Spatial and Temporal Maize Price Analysis in East Africa

|

|

|

- Owen Casey

- 5 years ago

- Views:

Transcription

1 Spatial and Temporal Maize Price Analysis in East Africa Sika Gbegbelegbe and Hugo de Groote Socioeconomics Program, CIMMYT, Nairobi, Kenya Selected Poster prepared for presentation at the International Association of Agricultural Economists (IAAE) Triennial Conference, Foz do Iguaçu, Brazil, August, Copyright 2012 by Gbegbelegbe S. and de Groote H.. All rights reserved. Readers may make verbatim copies of this document for non commercial purposes by any means, provided that this copyright notice appears on all such copies.

2 Abstract Maize is the major food crop and an important cash crop in East Africa, but yields have not increased in the last years. Maize prices fluctuate heavily both over time, causing price insecurity which hampers investment decisions, and over space which, combined with limited knowledge of that fluctuation, reduces opportunities to market surplus. In this paper, temporal and spatial price volatility is analyzed, based on monthly maize prices from various markets in East Africa, including 28 markets in Kenya. The hypothesis that the market liberalization of the 1990s increased efficiency and decreased volatility in Kenya is also tested. Preliminary results for Kenyan markets show a clear negative trend, indicating that real maize prices have decreased over time, on average 4% per year. Major factors in price variation are the differences between years, although a distinct one-season effect is demonstrated. Prices are clearly higher in the surplus zone during the high season, but lower otherwise. The coast has higher prices in the lower season. Generally, it can be concluded that price volatility has been decreasing over the years. The liberalization, most likely, has played a positive effect on this trend. Key words: Market liberalization, maize, price variation, spatial analysis

3 Spatial and temporal maize price volatility in East Africa 1. Introduction African agriculture improved dramatically in the 1960s and 1970s, due to strong public investment in research and extension, combined with market interventions such as guaranteed prices and subsidized inputs and credit (Stringer and Pingali, 2004). However, these interventions also had their limitations: government institutions often are not very efficient, and their interventions tend to be expensive and also tend to reduce the involvement of the private sector. Over time, government intervention in agricultural markets began to be seen as a major problem (Crawford et al., 2003). As a reaction, and strongly encouraged by the donor community, many countries adopted Structural Adjustment Plans (SAPs), starting in the 1980s. These SAPs focused on creating a conducive environment for private sector involvement, by liberalizing markets for agricultural inputs and outputs, letting market forces determine the prices of these products, and reduce government s role (Gisselquist and Grether, 2000; Gisselquist et al., 2002). The Kenyan government, faced with tight budgets and pressure from donors liberalized the maize marketing, lifting trade and transport controls, reducing the interventions of the marketing board, and liberalizing prices (Wangia et al., 2004). Other countries in there region, namely Uganda and Ethiopia, followed a strategy similar to that of Kenya by implementing SAPs. Unfortunately, the liberalization of the agricultural sector in SSA did little to increase productivity. A synthesis of relevant research finds a consensus that economic performance of the region has lagged behind that of developing countries in other regions

4 and that the reforms have fallen short of their expected outcomes (Kherallah et al., 2002). Often, reforms studied were only partially implemented and reversal was common. Others argue that, while liberalization is necessary to accelerate productivity, it is not sufficient. Proper distribution systems need to be in place, appropriate and efficient regulatory and legal frameworks need to be in place, and infrastructure, especially for transport infrastructure, is needed to decrease the transaction costs (Tripp, 2001; Tripp and Rohrbach, 2001). Informal discussions in the different agro-ecological zones in Kenya revealed that farmers complain that price volatility is a major problem (De Groote et al., 2004). Maize is their most important food crop, and also an important cash crop. But prices fluctuate heavily over time, so farmers face price insecurity that hampers investment decisions, and over space, although they have little knowledge on the latter to guide them to market their surplus. Therefore, in this paper, the temporal and spatial price volatility is analyzed in various markets in Kenya, Uganda and Ethiopia; the hypothesis that the liberalization increased market efficiency and decreased volatility in Kenya is also tested. 2. Methodology 2.1. Conceptual framework Before the liberalization, African governments generally maintained tight price and movement controls in the maize market. It was expected that the release of those controls could increase price volatility, at least in the short run. Over time, however, markets are expected to become more efficient, reducing the temporal volatility. Similarly, most African governments, used to have fixed and pan-territorial prices for

5 major staples. The liberalization was expected to bring price corrections, reflecting cost of production and trade. When markets become more efficient, however, these prices are expected to stabilize. Many factors, other than the policy environment, influence prices. Some of the main factors include changes in supply brought by climatic conditions, changes in imports, food aid and governmental interventions in the market The models The standard procedure to analyze the temporal price variability is to regress the corrected price on a time indicator. Mathematically: P = α + βt + ε it it where P it is the adjusted maize price in location i at time t in consecutive months (January 1, 1994 = 1). Since these price data are panel data, or combined cross-sectional and time series data, the appropriate model needs to correct for autocorrelation of the error terms over time and space by including dummies for both (Greene, 1991). For time, a combination of the trend and dummies for the months is used, and for space dummies for the markets. The model becomes: it = i + i m P α μ + βt + ε m it Where α i is the coefficient for the binary variable of market I, and μ m is the coefficient for the binary variable for month m. For this second regression, only those markets with few missing values were selected. Autocorrelation was tested using the Durban-Watson test. Seasonal variation was analyzed by comparing the coefficients of the monthly binary variables.

6 Spatial price variation was analyzed using the framework proposed by Rapsomanikis, Hallam and Conforti (2004) which involves the following steps (Figure 1): 1. Assess the order of integration of market price: If tests results suggest different integration orders across the price series, there is no integration and Granger causality tests are performed If results suggest I(0), estimate ADL and perform GC tests If results suggests series are integrated of order k, I(k), proceed to step 2 2. Apply Johansen or Engle and Granger procedures to test co integration: If results suggests no co-integration, estimate ADL and perform GC tests If results suggests co-integration, perform GC tests and move to step 3 3. Estimate VECM: assess speed of adjustment and test for long run Granger causality; then, move to step 4 4. Estimate AECM: test for asymmetric price response and transmission [FIGURE 1] This analysis should be considered as preliminary. Formal tests for market integration would use more sophisticated models that include lagged prices and other factors that influence prices, including rainfall and production in the region, such as the Ravallion/Timmer model (Fackler and Goodwin, 2001). Ideally, the model should include quantities marketed and transport costs, data that are unfortunately not yet available.

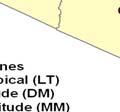

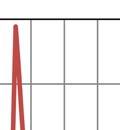

7 2.3. Data For the analysis on Kenyan markets, we used monthly maize prices collected by the Ministry of Agriculture, in 28 markets (although not consistently in the same markets every year), from January 1990 to December 2010 (150 months) (Figure 2). Maize prices for markets in Uganda and Ethiopia are from the Uganda Bureau of Statistics (UBOS) and the Central Statistical Office in Ethiopia, respectively. [FIGURE 2] To correct for inflation, nominal prices in Kenya, were multiplied by the Consumer Price Index (CPI), which is produced annually by the Central Bureau of Statistics (CBS). The annual CPI was converted into a monthly CPI using a linear approximation. 3. Preliminary Results Here, we discuss preliminary results for Kenya. Some additional analysis will also be done for maize markets in Uganda and Ethiopia Evolution of prices over time (temporal variation) Plotting the monthly maize prices over time clearly shows how the nominal price of maize has increased slowly over the years (Figure 3). The average price of maize was 1167 Kenya shillings (KSh) for a standard 90 kg bag, or 12.0 KSh/kg. Over the same period of 150 months, however, the CPI increased sharply, more than doubling in value.

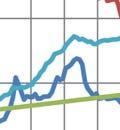

8 As a result, the maize price in constant prices (2009 KShs/kg) decreased substantially. The trend, obtained by KShs/month (Table 1), is about almost half a shilling per year for nominal prices and about 1 shilling per year for the real prices. [FIGURE 3] [TABLE 1] Correcting for the trend, the major source of variation is clearly between the different years, especially in the beginning. Maize prices in 1994 and 1997 are substantially above the trend, while 1995, 1996, 1998 and 2002 are substantially below. After the variation between years, there is also a clear seasonal pattern. Including binary variables for the major markets and monthly binary variables for February till December (keeping January as a base), results in significant price differences from May to August (Table 2). This reflects the supply of the major rainy season, from April to August. [TABLE 2] This seasonal variation is better understood when compared to the month with the lowest prices, October, and plotting the monthly price differences (Figure 4). A strong seasonal trend is clearly visible, although basically with only one season. Prices are lowest in November, shortly after the harvest. They rise slowly from November till April, followed by another sharp price increase in May. Price stays high in June and July, but

9 drop quickly over August and September. The short rainy season (October to December) does not seem to have much impact on prices, other than a small increase in December. [FIGURE 4] 3.2. Price differences between markets (spatial variation) Kenyan maize markets versus international maize markets Maize prices in Nairobi, Mombasa, and selected international markets are integrated of order one (Table 3). However, the maize price series in Nairobi does not seem to be co-integrated with the price of white maize in SAFEX or with the price of maize US no 2, from the US Gulf (Table 3). These results suggest no integration between maize markets in Nairobi and in international markets. Some additional Granger causality tests and the estimation of the ADL model indicate some Granger causality from Nairobian markets to SAFEX with lags 9 and 11 (Table 3). Such results imply that shocks to maize prices in Nairobi are passed through to maize prices in SAFEX some months later; however, the effects of these shocks are not strong enough to drive maize prices in SAFEX. The results also imply no relationship between maize prices in Nairobi and the price of maize US no 2 (Table 3). Maize markets in Mombasa are also not integrated with international maize markets (Table 3). However, the results suggest some Granger causality from Mombasa to Safex with a lag of 4 months: this means that shocks to maize prices in Mombasa are passed through, albeit not strongly to maize prices in SAFEX, about 4 months later. The results

10 also imply that the price of maize US no 2 Granger-causes maize prices in Mombasa for lags [TABLE 3] Market Integration between maize markets in Kenya Maize prices in all markets under study are integrated of order one: augmented Dickey-Fuller and Philips Perron tests with and without drift indicate that the price series are non-stationary in their levels but they are stationary in their first-difference (Table 4). The Engle and Granger procedure also indicated that all maize markets under study were co-integrated of degree CI(1,1) on a pairwise basis, except for Eldoret and Nairobi. The Granger causality tests were performed for the co-integrated price series (Table 4). The results related to maize markets in Nairobi relative to other markets in Kenya implied Granger causality in at least one direction. The estimation of the Vector Error Correction Models (VECM) implied that maize prices in Mombasa take about 1.7 months to fully adjust to the maize price changes in Nairobi: the coefficient of the error correction term is 0.6 and is significant at the 5% threshold level. The estimated coefficients in the VECM also imply that maize prices in Mombasa are affected by the maize price shocks that occurred 5 months earlier in Nairobi. However, the test of long-run Granger causality also indicates a bilateral Granger causality between maize prices in Nairobi and Mombasa: in the long-run, maize prices in Nairobi and Mombasa affect each other.

11 The results also indicate full price transmission between maize markets in Nairobi and Nakuru, with prices in Nakuru being affected by prices in Nairobi in the short term (Table 4). Long-run Granger causality test also indicate that maize prices in Nairobi Granger-cause maize prices in Nakuru and not vice versa. These results imply that maize prices in Nakuru strongly depend on maize prices in Nairobi. A similar conclusion applies for maize markets in Nairobi and Kisumu; however, in this case, maize prices in Nairobi strongly depend on maize prices in Kisumu. The Granger causality tests implied unilateral Granger causality between maize prices in Mombasa and each of the other Kenyan markets (Table 4). The results related to estimating the VECM for maize prices in Mombasa and Nakuru suggest a slow adjustment to the long-run relationship between maize prices in the two markets: the coefficient of the error correction term is insignificant. Moreover, maize prices in Mombasa are affected by maize price shocks that occur in Nakuru 9 months earlier. However, long-run Granger causality tests imply that maize prices in Mombasa and Nakuru affect each other in the long run. A similar conclusion applies to maize prices in Mombasa and Eldoret (Table 4). The econometric results imply that maize prices in Mombasa are affected by maize prices in Eldoret with a lag of 1, 2 and 7 months. However, maize prices in the two towns Granger-cause each other in the long run.

12 The Granger causality tests on maize prices in Mombasa and Kisumu showed no Granger causality, even if the series were co-integrated of degree CI(1,1) (Table 4). In addition, the results related to estimating the VECM for these two price series indicated no relationship between the price series. The results implying co-integration between the two prices series might stem from the fact that maize markets in Kisumu affect the ones in Nairobi while maize markets in Nairobi affect the ones in Mombasa, as shown in the earlier results. The Granger causality tests on the relationship between maize prices in Nakuru and each of Eldoret and Kisumu suggested bilateral or unilateral Granger causality (Table 4). The estimation results related to the VECM linking maize prices in Nakuru and Eldoret indicate a slow adjustment to the long-run equilibrium between maize prices in the two markets. In the short- and medium-term, maize prices in Nakuru affect maize prices in Eldoret. However, in the long-run, the two price series Granger-cause each other. A similar conclusion applies the maize prices in Nakuru and Kisumu. Maize prices in Nakuru affect maize prices in Kisumu in the short- to medium-term. However, the two price series affect one another in the long-run. The Granger causality tests between Eldoret and Kisumu implied a bilateral Granger causality (Table 4). However, the estimation of the VECM for the two price series indicated that there is no relationship between the two price series. Maize markets in Nakuru are integrated with maize in each of Eldoret and Kisumu, as explained earlier. Hence, it should not be surprising for Eldoret and Kisumu to be co-integrated, as shown

13 in the test results. However, the subsequent tests, including the VECM estimation has shown no relationship. Even if maize prices in maize prices in Nairobi and Eldoret are not co-integrated, some additional tests were conducted to assess whether the price series are linked to one another in any way. The Granger causality tests implied that there is Granger causality from Eldoret to Nairobi in the short-term (same month and also at lags of 1 and 2 months) (Table 4). Moreover, the estimation of the Autoregressive Distributive Lag model implied that shocks to maize prices in Eldoret are partly transmitted to maize prices in Nairobi within the same month or one month later Combining temporal and spatial analysis To determine if maize markets have become more integrated, the spatial and temporal dimensions of price variation were combined in the analysis. In particular, the evolution of price differences between major markets over time was analyzed (Table 5). The mean difference (MD in the Table 5) between the major consumer market, Nairobi, and the coast has evolved over the study period from positive (higher price in Nairobi) to negative (higher prices in Mombasa). The mean squared difference (MSD), an indicator of variance between the two markets, has declined over the years. This is confirmed by the results of regression of MSD over time (lower part of Table 5). The mean price difference between Nairobi and the supply markets (Kitale and Eldoret), on the other hand, have remained relatively constant, with a distinct peak in 2002.

14 The price differences between Nairobi and the major market in Western Kenya (Kisumu) have also been reduced over time. To analyze the difference with a deficit area Garissa), the available data are not sufficient. Comparing the prices between the major import harbor (Mombasa) and the most important Western consumption market (Kisumu), also indicates a reduction in variability. The reduction in price differences with the production zone (Eldoret) is less distinct, but the regression still shows it is significant. 4. Conclusions The analysis of temporal variation shows that real maize prices have decreased over time in Kenya. Major factors in price variation are the differences between years, although a distinct one-season effect is demonstrated. Prices are clearly higher in the surplus zone during the high season, but lower otherwise. The coast has higher prices in the lower season. Price volatility has been decreasing over the years, and most likely market liberalization has played a positive effect on this trend. However, to isolate the effect of the liberalization, the analysis needs to be widened to include other factors known to influence prices, in particular climatic conditions and its effect on production, maize imports and the effect of international maize prices.

15 Acknowledgments The authors thank officers from the Ministry of Agriculture in Kenya (MoA/marketing branch) for providing the data and for Domisiano Mwamu for assembling in data base.

16 References Crawford, E., V. Kelly, T.S. Jayne, and H. J Input use and market development in Sub-Saharan Africa: an overview. Food Policy 28: De Groote, H., J.O. Okuro, C. Bett, L. Mose, M. Odendo, and E. Wekesa Assessing the demand for insect resistant maize varieties in Kenya combining Participatory Rural Appraisal into a Geographic Information System, p , In L. Sperling, et al., eds. Participatory Plant Breeding and Participatory Plant Genetic Resource Enhancement: An Africa-wide Exchange of Experiences. Proceedings of a workshop held in M ' bé, Ivory Coast. May 7-10, CGIAR Systemwide Program on Participatory Research and Gender Analysis., Cali, Colombia. Fackler, P.L., and B.K. Goodwin Chapter 17 Spatial price analysis, p , In B. L. Gardner and G. C. Rausser, eds. Handbook of Agricultural Economics: Marketing, Distribution and Consumers, Volume 1, Part 2 ed. Elsevier, Amsterdam. Gisselquist, D., and J.M. Grether An argument for deregulating the transfer of agricultural technologies to developing countries. World Bank Economic Review 14: Gisselquist, D., J. Nash, and C. Pray Deregulating the Transfer of Agricultural Technology: Lessons from Bangladesh, India, Turkey, and Zimbabwe.,. The World Bank Research Observer 17: Greene, W.H Econometric Analysis Mcmillan Publishing Company, New York.

17 Kherallah, M., C. Delgado, E. Gabre-Madhin, N. Minot, M. Johnson, N., and O Reforming Agricultural Markets in Africa IFPRI, Washington D.C. Stringer, R., and P. Pingali Agriculture's Contributions to Economic and Social Development. electronic Journal of Agricultural and Development Economics 1:1-5. Tripp, R Can biotechnology reach the poor? The adequacy of information and seed delivery. Food Policy 26: Tripp, R., and D. Rohrbach Policies for African seed enterprise development. Food Policy 26:. Wangia, C., S. Wangia, and H. De Groote Review of maize marketing in Kenya: Implementation and impact of liberalisation, , In D. K. Friesen and A. F. E. Palmer, eds. Integrated Approaches to Higher Maize Productivity in the New Millennium. Proceedings of the 7th Eastern and Southern Africa Regional Maize Conference Nairobi, Kenya, February CIMMYT,, Mexico, D. F.

18 FIGURES Figure 1. A Conceptual Approach for testing for Market Integration

19 Figure 2. Kenya's Agro-ecological Zones and the Location of Markets with Available Maize Price Dataa Figure 3. Evolution of Maize Prices in Kenya ( )

20 Figure 4. Seasonal Variation of Maize Prices in Kenya

21 TABLES Table 1. Estimation of trends of maize prices in Kenya ( ) Variable Nominal Price (KShs/kg) Real price (2009 KShs/kg) Estimated coefficients Std. Error Sig. Estimated coefficients Std. Error Sig. Constant Month (January =1) R St. err. Estimate 4 8 N Note: nominal maize prices have increased substantially, from 1991 to 2011, an increase of KShs/month; however, real prices have decreased, by KShs/kg/month, or US$ 1.2/ton/month.

22 Table 2. Regression of Maize Prices (1999 KShs/kg) on Time, Months and Locations Unstandardized Coefficients Standardized Coefficients Model B Std. Error Beta t Sig. 1 (Constant) month_cont Nakuru Kisumu Nairobi Mombass month month month month month month month month month month month

23 Table 3. Test results related to market integration between international and Kenyan maize markets Order of integration 1 Granger causality 2 ADL estimation Nairobi Mombasa Nairobi Mombasa Nairobi Mombasa White maize (SAFEX) No GC GC Pass through is 2 way Pass through from Mombasa to SAFEX: lag 4 Maize US no 2 No GC GC* No pass through Pass through from Maize US no 2 to Mombasa: lags 1, 4 1: Augmented Dickey Fuller and Philips-Perron tests (with and without drift) were conducted on level and first-difference time series to assess order of integration; the results implied that all price series were I(1). The Engle and Granger procedure was the applied to assess whether the series were CI(1,1) 2: Granger causality tests were applied to series (first-differenced series); GC for Nairobi and wmsafex implies that there is statistically significant (threshold of 5%) Granger causality from Nairobi to the price of white maize on SAFEX; GC* for Mombasa and Musa implies that there is statistically significant Granger causality from the price of white maize US no 2 to maize prices in Mombasa

24 Table 4: Test Results related to market integration between maize markets in Kenya Order of integration 1 Granger causality tests 2 Nairobi Mombasa Nakuru Eldoret Kisumu Nairobi Mombasa Nakuru Eldoret Kisumu Nairobi CI(1,1) No No CI(1,1) No GC 4,12 GC 0, 1, 2 GC 0, 1, 6 Mombasa CI(1,1) CI(1,1) CI(1,1) CI(1,1) GC 5 GC 9,11 No No Nakuru CI(1,1) CI(1,1) CI(1,1) CI(1,1) GC 1,10 No GC 0, 1 GC 0, 1, 2, 3, 4, 5 Eldoret No CI(1,1) CI(1,1) CI(1,1) GC 3,4 GC 0, 2, 3 GC 4 Kisumu CI(1,1) CI(1,1) CI(1,1) CI(1,1) No No No GC 1 VECM estimation VECM estimation: adjustment to long run equilibrium (months) 3 VECM estimation: selected lagged terms 4 Nairobi Mombasa Nakuru Eldoret Kisumu Nairobi Mombasa Nakuru Eldoret Kisumu Nairobi 3.57 PT: lags 6 Mombasa 1.67 Insignificant Insignificant PT: lags 5 PT: lags 9 PT: 1, 2, 7 No relation Nakuru 2.13 PT: 4, 10 Eldoret Insignificant PT: 2, 3, 10 No relation Kisumu Insignificant No relation PT: 1, 2 No relation 1: Augmented Dickey Fuller and Philips-Perron tests (with and without drift) were conducted on level and first-difference time series to assess order of integration; the results implied that all price series were I(1). The Engle and Granger procedure was the applied to assess whether the series were CI(1,1) 2: Granger causality tests were applied to series (first-differenced series); GC-5 for Mombasa and Nairobi implies that there is statistically significant (threshold of 5%) Granger causality from Nairobi to Mombasa at lag 5 3: Results are related to the VECM estimation linking any two series; 1.67 for Nairobi and Mombasa implies that the long-run equilibrium between maize prices in Nairobi and Mombasa is restored 1.67 months after a shock 4: Results are related to the VECM estimation linking any two series; PT: lags 5 for Mombasa and Nairobi implies that there is price transmission (PT) and that shocks to maize prices in Nairobi are passed through to maize prices in Mombasa 5 months later.

25 Table 5. Analysis of the Difference between Maize Prices in Major Towns in Kenya (1999 KShs/kg, ) From Nairobi to From Mombassa to Mombassa Eldoret Kitale Kisumu Garissa Kisumu Eldoret MSD MD MSD MD MSD MD MSD MD MSD MD MSD MD MSD MD Means Overall

26 N N Regression (Constant) *** *** *** *** coefficients (0.419) (1.358) (1.156) (1.217) Time - (st dev.) *** *** *** (0.004) (0.0187) (0.012) (0.013) High season ** *** *** (0.394) (1.434) (1.088) (1.143) N R St error estimate MSD= Mean squared difference between constant maize prices MD= Mean difference between constant maize prices

QUARTELY MAIZE MARKET ANALYSIS & OUTLOOK BULLETIN 1 OF 2015

QUARTELY MAIZE MARKET ANALYSIS & OUTLOOK BULLETIN 1 OF 2015 INTRODUCTION The following discussion is a review of the maize market environment. The analysis is updated on a quarterly 1 basis and the interval

QUARTELY MAIZE MARKET ANALYSIS & OUTLOOK BULLETIN 1 OF 2015 INTRODUCTION The following discussion is a review of the maize market environment. The analysis is updated on a quarterly 1 basis and the interval

Gasoline Empirical Analysis: Competition Bureau March 2005

Gasoline Empirical Analysis: Update of Four Elements of the January 2001 Conference Board study: "The Final Fifteen Feet of Hose: The Canadian Gasoline Industry in the Year 2000" Competition Bureau March

Gasoline Empirical Analysis: Update of Four Elements of the January 2001 Conference Board study: "The Final Fifteen Feet of Hose: The Canadian Gasoline Industry in the Year 2000" Competition Bureau March

UPPER MIDWEST MARKETING AREA THE BUTTER MARKET AND BEYOND

UPPER MIDWEST MARKETING AREA THE BUTTER MARKET 1987-2000 AND BEYOND STAFF PAPER 00-01 Prepared by: Henry H. Schaefer July 2000 Federal Milk Market Administrator s Office 4570 West 77th Street Suite 210

UPPER MIDWEST MARKETING AREA THE BUTTER MARKET 1987-2000 AND BEYOND STAFF PAPER 00-01 Prepared by: Henry H. Schaefer July 2000 Federal Milk Market Administrator s Office 4570 West 77th Street Suite 210

Structural Reforms and Agricultural Export Performance An Empirical Analysis

Structural Reforms and Agricultural Export Performance An Empirical Analysis D. Susanto, C. P. Rosson, and R. Costa Department of Agricultural Economics, Texas A&M University College Station, Texas INTRODUCTION

Structural Reforms and Agricultural Export Performance An Empirical Analysis D. Susanto, C. P. Rosson, and R. Costa Department of Agricultural Economics, Texas A&M University College Station, Texas INTRODUCTION

Regression Models for Saffron Yields in Iran

Regression Models for Saffron ields in Iran Sanaeinejad, S.H., Hosseini, S.N 1 Faculty of Agriculture, Ferdowsi University of Mashhad, Iran sanaei_h@yahoo.co.uk, nasir_nbm@yahoo.com, Abstract: Saffron

Regression Models for Saffron ields in Iran Sanaeinejad, S.H., Hosseini, S.N 1 Faculty of Agriculture, Ferdowsi University of Mashhad, Iran sanaei_h@yahoo.co.uk, nasir_nbm@yahoo.com, Abstract: Saffron

Volatility returns to the coffee market as prices stay low

Volatility returns to the coffee market as prices stay low Daily coffee prices hit their lowest level in 19 months during August, as commodity markets worldwide were negatively affected by currency movements

Volatility returns to the coffee market as prices stay low Daily coffee prices hit their lowest level in 19 months during August, as commodity markets worldwide were negatively affected by currency movements

Statistics & Agric.Economics Deptt., Tocklai Experimental Station, Tea Research Association, Jorhat , Assam. ABSTRACT

Two and a Bud 59(2):152-156, 2012 RESEARCH PAPER Global tea production and export trend with special reference to India Prasanna Kumar Bordoloi Statistics & Agric.Economics Deptt., Tocklai Experimental

Two and a Bud 59(2):152-156, 2012 RESEARCH PAPER Global tea production and export trend with special reference to India Prasanna Kumar Bordoloi Statistics & Agric.Economics Deptt., Tocklai Experimental

Economic Role of Maize in Thailand

Economic Role of Maize in Thailand Hnin Ei Win Center for Applied Economics Research Thailand INTRODUCTION Maize is an important agricultural product in Thailand which is being used for both food and feed

Economic Role of Maize in Thailand Hnin Ei Win Center for Applied Economics Research Thailand INTRODUCTION Maize is an important agricultural product in Thailand which is being used for both food and feed

2018/19 expected to be the second year of surplus

2018/19 expected to be the second year of surplus Coffee year 2018/19 is expected to be the second consecutive season of surplus, as global output, estimated at 167.47 million bags, exceeds world consumption,

2018/19 expected to be the second year of surplus Coffee year 2018/19 is expected to be the second consecutive season of surplus, as global output, estimated at 167.47 million bags, exceeds world consumption,

Coffee market continues downward trend

Coffee market continues downward trend Since August 2017, the ICO composite indicator price has declined in each month except January 2018. The composite indicator decreased by 1.1% in March 2018 to an

Coffee market continues downward trend Since August 2017, the ICO composite indicator price has declined in each month except January 2018. The composite indicator decreased by 1.1% in March 2018 to an

QUARTERLY REVIEW OF THE PERFORMANCE OF THE DAIRY INDUSTRY 1

QUARTERLY REVIEW OF THE PERFORMANCE OF THE DAIRY INDUSTRY 1 The information in this document is from sources deemed to be correct. Milk SA, the MPO and SAMPRO are not responsible for the results of any

QUARTERLY REVIEW OF THE PERFORMANCE OF THE DAIRY INDUSTRY 1 The information in this document is from sources deemed to be correct. Milk SA, the MPO and SAMPRO are not responsible for the results of any

ECONOMICS OF COCONUT PRODUCTS AN ANALYTICAL STUDY. Coconut is an important tree crop with diverse end-uses, grown in many states of India.

ECONOMICS OF COCONUT PRODUCTS AN ANALYTICAL STUDY Introduction Coconut is an important tree crop with diverse end-uses, grown in many states of India. Coconut palm is the benevolent provider of the basic

ECONOMICS OF COCONUT PRODUCTS AN ANALYTICAL STUDY Introduction Coconut is an important tree crop with diverse end-uses, grown in many states of India. Coconut palm is the benevolent provider of the basic

World sugar market. Platts/Kingsman EU conference Geneva 14th of April Benoît Boisleux

World sugar market Platts/Kingsman EU conference Geneva 14th of April 215 Benoît Boisleux One year evolution of world prices NY 11 (2 nd month continuation) Cts/lb 2 Kingsman EU conf 8 April 214 NY 2nd

World sugar market Platts/Kingsman EU conference Geneva 14th of April 215 Benoît Boisleux One year evolution of world prices NY 11 (2 nd month continuation) Cts/lb 2 Kingsman EU conf 8 April 214 NY 2nd

Coffee market ends 2017/18 in surplus

Coffee market ends 217/18 in surplus World coffee production in coffee year 217/18 is estimated 5.7% higher at 164.81 million bags as output of Arabica increased by 2.2% to 11.82, and Robusta grew 11.7%

Coffee market ends 217/18 in surplus World coffee production in coffee year 217/18 is estimated 5.7% higher at 164.81 million bags as output of Arabica increased by 2.2% to 11.82, and Robusta grew 11.7%

MARKET NEWSLETTER No 93 April 2015

Focus on OLIVE OIL IMPORT TRENDS IN RUSSIA Russian imports of olive oil and olive pomace oil grew at a constant rate between 2/1 and 213/14 when they rose from 3 62 t to 34 814 t (Chart 1). The only exceptions

Focus on OLIVE OIL IMPORT TRENDS IN RUSSIA Russian imports of olive oil and olive pomace oil grew at a constant rate between 2/1 and 213/14 when they rose from 3 62 t to 34 814 t (Chart 1). The only exceptions

OF THE VARIOUS DECIDUOUS and

(9) PLAXICO, JAMES S. 1955. PROBLEMS OF FACTOR-PRODUCT AGGRE- GATION IN COBB-DOUGLAS VALUE PRODUCTIVITY ANALYSIS. JOUR. FARM ECON. 37: 644-675, ILLUS. (10) SCHICKELE, RAINER. 1941. EFFECT OF TENURE SYSTEMS

(9) PLAXICO, JAMES S. 1955. PROBLEMS OF FACTOR-PRODUCT AGGRE- GATION IN COBB-DOUGLAS VALUE PRODUCTIVITY ANALYSIS. JOUR. FARM ECON. 37: 644-675, ILLUS. (10) SCHICKELE, RAINER. 1941. EFFECT OF TENURE SYSTEMS

Figure 1: Quartely milk production and gross value

Million Litres Million Rands QUARTERLY DAIRY MARKET ANALYSIS BULLETIN 1 OF 215 1. INTRODUCTION The following discussion is a review of the dairy market environment. The analysis is updated on a quarterly

Million Litres Million Rands QUARTERLY DAIRY MARKET ANALYSIS BULLETIN 1 OF 215 1. INTRODUCTION The following discussion is a review of the dairy market environment. The analysis is updated on a quarterly

Estudio de las Cadenas de Valor de Maíz Blanco y Frijol en Centroamérica, IICA, RED SICTA, Cooperación Suiza en America Central, 2013.

REGIONAL MARKET FUNDAMENTALS Central America February 24, 2017 ABOUT THIS REPORT This report provides an overview of typical production and market behavior in Central America staple grains market. The

REGIONAL MARKET FUNDAMENTALS Central America February 24, 2017 ABOUT THIS REPORT This report provides an overview of typical production and market behavior in Central America staple grains market. The

Prices for all coffee groups increased in May

Prices for all coffee groups increased in May In May 2018, the ICO composite indicator increased by 0.7% to an average of 113.34 US cents/lb, following three months of declines. Prices for all coffee groups

Prices for all coffee groups increased in May In May 2018, the ICO composite indicator increased by 0.7% to an average of 113.34 US cents/lb, following three months of declines. Prices for all coffee groups

2. The proposal has been sent to the Virtual Screening Committee (VSC) for evaluation and will be examined by the Executive Board in September 2008.

for evaluation and will be examined by the Executive Board in September 2008.") WP Board 1052/08 International Coffee Organization Organización Internacional del Café Organização Internacional do Café Organisation Internationale du Café 20 August 2008 English only Projects/Common

WP Board 1052/08 International Coffee Organization Organización Internacional del Café Organização Internacional do Café Organisation Internationale du Café 20 August 2008 English only Projects/Common

Monthly Economic Letter

Monthly Economic Letter Cotton Market Fundamentals & Price Outlook RECENT PRICE MOVEMENT After some upward movement in April, most benchmark prices turned lower in early May. After climbing to the upper

Monthly Economic Letter Cotton Market Fundamentals & Price Outlook RECENT PRICE MOVEMENT After some upward movement in April, most benchmark prices turned lower in early May. After climbing to the upper

MARKET ANALYSIS REPORT NO 1 OF 2015: TABLE GRAPES

MARKET ANALYSIS REPORT NO 1 OF 215: TABLE GRAPES 1. INTRODUCTION The following text is a review of the table grapes marketing environment. This analysis is updated on a quarterly 1 basis. The interval

MARKET ANALYSIS REPORT NO 1 OF 215: TABLE GRAPES 1. INTRODUCTION The following text is a review of the table grapes marketing environment. This analysis is updated on a quarterly 1 basis. The interval

ANALYSIS OF THE EVOLUTION AND DISTRIBUTION OF MAIZE CULTIVATED AREA AND PRODUCTION IN ROMANIA

ANALYSIS OF THE EVOLUTION AND DISTRIBUTION OF MAIZE CULTIVATED AREA AND PRODUCTION IN ROMANIA Agatha POPESCU University of Agricultural Sciences and Veterinary Medicine, Bucharest, 59 Marasti, District

ANALYSIS OF THE EVOLUTION AND DISTRIBUTION OF MAIZE CULTIVATED AREA AND PRODUCTION IN ROMANIA Agatha POPESCU University of Agricultural Sciences and Veterinary Medicine, Bucharest, 59 Marasti, District

Wine-Tasting by Numbers: Using Binary Logistic Regression to Reveal the Preferences of Experts

Wine-Tasting by Numbers: Using Binary Logistic Regression to Reveal the Preferences of Experts When you need to understand situations that seem to defy data analysis, you may be able to use techniques

Wine-Tasting by Numbers: Using Binary Logistic Regression to Reveal the Preferences of Experts When you need to understand situations that seem to defy data analysis, you may be able to use techniques

Growing divergence between Arabica and Robusta exports

Growing divergence between Arabica and Robusta exports In April 218, the ICO composite indicator decreased by.4% to an average of 112.56, with the daily price ranging between 11.49 and 114.73. Prices for

Growing divergence between Arabica and Robusta exports In April 218, the ICO composite indicator decreased by.4% to an average of 112.56, with the daily price ranging between 11.49 and 114.73. Prices for

ICC July 2010 Original: French. Study. International Coffee Council 105 th Session September 2010 London, England

ICC 15-2 12 July 21 Original: French Study E International Coffee Council 15 th Session 22 24 September 21 London, England Relations between coffee stocks and prices Background In the context of its programme

ICC 15-2 12 July 21 Original: French Study E International Coffee Council 15 th Session 22 24 September 21 London, England Relations between coffee stocks and prices Background In the context of its programme

Coffee prices rose slightly in January 2019

Coffee prices rose slightly in January 2019 In January 2019, the ICO composite indicator rose by 0.9% to 101.56 US cents/lb as prices for all group indicators increased. After starting at a low of 99.16

Coffee prices rose slightly in January 2019 In January 2019, the ICO composite indicator rose by 0.9% to 101.56 US cents/lb as prices for all group indicators increased. After starting at a low of 99.16

2016 China Dry Bean Historical production And Estimated planting intentions Analysis

2016 China Dry Bean Historical production And Estimated planting intentions Analysis Performed by Fairman International Business Consulting 1 of 10 P a g e I. EXECUTIVE SUMMARY A. Overall Bean Planting

2016 China Dry Bean Historical production And Estimated planting intentions Analysis Performed by Fairman International Business Consulting 1 of 10 P a g e I. EXECUTIVE SUMMARY A. Overall Bean Planting

Sugar Industry Update

January 19, 217 I Industry Research Sugar Industry Update Contact: Madan Sabnavis Chief Economist mailto:madan.sabnavis@careratings.com 91-22-6743489 Bhagyashree Bhati Research Analyst bhagyashree.bhati@careratings.com

January 19, 217 I Industry Research Sugar Industry Update Contact: Madan Sabnavis Chief Economist mailto:madan.sabnavis@careratings.com 91-22-6743489 Bhagyashree Bhati Research Analyst bhagyashree.bhati@careratings.com

1. Expressed in billions of real dollars, seasonally adjusted, annual rate.

ROUTPUT -- Real GNP/GDP 1. Expressed in billions of real dollars, seasonally adjusted, annual rate. 2. First Monthly Vintage: 1965:M11 First Quarterly Vintage: 1965:Q4 3. First Observation: 1947:Q1 4.

ROUTPUT -- Real GNP/GDP 1. Expressed in billions of real dollars, seasonally adjusted, annual rate. 2. First Monthly Vintage: 1965:M11 First Quarterly Vintage: 1965:Q4 3. First Observation: 1947:Q1 4.

The aim of the thesis is to determine the economic efficiency of production factors utilization in S.C. AGROINDUSTRIALA BUCIUM S.A.

The aim of the thesis is to determine the economic efficiency of production factors utilization in S.C. AGROINDUSTRIALA BUCIUM S.A. The research objectives are: to study the history and importance of grape

The aim of the thesis is to determine the economic efficiency of production factors utilization in S.C. AGROINDUSTRIALA BUCIUM S.A. The research objectives are: to study the history and importance of grape

FACTORS DETERMINING UNITED STATES IMPORTS OF COFFEE

12 November 1953 FACTORS DETERMINING UNITED STATES IMPORTS OF COFFEE The present paper is the first in a series which will offer analyses of the factors that account for the imports into the United States

12 November 1953 FACTORS DETERMINING UNITED STATES IMPORTS OF COFFEE The present paper is the first in a series which will offer analyses of the factors that account for the imports into the United States

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S.

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Required Report - public distribution Date: GAIN Report

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Required Report - public distribution Date: GAIN Report

MEASURING THE OPPORTUNITY COSTS OF TRADE-RELATED CAPACITY DEVELOPMENT IN SUB-SAHARAN AFRICA

Tendie Mugadza University of Cape Town MEASURING THE OPPORTUNITY COSTS OF TRADE-RELATED CAPACITY DEVELOPMENT IN SUB-SAHARAN AFRICA 1 PROBLEM: Background/Introduction Africa lags behind in development compared

Tendie Mugadza University of Cape Town MEASURING THE OPPORTUNITY COSTS OF TRADE-RELATED CAPACITY DEVELOPMENT IN SUB-SAHARAN AFRICA 1 PROBLEM: Background/Introduction Africa lags behind in development compared

Mexico Milk Cow Numbers and Milk Production per Cow,

TABLE OF CONTENTS 1. Mexico 1.1. Mexico Milk Market Introduction 1.1.1. Dairy Market Structure and Supply Chain in Mexico 1.1.2. Mexico Cow Milk Market Production and Fluid Milk Consumption by Volume,

TABLE OF CONTENTS 1. Mexico 1.1. Mexico Milk Market Introduction 1.1.1. Dairy Market Structure and Supply Chain in Mexico 1.1.2. Mexico Cow Milk Market Production and Fluid Milk Consumption by Volume,

Record exports in coffee year 2017/18

Record exports in coffee year 2017/18 Total coffee exports increased each year since 2010/11 with a new record reached in 2017/18 at 121.86 million bags, 2% higher than 2016/17. In the twelve months ending

Record exports in coffee year 2017/18 Total coffee exports increased each year since 2010/11 with a new record reached in 2017/18 at 121.86 million bags, 2% higher than 2016/17. In the twelve months ending

Problem Set #15 Key. Measuring the Effects of Promotion II

Problem Set #15 Key Sonoma State University Business 580-Business Intelligence Dr. Cuellar Measuring the Effects of Promotion II 1. For Total Wine Sales Using a Non-Promoted Price of $9 and a Promoted

Problem Set #15 Key Sonoma State University Business 580-Business Intelligence Dr. Cuellar Measuring the Effects of Promotion II 1. For Total Wine Sales Using a Non-Promoted Price of $9 and a Promoted

Appendix A. Table A.1: Logit Estimates for Elasticities

Estimates from historical sales data Appendix A Table A.1. reports the estimates from the discrete choice model for the historical sales data. Table A.1: Logit Estimates for Elasticities Dependent Variable:

Estimates from historical sales data Appendix A Table A.1. reports the estimates from the discrete choice model for the historical sales data. Table A.1: Logit Estimates for Elasticities Dependent Variable:

AJAE Appendix: Testing Household-Specific Explanations for the Inverse Productivity Relationship

AJAE Appendix: Testing Household-Specific Explanations for the Inverse Productivity Relationship Juliano Assunção Department of Economics PUC-Rio Luis H. B. Braido Graduate School of Economics Getulio

AJAE Appendix: Testing Household-Specific Explanations for the Inverse Productivity Relationship Juliano Assunção Department of Economics PUC-Rio Luis H. B. Braido Graduate School of Economics Getulio

Investment Wines. - Risk Analysis. Prepared by: Michael Shortell & Adiam Woldetensae Date: 06/09/2015

Investment Wines - Risk Analysis Prepared by: Michael Shortell & Adiam Woldetensae Date: 06/09/2015 Purpose Look at investment wines & examine factors that affect wine prices over time We will identify

Investment Wines - Risk Analysis Prepared by: Michael Shortell & Adiam Woldetensae Date: 06/09/2015 Purpose Look at investment wines & examine factors that affect wine prices over time We will identify

Record Exports for Coffee Year 2016/17

Record Exports for Coffee Year 2016/17 Total exports in September 2017 reached 8.34 million bags, compared to 9.8 million in September 2016. While coffee year 2016/17 registered a decrease in its final

Record Exports for Coffee Year 2016/17 Total exports in September 2017 reached 8.34 million bags, compared to 9.8 million in September 2016. While coffee year 2016/17 registered a decrease in its final

IMPACT OF PRICING POLICY ON DOMESTIC PRICES OF SUGAR IN INDIA

RESEARCH ARTICLE IMPACT OF PRICING POLICY ON DOMESTIC PRICES OF SUGAR IN INDIA Kavita*, R.K. Grover, Sunita and Raj Kumar Department of Agricultural Economics, CCSHAU, Hisar-125004, Haryana Email: kavitayadav230@gmail.com

RESEARCH ARTICLE IMPACT OF PRICING POLICY ON DOMESTIC PRICES OF SUGAR IN INDIA Kavita*, R.K. Grover, Sunita and Raj Kumar Department of Agricultural Economics, CCSHAU, Hisar-125004, Haryana Email: kavitayadav230@gmail.com

Outlook for the World Coffee Market

Outlook for the World Coffee Market 8 th AFRICAN FINE COFFEE CONFERENCE & EXHIBITION 17 to 19 February 2011 Arusha, Tanzania José Sette Executive Director a.i. 225 ICO composite indicator price Monthly:

Outlook for the World Coffee Market 8 th AFRICAN FINE COFFEE CONFERENCE & EXHIBITION 17 to 19 February 2011 Arusha, Tanzania José Sette Executive Director a.i. 225 ICO composite indicator price Monthly:

Dairy Market. July The U.S. average all-milk price rose by $0.20 per hundredweight in May from a

Dairy Market Dairy Management Inc. R E P O R T Volume 20 No. 6 July 2017 DMI NMPF Overview The U.S. average all-milk price rose by $0.20 per hundredweight in May from a month earlier, and the June federal

Dairy Market Dairy Management Inc. R E P O R T Volume 20 No. 6 July 2017 DMI NMPF Overview The U.S. average all-milk price rose by $0.20 per hundredweight in May from a month earlier, and the June federal

Liquidity and Risk Premia in Electricity Futures Markets

Liquidity and Risk Premia in Electricity Futures Markets IAEE Conference, Singapore, June 2017 Ivan Diaz-Rainey Associate Professor of Finance & Co-Director of the Otago Energy Research Centre (OERC) With

Liquidity and Risk Premia in Electricity Futures Markets IAEE Conference, Singapore, June 2017 Ivan Diaz-Rainey Associate Professor of Finance & Co-Director of the Otago Energy Research Centre (OERC) With

MARKET NEWSLETTER No 111 December 2016

On 1 January 2017 the new International Agreement on Olive Oil and Table Olives, 2015, came into force, being the sixth International Agreement of the Organisation. This new Agreement will allow the IOC

On 1 January 2017 the new International Agreement on Olive Oil and Table Olives, 2015, came into force, being the sixth International Agreement of the Organisation. This new Agreement will allow the IOC

Coffee market settles lower amidst strong global exports

Coffee market settles lower amidst strong global exports The ICO composite indicator price declined by 1.2% in February 2018 to an average of 114.19 US cents/lb. Indicator prices for all three Arabica

Coffee market settles lower amidst strong global exports The ICO composite indicator price declined by 1.2% in February 2018 to an average of 114.19 US cents/lb. Indicator prices for all three Arabica

"Primary agricultural commodity trade and labour market outcome

"Primary agricultural commodity trade and labour market outcomes" FERDI - Fondation pour les Etudes et Recherches sur le Developpement International African Economic Conference 2014 - Knowledge and innovation

"Primary agricultural commodity trade and labour market outcomes" FERDI - Fondation pour les Etudes et Recherches sur le Developpement International African Economic Conference 2014 - Knowledge and innovation

Monthly Economic Letter U.S. and Global Market Fundamentals

Monthly Economic Letter U.S. and Global Market Fundamentals August 2012 www.cottoninc.com After trading within relatively narrow bands throughout July, New York futures moved higher in early August, with

Monthly Economic Letter U.S. and Global Market Fundamentals August 2012 www.cottoninc.com After trading within relatively narrow bands throughout July, New York futures moved higher in early August, with

Coffee prices maintain downward trend as 2015/16 production estimates show slight recovery

Coffee prices maintain downward trend as 2015/16 production estimates show slight recovery The coffee market fell again in December 2015, reaching its second lowest monthly average of the year. This decrease

Coffee prices maintain downward trend as 2015/16 production estimates show slight recovery The coffee market fell again in December 2015, reaching its second lowest monthly average of the year. This decrease

MONTHLY COFFEE MARKET REPORT

E MONTHLY COFFEE MARKET REPORT June 2013 Coffee prices fell sharply in June 2013, as market fundamentals, combined with an uncertain macroeconomic outlook, drove the ICO composite indicator price to its

E MONTHLY COFFEE MARKET REPORT June 2013 Coffee prices fell sharply in June 2013, as market fundamentals, combined with an uncertain macroeconomic outlook, drove the ICO composite indicator price to its

Food Additive Produced by IAR Team Focus Technology Co., Ltd

Food Additive 2012.03 Produced by IAR Team Focus Technology Co., Ltd Contents 1. 2009-2011 Chinese Citric Acid Export Data Analysis... 3 2009-2011 Major Importers of Chinese Citric Acid...4 2. 2009-2011

Food Additive 2012.03 Produced by IAR Team Focus Technology Co., Ltd Contents 1. 2009-2011 Chinese Citric Acid Export Data Analysis... 3 2009-2011 Major Importers of Chinese Citric Acid...4 2. 2009-2011

Sunflower seed COMMODITY PROFILE

Contents 1. Description of the industry............................ 1 2. Marketing structure................................. 3 3. Strategic challenges................................ 6 4. Other information..................................

Contents 1. Description of the industry............................ 1 2. Marketing structure................................. 3 3. Strategic challenges................................ 6 4. Other information..................................

(A report prepared for Milk SA)

") South African Milk Processors Organisation The voluntary organisation of milk processors for the promotion of the development of the secondary dairy industry to the benefit of the dairy industry, the consumer

South African Milk Processors Organisation The voluntary organisation of milk processors for the promotion of the development of the secondary dairy industry to the benefit of the dairy industry, the consumer

Fair Trade and Free Entry: Can a Disequilibrium Market Serve as a Development Tool? Online Appendix September 2014

Fair Trade and Free Entry: Can a Disequilibrium Market Serve as a Development Tool? 1. Data Construction Online Appendix September 2014 The data consist of the Association s records on all coffee acquisitions

Fair Trade and Free Entry: Can a Disequilibrium Market Serve as a Development Tool? 1. Data Construction Online Appendix September 2014 The data consist of the Association s records on all coffee acquisitions

United Nations Conference on Trade and Development

United Nations Conference on Trade and Development 10th MULTI-YEAR EXPERT MEETING ON COMMODITIES AND DEVELOPMENT 25-26 April 2018, Geneva Cocoa Boom & Bust: A Review of Cocoa Market Developments By Laurent

United Nations Conference on Trade and Development 10th MULTI-YEAR EXPERT MEETING ON COMMODITIES AND DEVELOPMENT 25-26 April 2018, Geneva Cocoa Boom & Bust: A Review of Cocoa Market Developments By Laurent

IMPACT OF RAINFALL AND TEMPERATURE ON TEA PRODUCTION IN UNDIVIDED SIVASAGAR DISTRICT

International Journal of Agricultural Science and Research (IJASR) ISSN (P): 2250-0057; ISSN (E): 2321-0087 Vol. 8, Issue 1 Feb 2018, 51-56 TJPRC Pvt. Ltd. IMPACT OF RAINFALL AND TEMPERATURE ON TEA PRODUCTION

International Journal of Agricultural Science and Research (IJASR) ISSN (P): 2250-0057; ISSN (E): 2321-0087 Vol. 8, Issue 1 Feb 2018, 51-56 TJPRC Pvt. Ltd. IMPACT OF RAINFALL AND TEMPERATURE ON TEA PRODUCTION

Acreage Forecast

World (John Sandbakken and Larry Kleingartner) The sunflower is native to North America but commercialization of the plant took place in Russia. Sunflower oil is the preferred oil in most of Europe, Mexico

World (John Sandbakken and Larry Kleingartner) The sunflower is native to North America but commercialization of the plant took place in Russia. Sunflower oil is the preferred oil in most of Europe, Mexico

Notes on the Philadelphia Fed s Real-Time Data Set for Macroeconomists (RTDSM) Capacity Utilization. Last Updated: December 21, 2016

Capacity Utilization. Last Updated: December 21, 2016") 1 Notes on the Philadelphia Fed s Real-Time Data Set for Macroeconomists (RTDSM) Capacity Utilization Last Updated: December 21, 2016 I. General Comments This file provides documentation for the Philadelphia

1 Notes on the Philadelphia Fed s Real-Time Data Set for Macroeconomists (RTDSM) Capacity Utilization Last Updated: December 21, 2016 I. General Comments This file provides documentation for the Philadelphia

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S.

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Voluntary - Public Date: 4/24/2013 GAIN Report Number:

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Voluntary - Public Date: 4/24/2013 GAIN Report Number:

DERIVED DEMAND FOR FRESH CHEESE PRODUCTS IMPORTED INTO JAPAN

PBTC 05-04 PBTC 02-6 DERIVED DEMAND FOR FRESH CHEESE PRODUCTS IMPORTED INTO JAPAN By Andreas P. Christou, Richard L. Kilmer, James A. Stearns, Shiferaw T. Feleke, & Jiaoju Ge PBTC 05-04 September 2005

PBTC 05-04 PBTC 02-6 DERIVED DEMAND FOR FRESH CHEESE PRODUCTS IMPORTED INTO JAPAN By Andreas P. Christou, Richard L. Kilmer, James A. Stearns, Shiferaw T. Feleke, & Jiaoju Ge PBTC 05-04 September 2005

World of sugar PAGE 54

World of sugar More than 1 countries produce sugar, about 8% of which is made from sugar cane grown primarily in the tropical and sub-tropical zones of the southern hemisphere, and the balance from sugar

World of sugar More than 1 countries produce sugar, about 8% of which is made from sugar cane grown primarily in the tropical and sub-tropical zones of the southern hemisphere, and the balance from sugar

PEEL RIVER HEALTH ASSESSMENT

PEEL RIVER HEALTH ASSESSMENT CONTENTS SUMMARY... 2 Overall River Health Scoring... 2 Overall Data Sufficiency Scoring... 2 HYDROLOGY... 3 Overall Hydrology River Health Scoring... 3 Hydrology Data Sufficiency...

PEEL RIVER HEALTH ASSESSMENT CONTENTS SUMMARY... 2 Overall River Health Scoring... 2 Overall Data Sufficiency Scoring... 2 HYDROLOGY... 3 Overall Hydrology River Health Scoring... 3 Hydrology Data Sufficiency...

Problem Set #3 Key. Forecasting

Problem Set #3 Key Sonoma State University Business 581E Dr. Cuellar The data set bus581e_ps3.dta is a Stata data set containing annual sales (cases) and revenue from December 18, 2004 to April 2 2011.

Problem Set #3 Key Sonoma State University Business 581E Dr. Cuellar The data set bus581e_ps3.dta is a Stata data set containing annual sales (cases) and revenue from December 18, 2004 to April 2 2011.

Dairy Market. Overview. Commercial Use of Dairy Products

Dairy Market Dairy Management Inc. R E P O R T Volume 21 No. 6 June 2018 DMI NMPF Overview U.S. dairy markets received a one-two punch during the first weeks of June in the form of collateral damage from

Dairy Market Dairy Management Inc. R E P O R T Volume 21 No. 6 June 2018 DMI NMPF Overview U.S. dairy markets received a one-two punch during the first weeks of June in the form of collateral damage from

DETERMINANTS OF GROWTH

POLICY OPTIONS AND CHALLENGES FOR DEVELOPING ASIA PERSPECTIVES FROM THE IMF AND ASIA APRIL 19-20, 2007 TOKYO DETERMINANTS OF GROWTH IN LOW-INCOME ASIA ARI AISEN INTERNATIONAL MONETARY FUND Paper presented

POLICY OPTIONS AND CHALLENGES FOR DEVELOPING ASIA PERSPECTIVES FROM THE IMF AND ASIA APRIL 19-20, 2007 TOKYO DETERMINANTS OF GROWTH IN LOW-INCOME ASIA ARI AISEN INTERNATIONAL MONETARY FUND Paper presented

Angela Mariani. University of Naples Parthenope

Angela Mariani University of Naples Parthenope Workshop Mediterranean products in the global market Section 6: The global market for wine: issues and prospects p 17 June 2008 BRIEF COMMENTS ON THE FOLLOWING

Angela Mariani University of Naples Parthenope Workshop Mediterranean products in the global market Section 6: The global market for wine: issues and prospects p 17 June 2008 BRIEF COMMENTS ON THE FOLLOWING

EMBARGO TO ON FRIDAY 16 SEPTEMBER. Scotch Whisky Association. Exports of Scotch Whisky; Year to end of June 2016 (2016 H1)

") EMBARGO TO 00.01 ON FRIDAY 16 SEPTEMBER Scotch Whisky Association Exports of Scotch Whisky; Year to end of June 2016 (2016 H1) VOLUME UP 3.1% to 531 MILLION bottles VALUE DOWN SLIGHTLY BY 1.0% TO 1.70

EMBARGO TO 00.01 ON FRIDAY 16 SEPTEMBER Scotch Whisky Association Exports of Scotch Whisky; Year to end of June 2016 (2016 H1) VOLUME UP 3.1% to 531 MILLION bottles VALUE DOWN SLIGHTLY BY 1.0% TO 1.70

The Inclusiveness of Africa s Recent High- Growth Episode: Evidence from Six Countries

The Inclusiveness of Africa s Recent High- Growth Episode: Evidence from Six Countries Rodrigo Garcia-Verdu, Abebe Aemro Selassie, and Alun Thomas African Department International Monetary Fund 2012 Economic

The Inclusiveness of Africa s Recent High- Growth Episode: Evidence from Six Countries Rodrigo Garcia-Verdu, Abebe Aemro Selassie, and Alun Thomas African Department International Monetary Fund 2012 Economic

Spatial equilibrium analysis of vine and wine industry in Argentina. 2 The concern of improper government intervention to Argentinean vine and wine

Spatial equilibrium analysis of vine and wine industry in Argentina Content 1 Introduction 1.1 Background information and problem statement 1.2 Research objective and hypotheses 1.3 Methodology 2 The concern

Spatial equilibrium analysis of vine and wine industry in Argentina Content 1 Introduction 1.1 Background information and problem statement 1.2 Research objective and hypotheses 1.3 Methodology 2 The concern

July marks another month of continuous low prices

July marks another month of continuous low prices In July 2018, the ICO composite indicator price decreased by 2.9% to an average of 107.20 US cents/lb, which is the lowest monthly average for July since

July marks another month of continuous low prices In July 2018, the ICO composite indicator price decreased by 2.9% to an average of 107.20 US cents/lb, which is the lowest monthly average for July since

BORDEAUX WINE VINTAGE QUALITY AND THE WEATHER ECONOMETRIC ANALYSIS

BORDEAUX WINE VINTAGE QUALITY AND THE WEATHER ECONOMETRIC ANALYSIS WINE PRICES OVER VINTAGES DATA The data sheet contains market prices for a collection of 13 high quality Bordeaux wines (not including

BORDEAUX WINE VINTAGE QUALITY AND THE WEATHER ECONOMETRIC ANALYSIS WINE PRICES OVER VINTAGES DATA The data sheet contains market prices for a collection of 13 high quality Bordeaux wines (not including

Brazil Milk Cow Numbers and Milk Production per Cow,

TABLE OF CONTENTS 1. Brazil 1.1. Brazil Milk Market Introduction 1.1.1. Brazil Cow Milk Market Production and Fluid Milk Consumption by Volume, 1.1.2. Brazil Milk Cow Numbers and Milk Production per Cow,

TABLE OF CONTENTS 1. Brazil 1.1. Brazil Milk Market Introduction 1.1.1. Brazil Cow Milk Market Production and Fluid Milk Consumption by Volume, 1.1.2. Brazil Milk Cow Numbers and Milk Production per Cow,

Chapter 3. Labor Productivity and Comparative Advantage: The Ricardian Model

Chapter 3 Labor Productivity and Comparative Advantage: The Ricardian Model Preview Opportunity costs and comparative advantage A one-factor Ricardian model Production possibilities Gains from trade Wages

Chapter 3 Labor Productivity and Comparative Advantage: The Ricardian Model Preview Opportunity costs and comparative advantage A one-factor Ricardian model Production possibilities Gains from trade Wages

Preview. Chapter 3. Labor Productivity and Comparative Advantage: The Ricardian Model

Chapter 3 Labor Productivity and Comparative Advantage: The Ricardian Model Preview Opportunity costs and comparative advantage A one-factor Ricardian model Production possibilities Gains from trade Wages

Chapter 3 Labor Productivity and Comparative Advantage: The Ricardian Model Preview Opportunity costs and comparative advantage A one-factor Ricardian model Production possibilities Gains from trade Wages

Preview. Introduction (cont.) Introduction. Comparative Advantage and Opportunity Cost (cont.) Comparative Advantage and Opportunity Cost

Introduction. Comparative Advantage and Opportunity Cost (cont.) Comparative Advantage and Opportunity Cost") Chapter 3 Labor Productivity and Comparative Advantage: The Ricardian Model Preview Opportunity costs and comparative advantage A one-factor Ricardian model Production possibilities Gains from trade Wages

Chapter 3 Labor Productivity and Comparative Advantage: The Ricardian Model Preview Opportunity costs and comparative advantage A one-factor Ricardian model Production possibilities Gains from trade Wages

Agriculture and Food Authority

Agriculture and Food Authority Presentation by: SOLOMON ODERA Interim Head of Sugar Directorate Agriculture and Food Authority November, 2017 KENYA SUGARCANE INDUSTRY OUTLINE 1) Introduction 2) Kenyan

Agriculture and Food Authority Presentation by: SOLOMON ODERA Interim Head of Sugar Directorate Agriculture and Food Authority November, 2017 KENYA SUGARCANE INDUSTRY OUTLINE 1) Introduction 2) Kenyan

their cultivation in and 36% of expansion in crop NCARE). growing in olive Area: sq km (UN, 2008) (UN, 2010/ /15) GNI per Bank, 2010) 2009)

. growing in olive Area: sq km (UN, 2008) (UN, 2010/ /15) GNI per Bank, 2010) 2009)") Policies - Jordan 2012 1. GENERAL DESCRIPTION OF OLIVE GROWING IN JORDAN 1.1. Introductionn The olive tree is one of the most important and oldest crops in Jordan where it is ntertwined with the daily

Policies - Jordan 2012 1. GENERAL DESCRIPTION OF OLIVE GROWING IN JORDAN 1.1. Introductionn The olive tree is one of the most important and oldest crops in Jordan where it is ntertwined with the daily

Oregon Wine Industry Sustainable Showcase. Gregory V. Jones

Oregon Wine Industry Sustainable Showcase Gregory V. Jones Panel Framework Oregon wineries and vineyards are implementing innovative sustainability and environmental practices across the entire system

Oregon Wine Industry Sustainable Showcase Gregory V. Jones Panel Framework Oregon wineries and vineyards are implementing innovative sustainability and environmental practices across the entire system

Chapter 3. Labor Productivity and Comparative Advantage: The Ricardian Model. Pearson Education Limited All rights reserved.

Chapter 3 Labor Productivity and Comparative Advantage: The Ricardian Model 1-1 Preview Opportunity costs and comparative advantage A one-factor Ricardian model Production possibilities Gains from trade

Chapter 3 Labor Productivity and Comparative Advantage: The Ricardian Model 1-1 Preview Opportunity costs and comparative advantage A one-factor Ricardian model Production possibilities Gains from trade

Tanzania. Coffee Annual. Tanzania Coffee Annual Report

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Required Report - public distribution Date: GAIN Report

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Required Report - public distribution Date: GAIN Report

Does infant industry argument justify diversification policy in Argentinean wine sector?

Does infant industry argument justify diversification policy in Argentinean wine sector? N. Khachatryan 1, H. Schuele 1, A. Khachatryan 1 1 University of Hohenheim, Stuttgart, Germany Paper prepared for

Does infant industry argument justify diversification policy in Argentinean wine sector? N. Khachatryan 1, H. Schuele 1, A. Khachatryan 1 1 University of Hohenheim, Stuttgart, Germany Paper prepared for

KOREA MARKET REPORT: FRUIT AND VEGETABLES

KOREA MARKET REPORT: FRUIT AND VEGETABLES 주한뉴질랜드대사관 NEW ZEALAND EMBASSY SEOUL DECEMBER 2016 Page 2 of 6 Note for readers This report has been produced by MFAT and NZTE staff of the New Zealand Embassy

KOREA MARKET REPORT: FRUIT AND VEGETABLES 주한뉴질랜드대사관 NEW ZEALAND EMBASSY SEOUL DECEMBER 2016 Page 2 of 6 Note for readers This report has been produced by MFAT and NZTE staff of the New Zealand Embassy

INDIA: END OF THE SUGAR CYCLE? PRESENTED BY: ABINASH VERMA, DG, ISMA

INDIA: END OF THE SUGAR CYCLE? PRESENTED BY: ABINASH VERMA, DG, ISMA Outline of Presentation 2 The Indian Sugar Cycle Factors impacting the Cycle Do we see an end to the Cycle? Can the Cycle be better

INDIA: END OF THE SUGAR CYCLE? PRESENTED BY: ABINASH VERMA, DG, ISMA Outline of Presentation 2 The Indian Sugar Cycle Factors impacting the Cycle Do we see an end to the Cycle? Can the Cycle be better

Economic Losses from Pollution Closure of Clam Harvesting Areas in Machias Bay

Economic Losses from Pollution Closure of Clam Harvesting Areas in Machias Bay Kevin Athearn, Ph.D. University of Maine at Machias June 8, 2012 Tora Johnson (UMM) and Brian Beal (UMM) assisted with this

Economic Losses from Pollution Closure of Clam Harvesting Areas in Machias Bay Kevin Athearn, Ph.D. University of Maine at Machias June 8, 2012 Tora Johnson (UMM) and Brian Beal (UMM) assisted with this

Overview of the Manganese Industry

39th Annual Conference Istanbul, Turkey 2013 Overview of the Manganese Industry International Manganese Institute Alberto Saavedra Market Research Manager June, 2013 Introduction Global Production Supply,

39th Annual Conference Istanbul, Turkey 2013 Overview of the Manganese Industry International Manganese Institute Alberto Saavedra Market Research Manager June, 2013 Introduction Global Production Supply,

The Sources of Risk Spillovers among REITs: Asset Similarities and Regional Proximity

The Sources of Risk Spillovers among REITs: Asset Similarities and Regional Proximity Zeno Adams EBS Business School Roland Füss EBS Business School ZEW Mannheim Felix Schinder ZEW Mannheim Steinbeis University

The Sources of Risk Spillovers among REITs: Asset Similarities and Regional Proximity Zeno Adams EBS Business School Roland Füss EBS Business School ZEW Mannheim Felix Schinder ZEW Mannheim Steinbeis University

July 19, 2018 I Industry Research Sugarcane FRP increased to Increase in sugarcane FRP for season Rs.275 per quintal for

Sugarcane FRP increased to Rs.275 per quintal for 2018-19 sugar season Contact: Madan Sabnavis Chief Economist madan.sabnavis@careratings.com 91-022-6754 3489 Bhagyashree C. Bhati Research Analyst bhagyashree.bhati@careratings.com

Sugarcane FRP increased to Rs.275 per quintal for 2018-19 sugar season Contact: Madan Sabnavis Chief Economist madan.sabnavis@careratings.com 91-022-6754 3489 Bhagyashree C. Bhati Research Analyst bhagyashree.bhati@careratings.com

The state of the European GI wines sector: a comparative analysis of performance

The state of the European GI wines sector: a comparative analysis of performance Special Report November 2017 1. Overview of a growing global wine market Wine is one of the most globalised products. The

The state of the European GI wines sector: a comparative analysis of performance Special Report November 2017 1. Overview of a growing global wine market Wine is one of the most globalised products. The

CENTRAL AMERICA COFFEE RUST ACTION PLAN 2013 Component 1 Integrated Coffee Rust Management. LEADERS and PARTICIPANTS

Component 1 Integrated Coffee Rust Management 1: INTEGRATED COFFE RUST MANAGEMENT 1.1 Establishment of a Regional Program of Integrated Coffee Rust Management for commonly used susceptible varieties grown

Component 1 Integrated Coffee Rust Management 1: INTEGRATED COFFE RUST MANAGEMENT 1.1 Establishment of a Regional Program of Integrated Coffee Rust Management for commonly used susceptible varieties grown

Citrus: World Markets and Trade

United States Department of Agriculture Foreign Agricultural Service Citrus: World Markets and Trade Oranges Global orange production for 2012/13 is forecast to drop over 4 percent from the previous year

United States Department of Agriculture Foreign Agricultural Service Citrus: World Markets and Trade Oranges Global orange production for 2012/13 is forecast to drop over 4 percent from the previous year

Preview. Introduction. Chapter 3. Labor Productivity and Comparative Advantage: The Ricardian Model

Chapter 3 Labor Productivity and Comparative Advantage: The Ricardian Model. Preview Opportunity costs and comparative advantage A one-factor Ricardian model Production possibilities Gains from trade Wages

Chapter 3 Labor Productivity and Comparative Advantage: The Ricardian Model. Preview Opportunity costs and comparative advantage A one-factor Ricardian model Production possibilities Gains from trade Wages

Coffee market ends 2015/16 in deficit for the second consecutive year

Coffee market ends 2015/16 in deficit for the second consecutive year The coffee market settled up by 5.5% in September, mostly driven by a steady increase in Robusta prices supported by concerns over

Coffee market ends 2015/16 in deficit for the second consecutive year The coffee market settled up by 5.5% in September, mostly driven by a steady increase in Robusta prices supported by concerns over

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S.

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Required Report - public distribution Date: GAIN Report

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Required Report - public distribution Date: GAIN Report

LETTER FROM THE EXECUTIVE DIRECTOR COFFEE MARKET REPORT. November 2004

International Coffee Organization Organización Internacional del Café Organização Internacional do Café Organisation Internationale du Café E LETTER FROM THE EXECUTIVE DIRECTOR COFFEE MARKET REPORT November

International Coffee Organization Organización Internacional del Café Organização Internacional do Café Organisation Internationale du Café E LETTER FROM THE EXECUTIVE DIRECTOR COFFEE MARKET REPORT November

MONTHLY COFFEE MARKET REPORT

E MONTHLY COFFEE MARKET REPORT May 2014 After five consecutive months of rising prices, the coffee market reversed lower in May. From a high of 179 cents/lb in April, the daily price of the ICO composite

E MONTHLY COFFEE MARKET REPORT May 2014 After five consecutive months of rising prices, the coffee market reversed lower in May. From a high of 179 cents/lb in April, the daily price of the ICO composite

Gender equality in the coffee sector. Dr Christoph Sänger 122 nd Session of the International Coffee Council 17 September 2018

Gender equality in the coffee sector Dr Christoph Sänger 122 nd Session of the International Coffee Council 17 September 2018 Gender equality and the Sustainable Development Agenda Achieving gender equality

Gender equality in the coffee sector Dr Christoph Sänger 122 nd Session of the International Coffee Council 17 September 2018 Gender equality and the Sustainable Development Agenda Achieving gender equality

DRY BEANS PRICES AND INCOME DISTRIBUTION IN RWANDA: A NON- PARAMETRIC ANALYSIS

Research article DRY BEANS PRICES AND INCOME DISTRIBUTION IN RWANDA: A NON- PARAMETRIC ANALYSIS Odunga, Pius Ongoro Jaramogi Oginga Odinga University of Science and Technology (JOOUST, Kenya) Kigali Institute

Research article DRY BEANS PRICES AND INCOME DISTRIBUTION IN RWANDA: A NON- PARAMETRIC ANALYSIS Odunga, Pius Ongoro Jaramogi Oginga Odinga University of Science and Technology (JOOUST, Kenya) Kigali Institute

Coffee market recovers slightly from December slump

Coffee market recovers slightly from December slump After reaching its lowest level in 22 months in December 2017, the monthly average of the ICO composite indicator price increased by 1.4% to 115.60 US

Coffee market recovers slightly from December slump After reaching its lowest level in 22 months in December 2017, the monthly average of the ICO composite indicator price increased by 1.4% to 115.60 US

Total Sugar sales Jan Sept (T)

") I: BACKGROUND This is September newsletter publication of Agriculture and Food Authority, It gives insights into how the period January September 2016 performed, focusing on the local sugar market prices;

I: BACKGROUND This is September newsletter publication of Agriculture and Food Authority, It gives insights into how the period January September 2016 performed, focusing on the local sugar market prices;