Vegetable Imports Approaching 20% of Total Domestic Supply The taste of imported vegetables has become more familiar to the palates of Japanese consumers in recent years. According to the Ministry of Finance,

Dairy Market. Overview. Commercial Use of Dairy Products. U.S. Dairy Trade

Dairy Market Dairy Management Inc. R E P O R T Volume 19 No. 11 November 2016 DMI NMPF Overview Four straight months of rising milk prices and three straight months of falling feed costs have brought some

Dairy Market Dairy Management Inc. R E P O R T Volume 19 No. 11 November 2016 DMI NMPF Overview Four straight months of rising milk prices and three straight months of falling feed costs have brought some

GLOBOIL INTERNATIONAL Emerging Trends In The Edible Oil Sector A View From Pakistan.. Abdul Rasheed Janmohammed

GLOBOIL INTERNATIONAL 2018 27-29 April, 2018 Hotel JW Marriott Marquis, Dubai, U.A.E. Emerging Trends In The Edible Oil Sector A View From Pakistan.. By Abdul Rasheed Janmohammed Chief Executive Chief

GLOBOIL INTERNATIONAL 2018 27-29 April, 2018 Hotel JW Marriott Marquis, Dubai, U.A.E. Emerging Trends In The Edible Oil Sector A View From Pakistan.. By Abdul Rasheed Janmohammed Chief Executive Chief

Daily Soft Markets Commentary Thursday February 22, 2018

Daily Soft Markets Commentary Thursday February 22, 2018 DAILY COCOA COMMENTARY Steady uptrend on firm demand and some supply uncertainties Cocoa has been able to extend its current upmove to the highest

Daily Soft Markets Commentary Thursday February 22, 2018 DAILY COCOA COMMENTARY Steady uptrend on firm demand and some supply uncertainties Cocoa has been able to extend its current upmove to the highest

Record exports in coffee year 2017/18

Record exports in coffee year 2017/18 Total coffee exports increased each year since 2010/11 with a new record reached in 2017/18 at 121.86 million bags, 2% higher than 2016/17. In the twelve months ending

Record exports in coffee year 2017/18 Total coffee exports increased each year since 2010/11 with a new record reached in 2017/18 at 121.86 million bags, 2% higher than 2016/17. In the twelve months ending

Coffee market recovers slightly from December slump

Coffee market recovers slightly from December slump After reaching its lowest level in 22 months in December 2017, the monthly average of the ICO composite indicator price increased by 1.4% to 115.60 US

Coffee market recovers slightly from December slump After reaching its lowest level in 22 months in December 2017, the monthly average of the ICO composite indicator price increased by 1.4% to 115.60 US

Monthly Economic Letter

Monthly Economic Letter Cotton Market Fundamentals & Price Outlook RECENT PRICE MOVEMENT NY futures and the A Index decreased throughout December before stabilizing in January. Chinese and Pakistani prices

Monthly Economic Letter Cotton Market Fundamentals & Price Outlook RECENT PRICE MOVEMENT NY futures and the A Index decreased throughout December before stabilizing in January. Chinese and Pakistani prices

QUARTERLY REVIEW OF THE PERFORMANCE OF THE DAIRY INDUSTRY 1

QUARTERLY REVIEW OF THE PERFORMANCE OF THE DAIRY INDUSTRY 1 The information in this document is from sources deemed to be correct. Milk SA, the MPO and SAMPRO are not responsible for the results of any

QUARTERLY REVIEW OF THE PERFORMANCE OF THE DAIRY INDUSTRY 1 The information in this document is from sources deemed to be correct. Milk SA, the MPO and SAMPRO are not responsible for the results of any

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S.

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Required Report - public distribution Date: GAIN Report

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Required Report - public distribution Date: GAIN Report

Outlook for FCOJ in 2019/20

December 2018 Outlook for FCOJ in 2019/20 The Orange Juice Market Moves Towards Balance RaboResearch Food & Agribusiness far.rabobank.com Andrés Padilla Senior Analyst Beverages +55 11 5503 7000 Contents

December 2018 Outlook for FCOJ in 2019/20 The Orange Juice Market Moves Towards Balance RaboResearch Food & Agribusiness far.rabobank.com Andrés Padilla Senior Analyst Beverages +55 11 5503 7000 Contents